February 4, 2026

Invisible insurance integrates protection directly into the products or services you’re already buying - no forms, no separate decisions, no claims hassle. It activates automatically when needed, enhancing convenience and simplifying the customer experience.

Why it matters:

Solutions like Walnut make this integration easier, offering tools to launch insurance programs quickly, handle compliance, and automate processes. With invisible insurance, businesses improve customer satisfaction, retention, and loyalty while reducing effort for everyone involved.

Invisible insurance hinges on three key design principles that remove friction at every step of the customer journey. These principles - pre-filled data, automatic enrollment, and silent payouts - work together to ensure interactions are effortless and seamless.

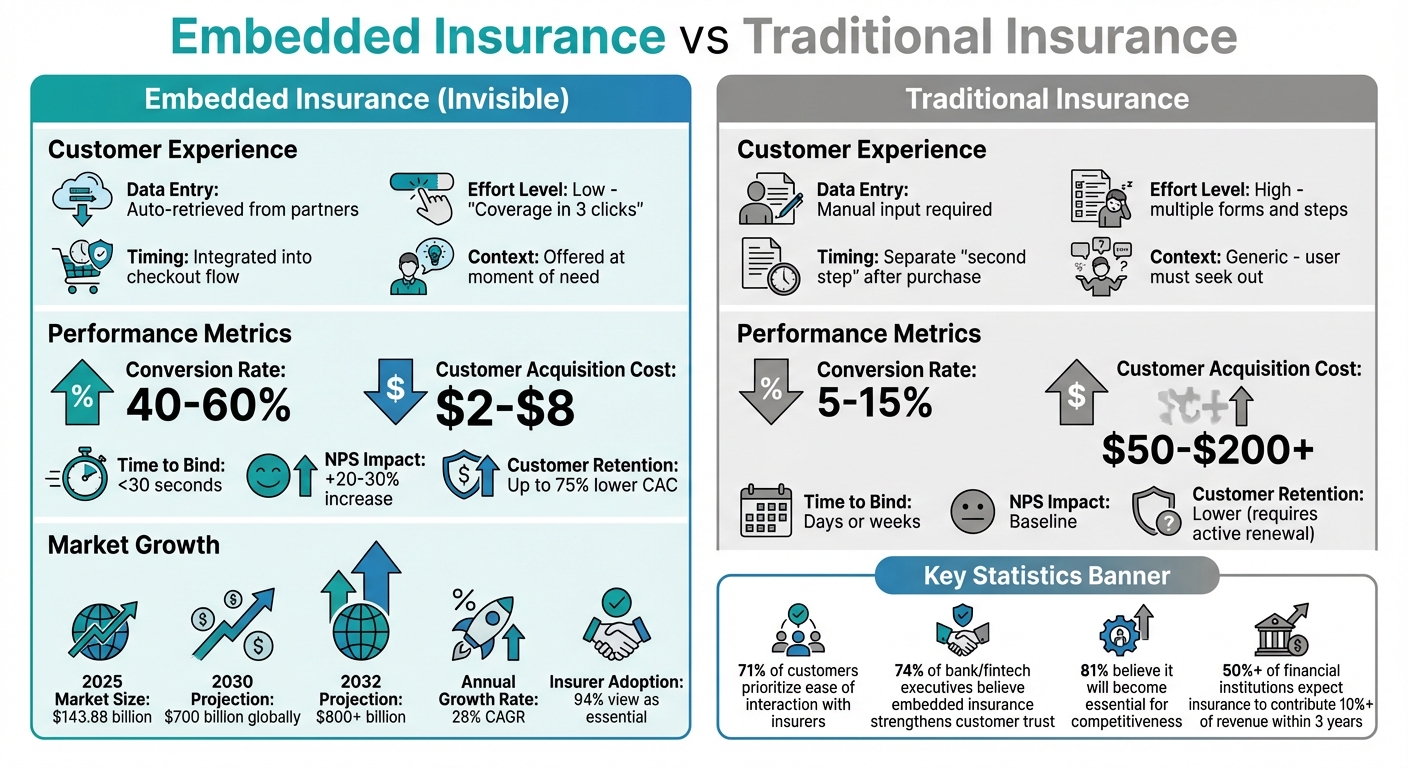

Filling out endless forms is one of the most tedious aspects of buying insurance. Pre-filled data solves this by automatically pulling information from partner platforms, like e-commerce sites or automotive marketplaces, to generate instant quotes. Customers don’t have to type a single detail.

