March 9, 2026

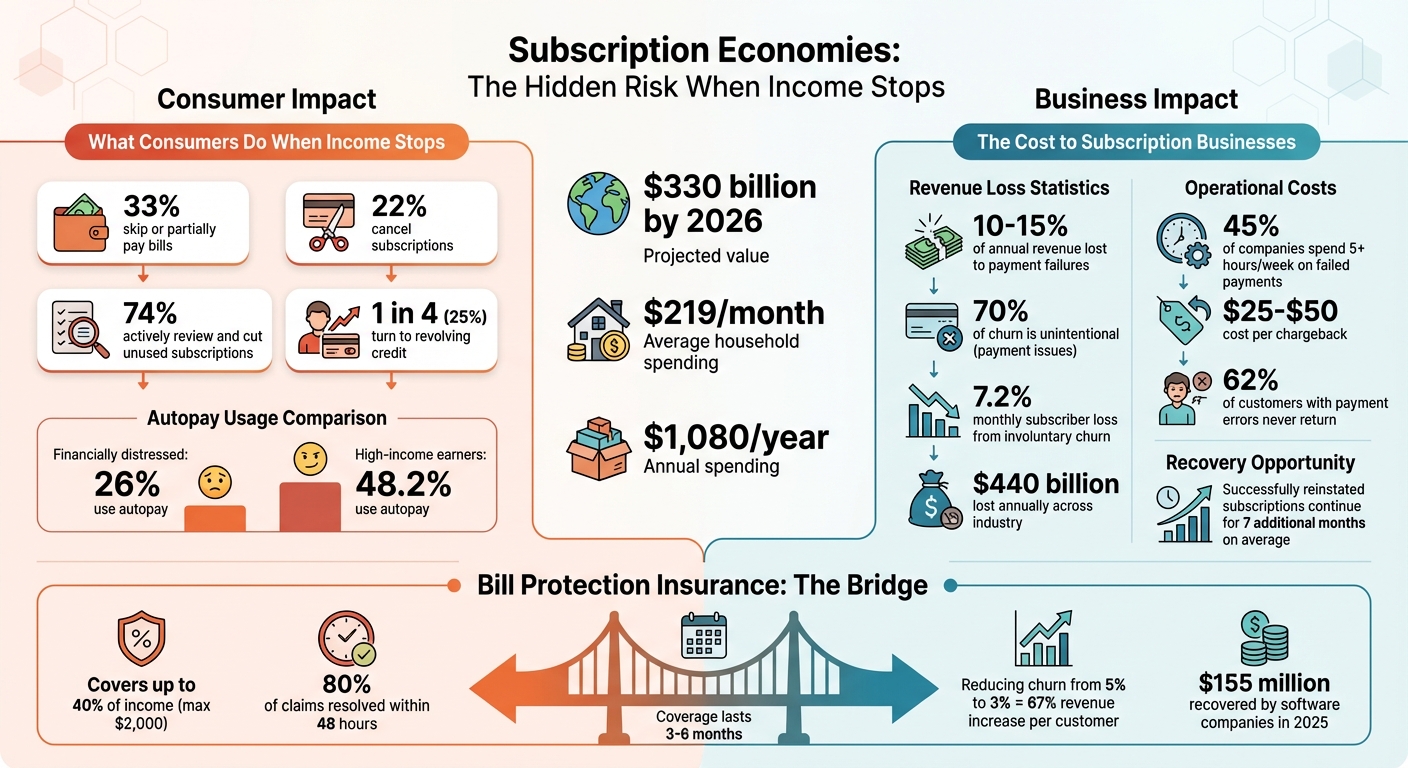

Recurring subscription payments can quickly become a financial burden when income stops. With the subscription economy projected to reach $330 billion in 2026, most households now juggle multiple services, spending an average of $219 monthly. While subscriptions offer convenience, they also create challenges when income becomes unpredictable due to job loss, illness, or reduced hours.

Solution: Bill protection insurance helps consumers maintain payments during income disruptions. It covers recurring expenses like subscriptions, utilities, and rent, providing short-term relief while stabilizing business revenue. As a technology enabler for embedded insurance, Walnut allows this protection to be integrated into subscription platforms, ensuring ensures payments continue during hardships, reducing customer churn and financial stress for both sides.

Subscription Economy Financial Impact: Consumer Behavior and Business Losses

When income vanishes, deciding which bills to cover becomes a juggling act. Experts describe this as a game of "financial whack-a-mole", where people reactively decide whether to pay bills fully, partially, or delay them until money becomes available [7].

