January 2, 2026

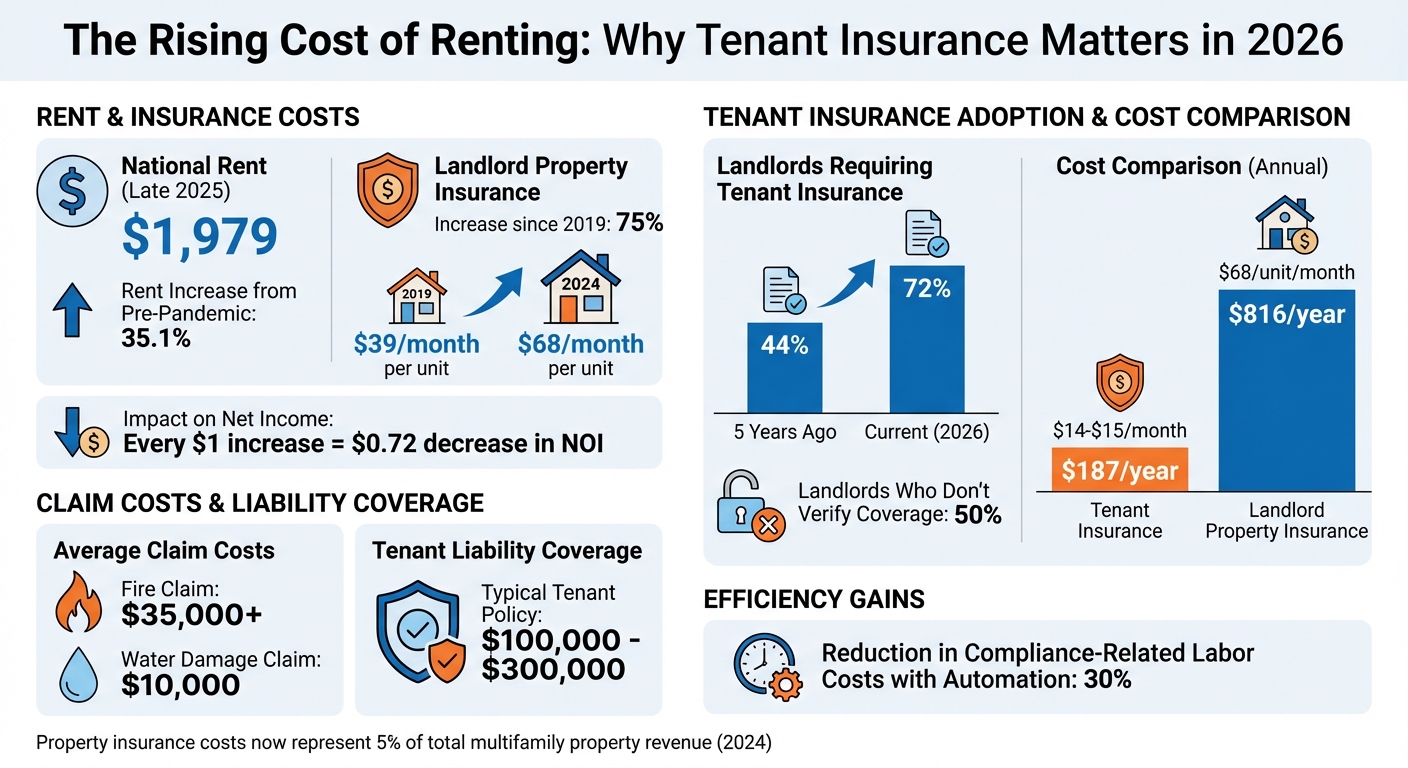

Rent prices have hit record highs, with the national average reaching $1,979 by late 2025 - a 35.1% increase from pre-pandemic levels. At the same time, landlords face skyrocketing property insurance costs, up 75% since 2019. These rising expenses, combined with tenant financial strain and increased liability risks, are driving more landlords to require tenant insurance in leases starting in 2026.

Here’s why tenant insurance is becoming a must:

With 72% of landlords now requiring tenant insurance, this trend is reshaping the rental market, offering financial protection for both landlords and tenants.

Although no federal law mandates tenant insurance, landlords in most states have the authority to make it a lease requirement [5][7]. This creates a mix of rules - some states outline clear laws, while others leave it entirely up to landlords.

Take Oregon, for example. Under ORS 90.222, landlords can require tenants to carry liability coverage up to $100,000 or an amount typical for similar properties. However, this requirement comes with conditions: landlords must maintain their own liability coverage and provide proof if tenants request it. Additionally, Oregon law prohibits landlords from requiring insurance for tenants in subsidized housing or for those earning 50% or less of the area’s median income [4].

Virginia, on the other hand, has its own approach under §55-248.7:2. Here, landlords can demand both "damage insurance" and renter's insurance as part of the lease. If premiums are collected before a tenant moves in, the combined total of premiums and security deposits cannot exceed two months’ rent. Landlords also have the option to purchase insurance on behalf of tenants and recover the costs, including administrative fees [6].