Tesla demonstrated this concept in 2019 with Tesla Insurance. By using real-time data from vehicle sensors, Tesla monitors driver performance and automates pricing. Instead of relying on traditional questions for underwriting, their system collects data continuously in the background [1].

Aspect

Traditional Onboarding

Pre-Filled (Embedded) Onboarding

Manual input of personal and asset details

Data auto-retrieved from partners

High; requires multiple forms and steps

Low; often described as "Coverage in 3 clicks"

"Second step" after the primary purchase

Integrated directly into the checkout flow

Generic; user must seek out the product

Hyper-relevant; offered at the moment of need

This shift toward Embedded Insurance 2.0 focuses on leveraging customer data throughout the insurance process - not just at the point of sale. The embedded property and casualty (P&C) insurance market in the U.S. is expected to hit $70 billion by 2030 [1].

With data entry simplified, automatic enrollment further enhances the experience.

Automatic enrollment ensures coverage starts immediately upon purchase. Customers don’t have to make a separate decision about whether to buy insurance - it’s already included when they need it most.

The embedded insurance market is forecasted to grow from $143.88 billion in 2025 to over $800 billion by 2032, with a compound annual growth rate of 28% [3]. This growth reflects the fact that 94% of insurers now view embedded insurance as essential to their long-term strategies [3].

Embedded insurance models also deliver better conversion rates compared to standalone insurance products. Why? Automatic enrollment removes barriers right when customers are ready to make a purchase.

"Embedded insurance is transforming from a distribution tactic to a customer experience strategy as insurers prioritize seamless, friction-free protection."

By activating coverage at the point of sale, automatic enrollment boosts customer confidence and reduces post-purchase stress [3]. In fact, digital insurance claims saw a 17-point rise in customer satisfaction in 2024, thanks to improved mobile and web services [3].

Once data and enrollment are streamlined, silent payouts complete the frictionless experience.

Silent payouts ensure customers receive benefits without needing to file claims manually. Using auto-triggers - such as detecting a flight delay or other data events - the system processes payouts automatically when a covered event occurs.

This eliminates the frustrating "claims crawl" and replaces manual processes with data-driven automation [6]. Embedded insurance models with silent payouts see conversion rates of 40–60%, compared to just 5–15% for traditional models [9].

Metric

Embedded (Silent) Model

Traditional Model

40–60%

5–15%

$2–$8

$50–$200+

< 30 seconds

Days or weeks

High (platform-driven)

Medium

Silent payouts align with the "Zero UI" trend, where technology operates in the background, responding to context without requiring user input [7][8]. Customers only notice it when it delivers a benefit [4].

"In 2025, the best insurance won't feel like insurance. It will just be there - contextual, invisible, and real-time."

