June 1, 2026

Key takeaway: Higher interest rates have not reduced borrowing in the U.S. - instead, they’ve made defaults more costly for both borrowers and lenders. By Q1 2026, U.S. household debt hit $18.8 trillion, with credit card APRs averaging 23.4%, auto loan payments rising, and delinquency rates climbing across all debt categories. Borrowers face mounting financial strain, while lenders deal with increased charge-offs and portfolio risks.

Creditor insurance offers a safeguard by covering loan payments during life events like job loss or illness, preventing missed payments from escalating into defaults. Lenders benefit from reduced charge-offs, while borrowers gain a financial cushion during tough times.

Key benefits of creditor insurance:

How it works: Embedded creditor insurance integrates directly into loan applications or servicing platforms, offering borrowers tailored coverage options in real time. By addressing financial disruptions early, it helps stop defaults before they happen.

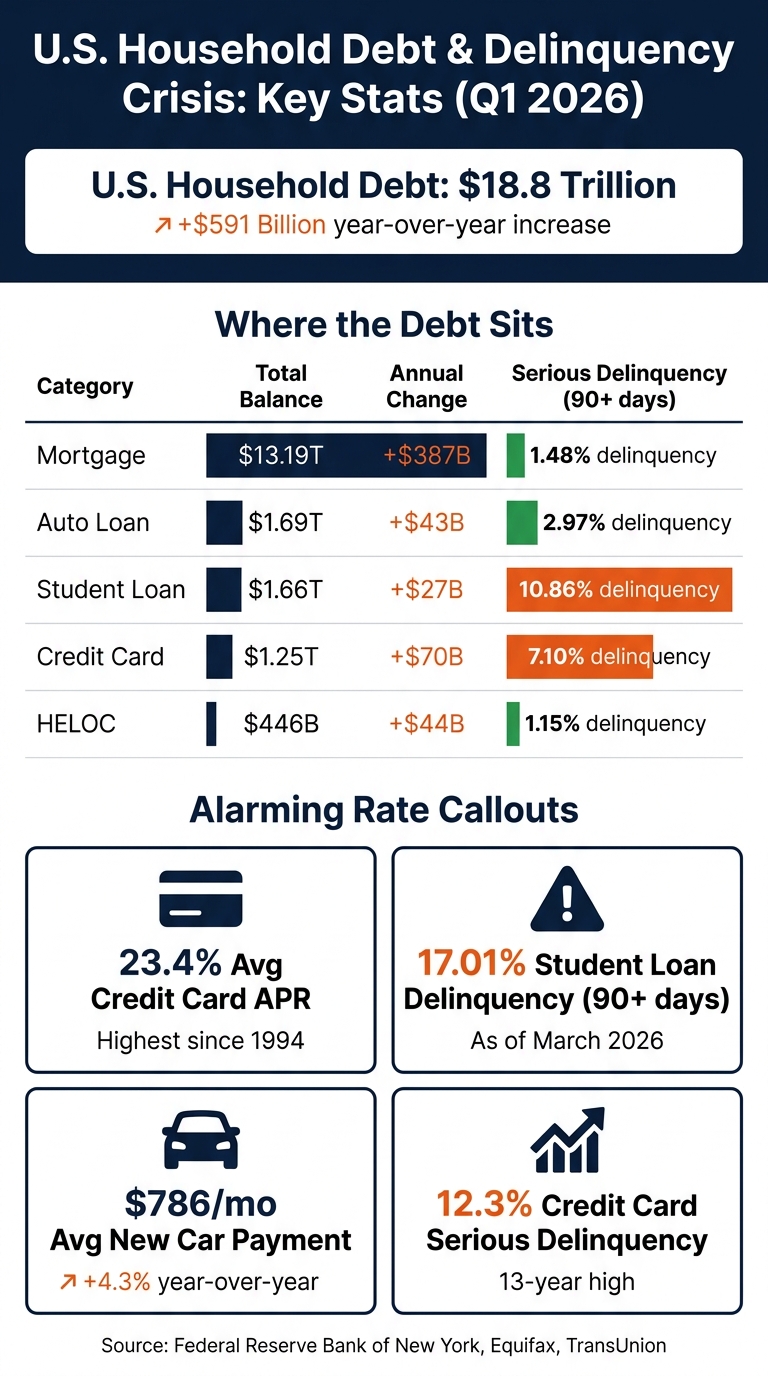

By Q1 2026, U.S. household debt had reached an eye-popping $18.8 trillion, marking a $591 billion increase compared to the previous year [1]. This growth wasn’t confined to one area - it spanned across mortgages, credit cards, auto loans, and home equity lines of credit (HELOCs). Mortgage balances alone grew by $387 billion, while credit card debt added $70 billion. Auto loans and HELOCs also saw notable jumps, rising by $43 billion and $44 billion, respectively [1][7].