Property management groups are increasingly pushing for mandatory insurance clauses in leases. This trend is especially noticeable in states like Florida, Louisiana, and Texas, where property insurance costs are much higher due to the risk of natural disasters [1][5]. These mandates highlight the growing need for financial protections, both for landlords and tenants.

The financial impact of uninsured tenants is even more critical in light of the varying regulations across states. By 2024, property insurance expenses made up about 5% of the total revenue for an average multifamily property, with landlords shouldering most of these costs instead of passing them on to tenants [1].

Uninsured tenants pose significant risks. When tenant negligence leads to damages not covered under a landlord’s commercial insurance, filing claims can drive up premiums, increasing overall costs [2][3][8]. This creates a feedback loop where higher claims lead to higher premiums, which then burden landlords further [2][8].

Tenant insurance helps shift these financial risks. Most policies offer liability coverage between $100,000 and $300,000, which can cover damages caused by tenants without affecting a landlord’s claims history. This is particularly important in multi-unit buildings, where one tenant’s mistake could impact several units [2].

For tenants, the cost is relatively low - around $187 per year on average [7]. Compare that to the approximately $816 per unit that landlords pay annually for property insurance [1]. By requiring tenant insurance, landlords not only protect their own finances but also provide tenants with affordable coverage that offers peace of mind.

Managing tenant insurance manually - using spreadsheets to track documents, contacting insurers, and monitoring expiration dates - leaves plenty of room for mistakes [10][11]. Errors like incorrect dates, coverage limits, or even fraudulent documents can easily go unnoticed.

The challenge often gets worse after tenants move in. Many renters provide proof of insurance to meet lease requirements, only to cancel their policies shortly after. Manual systems often catch these lapses only during random audits [11][12]. Mike Hogentogler, COO at LCOR, highlights this issue:

"The hardest part is that while it's a requirement to have renters insurance to move-in, it's really difficult to keep track of who remains in compliance and who doesn't after they move in."

Shockingly, nearly 50% of landlords don't verify renters' insurance coverage at all, even if it's a lease requirement [13]. Onsite teams, already stretched thin with leasing and maintenance duties, often struggle to chase tenants for renewals. This leads to inconsistent enforcement and delays [11][12]. Companies that adopted automated tracking systems have reported a 30% reduction in compliance-related labor costs [11]. Without such solutions, manual gaps not only slow operations but also increase the risk of costly insurance claims.

When tenants lack liability insurance, landlords often bear the financial burden. For example, the average fire claim costs over $35,000, while water damage claims average around $10,000 [14]. Without tenant coverage, these expenses fall under the property owner's insurance, leading to deductibles and potentially higher premiums [2][14].

Mike Hogentogler explains the ripple effect:

"If a resident doesn't have renters insurance for a problem, it needs to go onto my property insurance, which is now subject to deductibles and also hits my track record."

Uninsured claims can severely strain operating budgets. Between 2019 and 2024, monthly property insurance costs for multifamily buildings surged by more than 75%, jumping from $39 to $68 per unit. For every dollar increase in insurance costs, a property owner's net income drops by about 72 cents, directly affecting Net Operating Income (NOI) and overall property value [1]. These rising costs make uninsured claims an even heavier financial burden for landlords.

Walnut Insurance tackles the hassle of manual tenant insurance management by embedding insurance directly into digital lease processes. Gone are the days of tracking policies through spreadsheets, emails, and voicemails. With Walnut’s platform, tenant insurance policies are activated during onboarding, and all provider details, including policy expiration dates, are automatically logged into a centralized dashboard. Plus, by listing the landlord as an "additional interest" or "interested party", property managers are notified if a tenant’s policy is canceled or lapses. Tenants also receive timely reminders before their policies expire, ensuring smoother compliance [2][14][15].

This automated system directly addresses the manual verification headaches landlords often face, making insurance management less stressful and far more efficient.

Walnut offers three tailored integration options to accommodate various operational setups:

Plan

Technical Requirements

Customization

Data Sharing

Best For

No technical setup needed

Basic branding and color options

No data sharing

Landlords looking for a simple, IT-free solution

Minimal API setup

Branding and color customization

Data sharing for faster onboarding

Property managers aiming for a smoother tenant experience

Moderate technical integration

Fully customized API-driven workflow

Full data sharing

Large-scale operators needing a seamless and branded solution

By embedding insurance into the leasing process, landlords and tenants both gain significant advantages. For landlords, this approach reduces financial risks and helps keep premiums low. As DoorLoop explains:

"When a tenant's policy responds first, it reduces the likelihood of claims against your landlord insurance policy. Staying claim-free helps keep your own insurance rates down."

For tenants, the process is equally streamlined. Insurance can be purchased and proof submitted during lease signing, with policies typically costing between $15 and $30 per month. Some options are even available for as little as $5 per month [15][9][16].

Landlords benefit from better liability protection, closing gaps that could lead to unpaid damages. Considering that fire claims often exceed $35,000 and water damage averages $10,000, tenant insurance ensures landlords aren’t left covering costs beyond security deposits [14].

Walnut Insurance simplifies tenant insurance with a two-step process that works seamlessly with your property management system. First, you set the insurance requirement directly in your lease template. Then, when tenants log into their portal during the move-in process, they’re prompted to meet this requirement immediately.