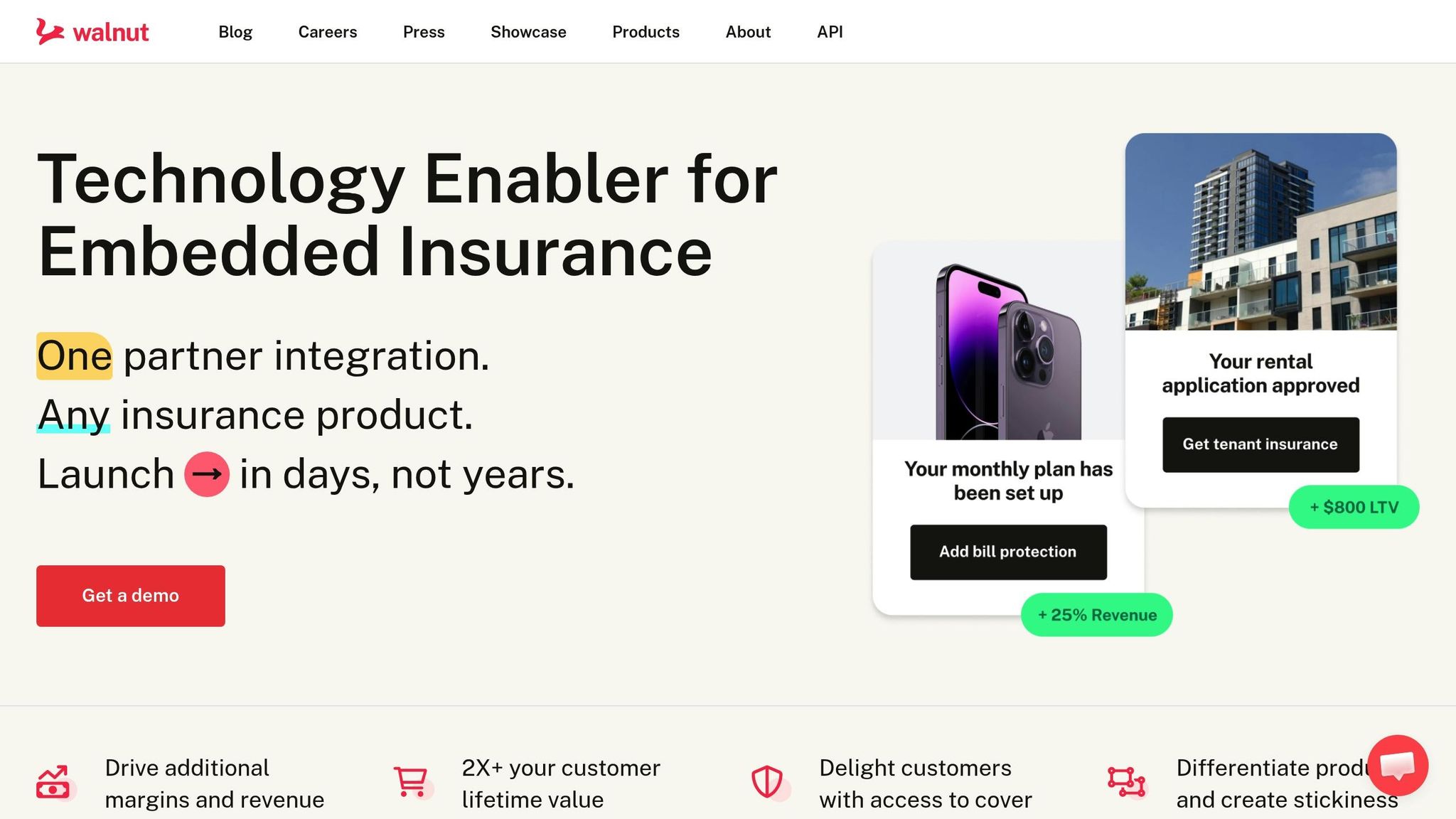

Walnut transforms the concept of invisible insurance into a practical reality, offering flexible integration options that cater to varying technical capabilities. By connecting to over 14 insurance carriers through a single API, Walnut eliminates the need for multiple negotiations and simplifies backend management processes. This streamlined approach allows companies to launch insurance programs in just days instead of years [11][10]. It’s a seamless solution that aligns perfectly with the frictionless experience discussed earlier.

"We're excited to partner with Walnut, bringing insurance into the digital age and creating greater access to protection for all Canadians. We've been impressed with how their infrastructure has been able to support us in growing our product offering."

Clients such as Neo Financial and Propel Holdings have successfully embedded insurance into their platforms using Walnut, resulting in smooth integration and rapid deployment [10][11].

Walnut takes care of licensing, compliance, policy creation, certificate generation, and post-purchase delivery, allowing partners to concentrate on their primary business goals [11][12]. The platform also handles multi-party payouts and revenue reconciliation, automating revenue splits between brokers, enterprise partners, and insurers [12].