The data paints a clear picture of the challenge. About 33% of consumers either skip or partially pay their bills, while 22% cancel subscriptions altogether. Considering that Americans typically spend $1,080 annually on subscriptions, it's no surprise that many are reevaluating these costs in tough times [4][7]. In fact, 74% of consumers are actively reviewing and cutting unused or unnecessary subscriptions to save money [4].

"When you're living paycheck to paycheck, you can't afford to have money pulled from your account on a fixed schedule - you need flexibility." - PYMNTS Intelligence [7]

Managing cash flow becomes a top priority during financial struggles. Many consumers avoid using autopay to prevent overdraft fees and maintain control over their accounts. For instance, only 26% of financially distressed individuals use autopay, compared to 48.2% of high-income earners [7]. Instead of formally canceling subscriptions, some adopt "passive canceling" strategies, like letting credit cards expire or turning off auto-renew options [4]. And when income dries up or unexpected expenses arise, nearly one in four consumers turns to revolving credit to make ends meet, often leading to long-term debt [6].

While consumers shift priorities to navigate financial challenges, subscription providers face their own set of obstacles, especially when it comes to lost revenue and customer retention.

As consumers struggle with payment issues, businesses feel the ripple effects, particularly in the form of revenue loss. Subscription services, for example, lose 10% to 15% of their annual revenue due to payment failures caused by expired cards or insufficient funds [10]. These aren't usually deliberate cancellations - nearly 70% of subscription churn is unintentional, stemming from payment issues rather than customer choice [2].

The financial toll doesn't stop there. Businesses spend significant time and resources addressing these problems. 45% of subscription companies dedicate five hours per week to handling failed payments, and chargebacks alone cost $25–$50 each. Worse, 62% of customers who encounter payment errors never return, cutting into their lifetime value [5][8][10].

"Involuntary churn is not a subscriber problem, it's an infrastructure problem." - Pelcro [9]

Involuntary churn can have a major impact, with businesses losing 7.2% of their subscribers each month if the issue isn't addressed [2]. However, there's hope for recovery - subscriptions that are successfully reinstated after an involuntary churn event often continue for an average of seven additional months [10]. This highlights that many customers still value the service but struggle to keep up with payments during financial hardship.

Bill protection insurance, often called "bill cover", is designed to safeguard recurring payments during periods of income disruption. Unlike traditional income protection, which replaces a portion of your overall salary, this type of insurance focuses solely on essential recurring expenses. These include rent or mortgage payments, utilities, subscription services, credit card payments, and other everyday costs that can pile up during tough times [11].

Coverage kicks in during specific life events, such as involuntary job loss, critical illness, disability, or even death [13]. Some newer policies have expanded to include additional situations, like public transportation disruptions or the need to care for an ill family member [11].

The payout structure depends on the policy. Standard bill protection policies usually cover up to 40% of an individual's income, with most capping payments at $2,000 for single coverage [12]. In comparison, traditional income protection policies cover a higher percentage - typically between 50% and 70% of pre-tax earnings - but come with higher premiums due to their broader scope [12].

Bill protection insurance simplifies the process of managing income disruptions. Signing up is straightforward - customers often enroll through their subscription service. If a qualifying event occurs, such as losing a job, they can file a claim directly through the provider’s app or website [11].

Modern policies use AI-driven systems to expedite claims processing. For instance, MIC Global reported that 80% of claims were resolved within 48 hours between May and December 2023 [11].

For job loss, coverage typically lasts up to three months, providing short-term financial relief [11]. For longer-term issues, like disabilities or illnesses, coverage may extend to six months, depending on the policy [13]. During this time, payments are made directly to service providers, ensuring subscriptions remain active while customers focus on recovery. This streamlined process also helps businesses by reducing subscription cancellations and stabilizing revenue streams.

"MiIncome is an embedded micro insurance product that is included as part of your company's existing digital platform or service... providing fast payments... so that they can concentrate on getting back to earning without financial worries."

- MIC Global [11]

For consumers, bill protection insurance provides much-needed financial stability during challenging times. It ensures uninterrupted access to essential services and reduces the stress of choosing which bills to prioritize. By tying the coverage to specific provider accounts, it also adds an extra layer of security [13].

For businesses, the advantages are equally compelling. Bill protection can generate new revenue streams through premium-sharing while reducing losses from unpaid bills. It also addresses involuntary churn, as customers who resolve past-due balances are five times more likely to accept protection offers [13].

