March 6, 2026

In a world where fast transactions dominate, traditional insurance often fails to meet modern needs. Enter embedded micro-income insurance - a system that provides transaction-specific coverage, offering protection for single rides, deliveries, or purchases. With premiums as low as $0.01 to $0.06 per transaction, this approach is affordable, simple, and tailored to real-time risks.

Companies like Walnut are leading the charge, integrating insurance directly into payment systems through flexible options like co-branded links, referral data, or APIs. These tools not only improve customer trust but also boost revenue, with platforms reporting up to 4x higher average revenue per user (ARPU) and 2x customer lifetime value. By leveraging real-time transaction data and partnering with over 14 carriers, Walnut ensures precise underwriting and risk-sharing, making micro-income insurance scalable and reliable.

This shift is redefining financial safety nets, embedding protection into everyday transactions to reduce friction, increase retention, and provide peace of mind during uncertain times.

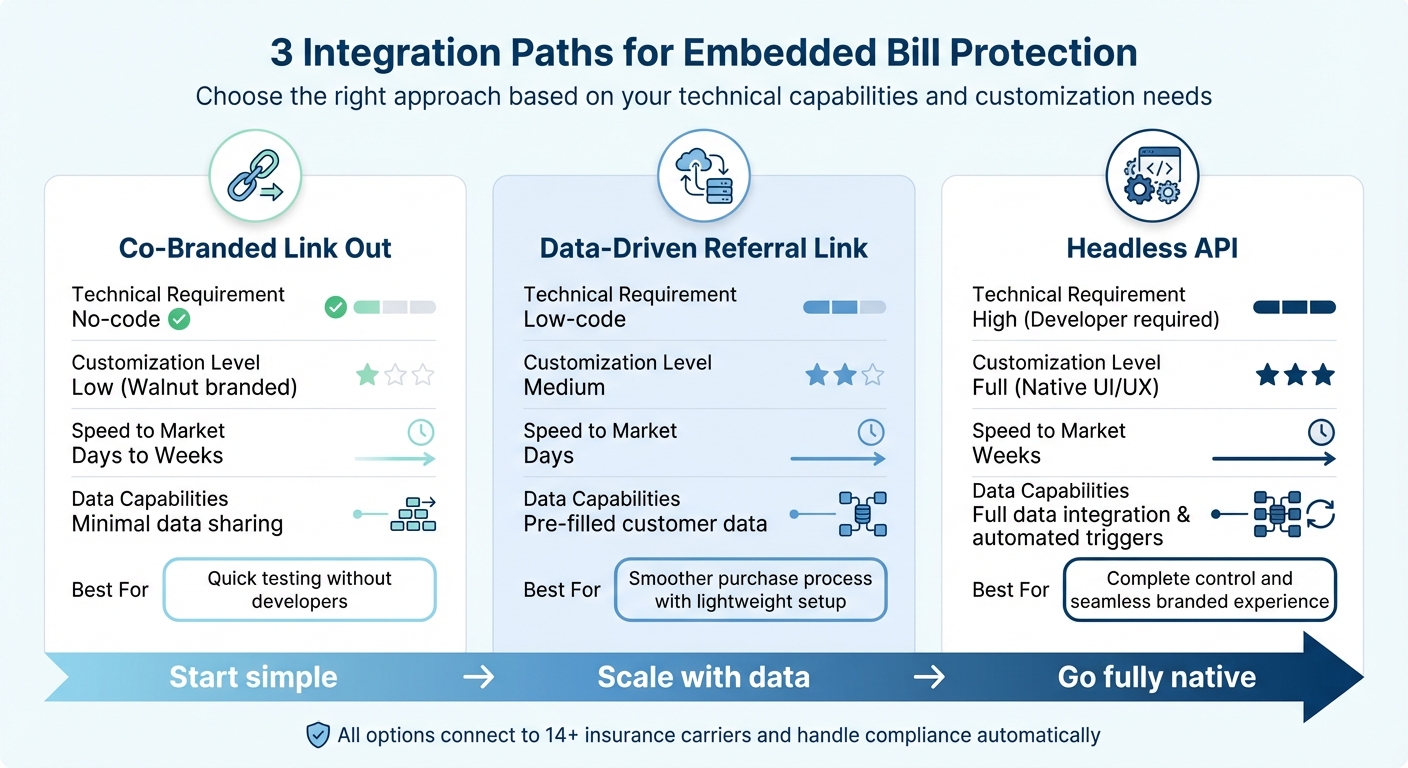

Walnut's product architecture is designed to make embedding bill protection straightforward, offering three flexible integration paths to suit different needs and technical capabilities. Here's a quick breakdown:

These options cater to varying priorities, from quick deployment to deep customization, ensuring businesses can integrate insurance solutions effectively.