By enabling customer data to flow effortlessly, Walnut delivers on the promise of pre-filled data integration, enhancing the overall experience.

Walnut provides three integration tiers, offering a balance between customization and ease of implementation. All options ensure seamless API-driven data integration, allowing customer details to pass automatically from the partner platform to the insurance system [12].

Integration Option

Data Sharing Level

Technical Requirements

Impact on User Experience

Medium (via referral links/standalone)

Minimal setup; launch in under a day

Quick and co-branded, though with a slight step in the journey

High (Full data synchronization)

Requires developers for full data sync

Fully seamless; insurance becomes part of the native experience

High (In-journey cross-sells)

Pre-filled lead data for digital/advisor sales

Supports digital or advisor-driven sales with pre-filled data

For example, ATCO, a retail energy provider serving over 3 million customers, used Walnut to seamlessly integrate insurance into their "Friends and Family" energy plans. This created a smooth digital protection experience during the onboarding process [10].

Walnut’s platform supports instant policy binding through both no-code and API-driven options [10]. Businesses with no prior insurance expertise can launch branded insurance programs in less than a day using no-code solutions. Meanwhile, companies with in-house technical teams can build deeper integrations using Walnut’s modern APIs [11].

The platform’s quoting and underwriting engines use partner data or existing pricing APIs to provide real-time, dynamic pricing within the customer journey [12]. This ensures immediate coverage activation at the point of purchase.

Walnut also handles licensing and compliance, paired with multi-channel broker support, so partners don’t have to navigate complex regulatory requirements or hire insurance specialists [11]. This infrastructure ensures automatic enrollment complies with legal standards while maintaining a smooth customer experience.

Once a policy is activated, Walnut automates the entire post-purchase workflow. From policy creation and certificate generation to delivery, everything is handled without manual effort [12]. Additionally, the platform streamlines claims processing by managing data flow between the partner’s front-end systems and the carrier’s backend.

Walnut also automates multi-party payouts, ensuring accurate revenue splits among brokers, enterprise partners, and insurers [12]. Beyond that, the platform manages lead tracking, user management (including policy updates and cancellations), and reporting throughout the lifecycle of the insurance product [12].

This end-to-end automation allows businesses to offer invisible insurance without the need for complex infrastructure, making it easier than ever to integrate insurance into existing systems.

Invisible insurance can directly influence a company’s bottom line by boosting customer satisfaction and loyalty. When insurance is seamlessly integrated into the customer experience rather than offered as a separate product, the benefits are clear and measurable.

Traditional insurance often frustrates customers with tedious forms and complicated processes [5]. Simplifying these steps through embedded insurance significantly enhances customer advocacy. For example, data shows that embedded insurance models can lead to a 20–30% boost in Net Promoter Scores (NPS) compared to standalone insurance purchases.

This improvement is especially noticeable during emotionally charged moments, like filing a claim. Trust in a brand is heavily influenced by these interactions [13]. Automated, instant payouts eliminate the delays and stress associated with manual, paper-based processes, turning what could be a negative experience into a positive one [5][13]. For mid-sized carriers, addressing this "invisible CX gap" can unlock tens of millions of dollars in value [13].

The industry is taking note. 74% of bank and fintech executives believe embedded insurance strengthens customer trust, and 81% think it will soon shift from a "nice-to-have" to an essential offering for staying competitive [2]. This increase in customer advocacy not only drives NPS growth but also translates into stronger retention rates.

Improved NPS is just part of the story. Businesses that implement embedded insurance also see higher customer retention. By weaving insurance into digital ecosystems, companies can drastically lower customer acquisition costs (CAC) - by as much as 75% [14]. At the same time, these integrations enhance customer retention and boost Customer Lifetime Value (CLV) by making insurance a natural part of the primary product experience [15].