Here’s a snapshot of where the debt stands:

Debt Category

Total Balance (Q1 2026)

Annual Change

Serious Delinquency (90+ Days)

Mortgage

$13.19 trillion

+$387 billion

1.48%

Auto Loan

$1.69 trillion

+$43 billion

2.97%

Student Loan

$1.66 trillion

+$27 billion

10.86%

Credit Card

$1.25 trillion

+$70 billion

7.10%

HELOC

$446 billion

+$44 billion

1.15%

Source: Federal Reserve Bank of New York [1]

This sharp rise in borrowing underscores how households are leaning on debt to manage their finances, even as interest rates remain high.

Despite climbing interest rates, borrowing didn’t slow down. Instead, it became a lifeline for many households. By mid-2024, pandemic-era savings had dried up, leaving the lowest two income brackets in the red when it came to liquid wealth [5]. With essentials like groceries and insurance still costing more, credit cards shifted from being a convenience to a necessity.

The numbers tell the story. Subprime bankcard originations jumped 18.6% year-over-year by early 2026 [2], and total credit limits hit a record $5.5 trillion in Q1 2026 [6]. Maria Urtubey, an advisor at Equifax, explained it well:

"Lenders originating more bankcard accounts for consumers in subprime while also increasing total credit limits suggests that, for the lower economic tier, credit may have moved beyond a financial tool and may be becoming a necessity for managing the rising costs of living."

This widespread reliance on credit has set the stage for growing financial strain, especially as interest rates remain steep.

Higher interest rates don’t just encourage borrowing; they also make it harder to keep up with payments. With the average credit card APR hitting 23.4% - the highest since 1994 [5] - carrying a balance has become a heavy burden. For example, a household with a $7,500 credit card balance now pays about $1,750 annually in interest before even touching the principal [5]. Combine that with rising auto payments, which now average $786 per month for new cars (up 4.3% year-over-year) [3], and it’s clear why budgets are feeling the squeeze.

The impact of higher rates isn’t distributed evenly. Between 2019 and 2025, the super-prime borrower population grew by 15 million [3], but near-prime and subprime borrowers saw their non-mortgage debt-to-income ratios climb sharply. Serious delinquencies paint an even starker picture: student loan delinquency reached 17.01% by March 2026 [2], and credit card delinquency hit a 13-year high of 12.3% [5]. These figures highlight a troubling reality: for many Americans, there’s little room left for financial missteps.

Missing a payment in a high-interest environment can quickly snowball into a heavier financial burden. Credit card APRs, which are tied to the federal funds rate, make delinquent balances grow at an alarming pace. For borrowers with lower credit scores, the situation is even worse. The interest rate spread for these individuals can climb as high as 21% above the federal funds rate[4], making it nearly impossible to catch up once they fall behind.

A lower credit score doesn’t just mean higher rates; it limits borrowing options to more expensive products, creating a cycle that’s hard to escape. For example, near-prime borrowers saw their non-mortgage debt-to-income (DTI) ratios rise by 176 basis points between Q4 2019 and Q4 2025. By comparison, super-prime borrowers only experienced a 29 basis point increase[3]. This shows how even a small financial misstep can trap borrowers in a cycle of increasingly costly debt, especially when interest rates remain high.

These rising costs for borrowers inevitably lead to greater risks and losses for lenders.

When borrowers struggle, lenders feel the impact through mounting losses. Credit card loans alone account for a staggering 53% of banks' annual default losses. For borrowers with FICO scores around 600, net charge-off rates can hit 9.3% annually[4], significantly affecting portfolios that are heavily weighted toward non-prime accounts.

Operational expenses only make things worse. Credit card operations cost lenders between 4% and 5% of their dollar balances annually. On top of that, marketing costs for credit card products are roughly ten times higher than for other banking services[4]. As charge-offs rise, these fixed costs remain constant, putting a squeeze on margins. This forces lenders to either tighten their underwriting standards or absorb the financial losses.

Maria Urtubey, an Advisor at Equifax, highlights the broader implications:

"For the financial system, the rising write-offs represent a necessary adjustment to bring risk levels back to a sustainable baseline."

And as noted by Itamar Drechsler and colleagues at the Federal Reserve Bank of New York:

"High rates reflect compensation for default risk that cannot be diversified away, either within the credit card market or across other lending markets in downturns."