At the core of Walnut's system is its "One API" approach, which simplifies the deployment of insurance products, including bill and payment protection, through a single integration [1]. The platform connects with over 14 insurance carriers, giving businesses the freedom to choose products tailored to their customers' needs.

Walnut’s technical stack automates traditionally manual tasks, offering features like real-time pricing, instant quotes, and automated claims processing. Pre-filled data capabilities make one-click coverage possible at the point of purchase, reducing friction and improving the user experience [2]. Additionally, Walnut handles compliance through full-service licensing and broker support, allowing partners to launch branded insurance programs without needing prior experience in the insurance industry [1]. With this infrastructure, businesses can go live in days instead of years [1].

Here's a comparison to help weigh the trade-offs between the three integration paths:

Integration Option

Technical Requirement

Customization Level

Speed to Market

Data Capabilities

No-code

Low (Walnut branded)

Days to Weeks

Minimal data sharing

Low-code

Medium

Days

Pre-filled customer data

High (Developer required)

Full (Native UI/UX)

Weeks

Full data integration & automated triggers

The choice boils down to priorities. If speed and ease of setup are key, the Co-Branded Link Out might be the way to go. For platforms aiming for a fully branded, seamless experience, the Headless API offers ultimate control - though it requires more developer involvement [3].

Traditional insurance underwriting often relies on outdated methods, using historical averages and static assumptions. This approach can be slow and imprecise, failing to reflect actual risks. Walnut takes a different route, leveraging real-time transaction data to make underwriting dynamic and accurate. By analyzing behavioral signals - such as subscription trends, payment histories, or even contextual cues like airport Wi-Fi usage - the platform pinpoints the ideal moment to offer coverage [6].

This method directly addresses one of micro-insurance's biggest challenges: information asymmetry. Real-time data allows Walnut to fine-tune pricing, reduce fraud through automated detection, and align coverage with individual customer needs [7][8].

"Data is at the core of any insurance offering, empowering insurers to understand the unique needs and risk profiles of underserved segments and helping to create better risk assessment, pricing, and distribution models." - CGAP Research & Publications

By embedding insurance at critical moments - such as during a lease signing or while paying a bill - Walnut helps carriers develop stronger risk profiles with less adverse selection. This contrasts with optional insurance models where only the most risk-averse individuals typically opt in [6]. Such precise underwriting sets the stage for effective risk distribution, as discussed below.

Walnut goes beyond underwriting by managing risk through a network of more than 14 insurance carriers. This diversified model spreads liability, ensuring the platform can scale without overburdening any single partner's financial capacity. It addresses a key issue in micro-insurance: shared risk, where a single event - like a regional disaster - can strain a small risk pool [8].

By distributing policies across multiple carriers, Walnut ensures it can handle large volumes of micro-transactions while maintaining financial stability. Insurers benefit from profit-sharing arrangements, avoiding the need to sink heavy upfront costs into customer acquisition. This makes the model more appealing and sustainable for carriers [5].

"For insurers and brokers, Walnut's platform provides significant benefits, such as the ability to profit share versus front-loading marketing costs, improving risk management, and unlocking untapped channels." - Walnut Insurance

The platform also supports multi-channel distribution, ranging from co-branded experiences to headless API integrations. This flexibility allows risk to flow seamlessly across various digital ecosystems, reducing the chance of bottlenecks [5]. Such redundancy ensures reliable service and safeguards the system from single points of failure [9]. With the embedded insurance market expected to generate $70 billion to $700 billion in gross written premiums by 2030, Walnut's approach positions it well for scalable growth [9][10].

Walnut's platform seamlessly integrates at the transaction layer, where customers already handle their money. This is made possible through modern APIs that use a simple x-api-key header for authentication. This setup allows e-wallets, lending platforms, and payment processors to embed bill protection without overhauling their existing infrastructure [[11]].

Here’s how it works: once a customer completes a transaction, the API gathers the necessary customer data to activate coverage effortlessly. It then generates a checkoutURL and tempId, guiding users smoothly from payment to insurance activation [[12]]). The process is so streamlined that even non-technical teams can implement it quickly. This efficient workflow demonstrates how embedded bill protection operates in real time, making it easy to adopt and implement.