Metric

Embedded Insurance

Traditional Insurance

Minimal (pre-filled/automatic)

High (manual forms/separate site)

Up to 75% lower

High (marketing/agent commissions)

Higher (ecosystem integration)

Lower (requires active renewal)

20–30% increase

Baseline

Real-world examples illustrate this potential. In mid-2023, Brazilian digital bank Nubank teamed up with Chubb to launch "Nubank Vida." The result? Over 560,000 active policies, with 50% of those customers purchasing life insurance for the first time [2]. Additionally, more than 50% of financial institutions expect insurance to contribute at least 10% of their total revenue within the next three years, up from only 20% today [2].

The market for embedded insurance is on a rapid growth trajectory, projected to hit $700 billion globally by 2030, potentially representing 25% of the total property and casualty market worldwide [14][15]. These numbers highlight how embedding insurance into everyday experiences not only drives engagement but also fosters long-term customer loyalty. When insurance blends seamlessly into the background, customers are far more likely to stick with it.

The most effective insurance is the kind that customers don’t need to think about. When coverage is seamlessly pre-filled, automatically enrolled, and quietly paid out, it becomes a natural extension of the customer experience. This streamlined approach brings clear benefits.

Businesses embedding insurance into their platforms have reported over double the customer lifetime value, a 30% increase in engagement, and a 25% drop in support inquiries - redefining how they connect with their customers.

Walnut’s infrastructure enables businesses of all sizes to integrate invisible insurance effortlessly. With no-code, co-branded, or API-driven solutions, Walnut handles compliance, carrier integration, and backend claims automation. Partners like Neo Financial and ATCO already leverage this system, collectively reaching over 4 million customers.

As market trends highlight these advantages, more companies are recognizing built-in insurance as a competitive edge. Invisible insurance ensures customers are protected exactly when they need it, without unnecessary hassle.

Explore how Walnut can help integrate invisible insurance into your platform and turn coverage into a strategic asset.

Embedded insurance enhances customer satisfaction and loyalty by making protection simple and stress-free. Features like pre-filled data, automatic enrollment, and silent payouts ensure customers are covered without the need for constant oversight or extra effort. This streamlined approach resonates with today’s preference for convenience, especially among Millennials and Gen Z.

By weaving insurance into the purchase process - whether at checkout or during service sign-up - customers gain instant protection without jumping through additional hoops. Silent payouts and automatic renewals further reduce friction, fostering trust and creating a smoother experience. This often translates into higher satisfaction, stronger loyalty, and better retention. Companies that embrace these practices frequently report improved Net Promoter Scores (NPS) and stronger, longer-lasting customer relationships.

Automatic enrollment and silent payouts are transforming the way customers interact with insurance, making the process smoother and more hassle-free.

Automatic enrollment signs people up for coverage by default, cutting out extra steps and boosting participation rates. With this approach, customers can start enjoying their benefits immediately, without delays or unnecessary effort.

On the other hand, silent payouts take the stress out of the claims process. Payments are handled automatically when they're needed, so customers don’t have to worry about filing claims or taking additional steps. It’s a behind-the-scenes system that reduces friction and makes the experience much more straightforward.

By combining these features, insurance becomes easier to use and more dependable. Customers are more likely to feel satisfied and stick around, thanks to a process that prioritizes simplicity and convenience. It’s a modern approach that aligns with what today’s policyholders expect - effortless and reliable service.

Walnut streamlines the integration of invisible insurance into digital platforms with its API-driven technology and no-code tools. These solutions make it easy for businesses to weave insurance offerings into their existing systems - whether that's an e-commerce site or a financial app - without requiring extensive development work.

Through real-time data exchange, Walnut’s platform automates key processes like policy issuance, underwriting, and claims management. This automation ensures a smooth experience for customers, blending convenience with an almost imperceptible integration. Businesses can introduce insurance at just the right moments, like during checkout or onboarding, making it feel like a natural extension of the user experience.

On top of that, Walnut emphasizes compliance and data security, helping businesses protect customer trust. By offering seamless insurance integration, companies can boost satisfaction, build loyalty, and drive additional revenue.