Credit card default risk is systemic and unavoidable. When the economy weakens, charge-off rates increase across all credit tiers simultaneously. The systemic default risk premium for credit card lending is estimated at 5.3% annually[4]. This cost is ultimately passed back to borrowers through higher rates, worsening the cycle for everyone involved. These challenges highlight the importance of proactive measures, like creditor insurance, to help break the default cycle.

For decades, lenders have leaned on tools like underwriting models, risk-based pricing, and collections to manage risk. But these tools were designed for a different economic landscape. In today's environment of high interest rates and increased credit utilization, their limitations are becoming painfully clear.

The biggest issue? Timing. The Equifax Market Pulse Report highlights this challenge:

"Typically, delinquencies and write-offs move in tandem, however, the current data demonstrates more of a 'lagging indicator,' representing accounts that likely became delinquent months ago and have finally reached the point of being uncollectible."

In other words, by the time a delinquency is flagged, the damage is already done. Collections and write-offs deal with defaults only after they happen, making them inherently reactive.

Underwriting faces a similar problem. Under the CARD Act, interest spreads are locked in at origination, meaning they can't adapt to changes in a borrower’s financial health over time. As researchers at the Federal Reserve Bank of New York explain:

"In setting the interest spread on a card at the time of origination, banks must price in the account's default risk over its entire lifetime."

This approach assumes that a borrower’s financial stability remains constant, but recent trends among non-prime borrowers tell a different story. Financial stress is worsening, and traditional models aren't keeping up. Compounding the issue, lenders have long assumed that borrowers prioritize essential payments, like mortgages or auto loans. However, rising enforcement pressures across various categories are disrupting this hierarchy. For example, student loan delinquencies of 90+ days reached a staggering 17.01% in March 2026 [2], signaling that stress is spilling over into areas once considered stable.

To address these challenges, lenders need tools that can act in real-time, responding to life events before they spiral into defaults.

Standard risk tools are reactive by nature, which leaves lenders playing catch-up. What’s needed now is an approach that focuses on life events - events like job losses, medical emergencies, or sudden income disruptions - rather than static credit metrics at the time of origination.

Jason Laky, Executive Vice President at TransUnion, underscores the growing divide:

"As super prime consumers gain ground... many below-prime borrowers are taking on higher debt loads, increasing their reliance on credit and showing early signs of performance stress at a time when affordability pressures remain elevated."

This stress often appears suddenly, and by the time delinquencies are detected, defaults are already underway. Event-triggered solutions embedded within the lending process offer a way to break this cycle. These tools can activate support the moment a borrower encounters a financial disruption, intercepting the default chain before it begins.

In today’s high-rate environment, where the cost of defaults is soaring, relying solely on reactive tools is no longer sufficient. This is where creditor insurance comes into play - offering a proactive way to manage risk and protect both lenders and borrowers from the cascading effects of financial hardship.

Creditor insurance steps in to prevent defaults by covering monthly payments or paying off balances when specific life events occur. These triggering events often include involuntary job loss, disability, or death. The moment a financial disruption happens, the insurance kicks in, stopping a missed payment from spiraling into a default.

Another option is the debt cancellation or suspension agreement, which is structured directly between the lender and borrower. Unlike traditional insurance, these agreements allow debt to be paused or forgiven under certain conditions and are regulated as banking products.

By providing timely support during financial setbacks, creditor insurance safeguards borrowers while offering clear advantages for lenders.

For borrowers - especially those in near-prime and subprime credit tiers - the stakes are enormous. By late 2025, non-mortgage debt-to-income ratios for near-prime consumers climbed to 16.5%, marking a 176-basis-point rise from 2019 [3]. For individuals already balancing tight budgets, a single event like job loss or disability can tip the scales. Creditor insurance absorbs that shock, keeping accounts in good standing and shielding credit scores from the damage caused by missed payments.

This safety net is especially critical in an environment of rising household debt and higher default rates. For lenders, the numbers speak volumes. Net charge-off rates for borrowers with a 600 FICO score reached 9.3% annually [4], while credit card serious delinquency rates hit 12.3% in early 2026 - the highest since 2012 [5]. The financial impact of unchecked defaults is significant, but creditor insurance helps mitigate these risks by reducing charge-offs and stabilizing earnings, particularly during economic downturns when default risks surge across the board.

Consumer sentiment also supports the value of this product. In fact, over 85% of consumers who purchase debt protection view it as a "good idea" [8], highlighting the demand when the terms are clearly presented.

Beyond its financial benefits, creditor insurance strengthens trust and builds lasting relationships when implemented transparently. Regulatory scrutiny has been intense, largely due to past issues like hidden fees or auto-enrollment practices that eroded consumer confidence.