Neo Financial is one example of a company leveraging this integration for its wide range of coverage options.

Embedded bill protection doesn’t just simplify coverage activation; it also delivers meaningful financial advantages. Businesses using Walnut's platform report a more than 2X increase in customer lifetime value while also reducing churn by making their products more appealing [1]. For lenders, this type of protection helps cut down on defaults, charge-offs, and collection costs by covering payments during events like job loss or illness.

The revenue model focuses on branded insurance programs that enhance profit margins and improve capital efficiency. By stabilizing loss curves and introducing new revenue streams, institutions can strengthen their financial performance. This form of micro-income insurance, embedded directly into transactions, plays a key role in boosting customer retention and revenue. With 94% of insurers identifying embedded insurance as a priority, this trend is rapidly gaining traction across industries [2]. Businesses can use real-time dashboards to track enrollment rates and revenue growth as coverage expands across their customer base [1].

Insurance is becoming part of everyday transactions, working quietly in the background without requiring active engagement from customers. With the help of pre-filled data and automatic enrollment, policies activate seamlessly based on transactional data. APIs play a critical role here, using real-time signals to trigger coverage during specific events. For example, a delayed flight could automatically activate travel insurance, or a job loss might initiate bill protection - no forms or claims required. Through tools like Headless API, companies like Walnut enable this kind of native, behind-the-scenes coverage activation. This approach not only simplifies the process for users but also lays the groundwork for scalable and compliant insurance solutions.

As invisible insurance gains traction, the ability to scale and meet regulatory standards has become a key factor for success. For example, 23 states and Washington, D.C. have already adopted the NAIC's model AI bulletin, signaling growing efforts to standardize AI regulations in the insurance industry. Walnut connects over 14 insurance carriers with non-insurance platforms, creating an efficient system for distribution, risk-sharing, and compliance. This streamlined approach supports embedded bill protection models, which are increasingly seen as essential to modern financial safety nets. With 94% of insurers identifying embedded insurance as a critical part of their strategy, companies that can implement these solutions efficiently and within regulatory frameworks are poised to thrive in a rapidly evolving market. [2][13]

Financial protection has seamlessly woven itself into the fabric of everyday transactions. Walnut integrates bill protection directly into payment processes, loan applications, and subscription services, embedding insurance directly at the transaction level. This shift from standalone policies to transaction-level protection marks a major transformation in how financial safety nets function.

Walnut offers three integration options that allow for quick and flexible deployment without requiring major system changes. By connecting with over 14 carriers and automating compliance, Walnut simplifies the implementation process. Its use of transaction data for underwriting enables instant, personalized coverage with minimal friction. This adaptability not only makes implementation straightforward but also empowers businesses to better navigate financial risks.

With 94% of insurers now considering embedded insurance a critical strategy [2], companies that can adopt these solutions efficiently will gain a competitive edge. This type of invisible insurance not only boosts convenience but also mitigates financial shocks before they occur, ensuring customers can stay on track with their obligations during periods of job loss or disability. It also strengthens the financial system by building resilience into its core. This evolution toward transaction-based risk management underscores the shift discussed earlier.

Businesses stand to gain significantly from embedded bill protection, benefiting from improved retention, increased revenue, and effortless integration.

Embedded bill protection automatically safeguards certain transactions, like travel delays or fraudulent charges. It works effortlessly in the background, requiring no extra effort from the customer, offering both ease and reassurance.

The best integration option depends heavily on what your platform requires and how technically equipped it is. If you're looking for something straightforward and easy to implement, no-code tools or basic data-sharing methods can get the job done with minimal hassle. However, if you need something more robust and tailored, API-based integration is the way to go. It allows for custom features, automation, and ensures compliance with U.S. regulations. Plus, APIs provide the adaptability needed to support long-term growth, perfectly aligning with Walnut’s commitment to delivering efficient and secure embedded insurance solutions.

Risk sharing among insurance carriers works by pooling resources to spread financial risks more evenly. Each carrier contributes premiums and, in return, shares losses according to pre-determined terms, typically based on their level of exposure. Some advanced systems take this further by using layered or dynamic allocation models. These models, often powered by digital platforms, allow for real-time adjustments in how risks are distributed. This method not only promotes stability but also improves the efficiency of risk transfer. It's especially useful in embedded insurance setups, such as offering micro-income protection tied to individual transactions.