The growing demand for such solutions highlights their importance. With 40% of North Americans showing interest in income protection and missed payments increasing by 46% since 2020, bill protection offers a practical way to keep customers connected even during financial disruptions [13]. By embedding this insurance into subscription platforms, businesses can provide seamless support while enhancing customer loyalty.

With income unpredictability on the rise, adding bill protection directly into subscription platforms can help stabilize both customer finances and recurring revenue streams.

Embedded bill protection weaves insurance into the customer journey. Businesses can now offer this protection at the point of signup or renewal, removing the need for customers to navigate to external sites.

API-driven solutions make the process smooth, handling quoting, application processing, premium collection, and policy documentation seamlessly [14]. Key components include APIs for Quotation, Proposal, Payment, and Documentation [14]. Together, these tools create a seamless experience that feels like a natural part of the subscription service instead of an external addition.

This integration tackles a major challenge for subscription businesses: failed payments. Providers lose about 9% of their annual revenue to payment failures, and 27% of subscribers cancel their service immediately after a payment failure notification [14]. By embedding bill protection that covers payments during income disruptions, businesses can avoid these losses. This creates a win-win for customers and providers, while setting the stage for flexible implementation methods tailored to various needs.

Subscription platforms can incorporate bill protection in three main ways, each catering to different levels of technical expertise and business objectives.

| Integration Type | Technical Requirement | Time-to-Market | Customization Level |

|---|---|---|---|

| No-Code Components | None | Days to weeks | Basic branding only |

| Data-Driven Referral | Light API setup | Weeks | Moderate customization |

| Headless API | Full API integration | Months | Complete control |

These options not only simplify implementation but also help reduce churn and strengthen customer loyalty.

Seamless integration of bill protection doesn’t just stabilize payments - it also significantly lowers involuntary churn and builds trust with customers. Payment failures, a leading cause of involuntary cancellations, account for up to 40% of total churn [9]. Bill protection ensures payment continuity, addressing this issue directly.

For example, in January 2026, a Recurly report analyzing 2,200 businesses revealed that automated recovery tools like intelligent retries and account updaters recovered $155 million for software companies and $100 million for digital media and entertainment firms [3]. Bill protection enhances these systems by covering payments when traditional recovery methods fail.

Offering this type of protection also shows empathy for customers' financial challenges. With 61% of subscribers reconsidering their paid subscriptions due to economic pressures [4], businesses that provide bill protection can foster trust and encourage loyalty.

"The subscription economy has entered a new phase. It is no longer defined by land-grab expansion but by operational discipline, lifecycle optimization, and strategic monetization." (Señal News, 2026) [3]

The operational advantages are clear. Automated protection reduces manual collection efforts, minimizes call center inquiries about billing issues, and eliminates the costs tied to repeated payment retries [14]. The revenue recovered through these systems is often seen as "pure EBITDA", as it secures recurring income without the expense of acquiring new customers [3].

The subscription economy faces a major challenge: involuntary churn, which leads to significant revenue losses. In fact, subscription companies lose an estimated $440 billion annually due to this issue [17].

One effective solution is bill protection insurance. While income disruptions like unemployment or disability can halt a customer's ability to pay, their bills don’t stop. By embedding protection into subscription services, payments can continue during these tough times. This not only helps customers maintain access to services but also prevents companies from losing valuable customer relationships and avoids the high costs of re-acquiring churned users.

The benefits go beyond just retaining customers - they’re measurable. For example, reducing monthly churn from 5% to 3% can increase revenue per customer by 67% [1]. Additionally, in 2025, automated recovery tools enabled software companies to reclaim more than $155 million in revenue that would have otherwise been lost due to payment failures [3].

"When brands support flexibility, customers come back when the value is there."

– Brian Geier, VP of Business Intelligence, Recurly [16]

Bill protection insurance is designed to cover specific recurring expenses, such as subscriptions or utility bills, during temporary financial setbacks. This ensures that essential payments are handled, helping you avoid late fees or service disruptions.

Income protection, however, steps in when you’re unable to work due to illness or injury. It provides a portion of your income over the long term, helping you manage everyday living costs.

While both types of insurance tackle financial challenges, they address different needs and situations.

To qualify for bill protection in cases of job loss or illness, you'll usually need to submit certain documents, like a termination notice from your employer or relevant medical records. The exact requirements can differ based on the provider's policies, so it's a good idea to review their specific guidelines for detailed instructions.

Bill protection takes care of paying your subscription and utility providers directly. If your income stops, this service ensures your bills are covered, so your essential services continue without you needing to handle the payments yourself.