Tenants have two choices: they can either purchase a policy through Walnut’s integrated platform - where they receive instant quotes and can bind coverage on the spot - or upload proof of an existing insurance policy. Whichever option they choose, the system automatically captures essential details like provider information, policy numbers, and expiration dates. All of this is stored in a centralized dashboard, eliminating the need for manual data entry.

If a tenant opts to purchase a policy through Walnut, their coverage is verified automatically before the lease is finalized. This efficient setup not only speeds up the leasing process but also minimizes administrative tasks for property managers, making the entire workflow smoother and more reliable. [15]

Managing tenant insurance has long been a tedious task for landlords, but Walnut’s automated platform tackles these challenges head-on. By handling policy management digitally, it eliminates the need for manual verifications and reduces compliance issues. A property management professional sums up the frustration well:

"Chasing tenants for renters' insurance is a time-consuming headache. You send emails, leave voicemails, and track everything on a spreadsheet."

Walnut’s solution removes these headaches by automating follow-ups, including sending renewal reminders. The system also offers real-time portfolio visibility, allowing property managers to quickly see which units are covered without sifting through spreadsheets or making phone calls. This level of automation not only saves time but also speeds up tenant onboarding, helping to reduce vacancy periods. [15]

Tenant insurance has become a critical tool for landlords navigating the challenges of 2026. With property insurance costs skyrocketing - up 75% since 2019 - and every $1 increase reducing net income by $0.72, landlords can no longer afford to absorb tenant-caused claims [1]. By requiring tenant insurance with liability coverage, landlords transfer the financial risks of incidents like kitchen fires, water damage, and third-party injuries away from their own policies. This approach not only safeguards their finances but also helps maintain stable premiums and clean loss histories [2].

Beyond financial protection, tenant insurance also introduces operational efficiencies that simplify property management. Manual tracking of policies wastes valuable time that could be better spent on revenue-generating activities. Walnut's embedded platform addresses this by automating policy verification, monitoring coverage in real time, and sending alerts for lapses [15]. This automation-first approach is quickly becoming essential in the competitive rental market.

The numbers tell a compelling story: 72% of landlords now require renters insurance, a significant jump from 44% just five years ago [17][14]. With average fire damage claims exceeding $35,000 and water damage claims averaging $10,000, even a single uninsured event can erase months of rental income [14].

Walnut offers scalable solutions tailored to landlords' needs, from simple co-branded links to fully integrated API workflows. These tools allow landlords to implement tenant insurance requirements seamlessly, whether managing a handful of units or thousands. By ensuring 100% compliance from the start, Walnut reduces administrative headaches while protecting landlords' bottom lines [15].

In a rental market defined by rising costs, tenant insurance is no longer optional - it’s essential. By embracing automated and embedded insurance solutions, landlords not only shield themselves from financial risks but also enhance the tenant experience. These tools provide a competitive edge, ensuring landlords can thrive in today’s high-cost rental environment.

Landlords are increasingly requiring tenant insurance in 2026, driven by legal changes, financial considerations, and operational efficiencies. Updated state laws now allow landlords to make renter’s insurance a mandatory part of lease agreements. This requirement helps safeguard property owners from potential risks, including unpaid damages, liability claims, or lawsuits stemming from tenant-related incidents.

As repair costs and liability claims continue to rise, tenant insurance shifts the financial responsibility for property loss or accidents to the tenant’s policy. Many landlords are also leveraging modern property management systems to simplify the process. These systems often integrate insurance verification directly into digital lease workflows, ensuring tenants meet requirements before moving in. This automation not only reduces manual follow-ups but also helps both landlords and tenants manage risks more effectively.

Renter's insurance provides a layer of financial security for both landlords and tenants, creating a win-win situation. For landlords, it helps address expenses tied to property damage, unpaid repairs, or liability claims - like if a guest gets injured on the property. This added protection can ease conflicts, simplify property management, and might even lead to reduced insurance premiums for the landlord.

On the tenant's side, renter's insurance safeguards personal belongings against risks such as fire, theft, or water damage. It can also cover extra living costs, like hotel stays, if their home becomes temporarily unlivable. Plus, liability coverage ensures tenants aren't stuck footing the bill if they accidentally cause damage or injury. The best part? All these benefits typically come at a cost of less than $20 per month.

Managing tenant insurance manually - whether through spreadsheets, emails, or stacks of paper - can be a logistical headache for landlords and property managers. The process of verifying tenant policies involves gathering and checking details like policy numbers, expiration dates, and proof of coverage. Not only is this labor-intensive, but it’s also prone to mistakes. Missed deadlines or lapses in coverage can leave landlords vulnerable to hefty liability risks and unpaid repair costs.

On top of that, handling large amounts of paperwork - like PDFs and scanned insurance certificates - can easily overwhelm teams, especially when managing properties with hundreds of units. Staff often end up re-entering the same data into multiple systems, which adds to their workload and slows down leasing operations. Without automation, compliance checks are inconsistent, making it tough to monitor coverage in real time. This lack of efficiency can lead to higher labor expenses, delays in rent collection, and increased financial risks for landlords.