Today, the standard is clear: opt-in processes with plain-language disclosures that explain coverage upfront. The industry has also moved away from single-premium financed insurance - where the cost is bundled into the loan balance - and adopted Monthly Outstanding Balance (MOB) pricing. This method charges a small monthly fee based on the current balance, making costs more transparent and less burdensome for borrowers.

For lenders, compliance isn’t just about meeting legal requirements - it’s a way to stand out. Borrowers who fully understand their coverage and trust it will work when needed are more likely to stay loyal. Clear communication, easy opt-in options, and responsive claims handling set apart creditor insurance that earns trust from products that cause frustration.

Adding creditor insurance directly into the lending process ensures borrowers can access coverage when they need it most - without unnecessary hassle. This streamlined approach relies on API-driven integration, making the process smooth for both lenders and borrowers.

Walnut Insurance embeds creditor insurance right into the lending experience. By integrating at critical moments such as loan application screens, account onboarding, servicing portals, or even during hardship discussions, lenders can present insurance options at the exact time they’re most relevant - helping prevent defaults before they happen.

Through a quote and eligibility API, real-time coverage options are generated as soon as a borrower is approved. Using existing data like loan amount, term, borrower age, and state, the system provides tailored insurance offers. An enrollment API then finalizes the policy, linking it directly to the loan record. This process fits seamlessly into the lender's digital flow. Borrowers see an insurance offer alongside their monthly payment and can opt in without leaving the application process.

Integration Type

Technical Requirement

Setup Time

Brand Customization

Co-Branded Link Out

None

Less than 1 day

Basic (colors, logo)

Data-Driven Referral

Light API setup

1–3 days

Moderate (pre-filled data)

Headless API

Full API integration

Days to weeks

Complete (native experience)

Fintech partnerships with embedded insurance platforms have cut go-live timelines significantly. While traditional implementations could take 12–18 months, ready-made APIs, compliance tools, and carrier integrations can reduce that to just weeks or months.

The real advantage of embedded creditor insurance lies in its ability to connect with live borrower data and behavioral patterns. For example, if a borrower misses a payment or only makes a partial one, the system can automatically check for active coverage and send a message about claim eligibility - potentially stopping a 30-day delinquency from turning into a 90-day default. Similarly, when a borrower’s revolving balance spikes or they request a credit line increase, it’s a natural opportunity to offer or review coverage.

Employment data and payroll-integrated apps also play a key role. They can flag reduced hours or job loss in near real time, allowing lenders to proactively offer claims support before a payment is missed. Over time, this data feeds back into the lender’s risk models, improving pricing strategies, refining targeting efforts, and providing underwriters with valuable insights into how insured loans perform compared to uninsured ones. These dynamic adjustments not only enhance coverage outcomes but also simplify regulatory compliance challenges.

Regulatory complexity is one of the biggest hurdles lenders face when integrating insurance products. Licensing requirements, disclosure rules, consent processes, and monitoring across all 50 U.S. states can be daunting. Platforms like Walnut simplify this by offering pre-built disclosure templates, compliant opt-in flows, and audit-ready record-keeping - eliminating the need for lenders to build these systems themselves.

Additionally, Walnut connects lenders with over several insurance carriers, provides claims intake support, and offers analytics dashboards to track key metrics like attach rates, loss ratios, and claim causes. By taking on this operational burden, lenders can focus more on managing default risks and improving portfolio performance, even in high-interest rate environments, rather than worrying about compliance challenges.

Debt levels are climbing, and delinquencies are becoming more frequent, making the cost of default painfully clear. In the U.S., consumer debt remains sky-high, with delinquency rates reaching historic peaks. Add to that an average credit card APR of 23.4% [5], and the stakes for missing payments have never been higher. Borrowers haven’t slowed down their borrowing despite these rates; instead, every missed payment now comes with an even heftier price tag.

The problem with traditional risk management tools is that they’re reactive - they kick in only after delinquencies occur. Conventional approaches like FICO-based pricing or writing off bad debt happen too late to prevent losses. This lag underscores the need for solutions that act earlier in the process.

This is where event-triggered creditor insurance steps in. Unlike reactive tools, it works proactively, addressing potential defaults before they happen. Embedded creditor insurance provides coverage for borrowers facing unexpected challenges like unemployment, disability, or even death - before a payment is missed. For lenders, this means fewer charge-offs and a steadier portfolio. For borrowers, it’s a financial buffer that protects their credit and supports their families during tough times.

Walnut Insurance makes implementing this solution seamless. Using API-driven integration, lenders can embed this coverage into their digital platforms in just weeks. Walnut handles everything from connecting with insurance carriers to ensuring compliance across states and managing claims. In a market where auto loan write-offs have jumped by 27.5 basis points year-over-year [2], and credit card charge-offs range between 5.5% and 8.5% annualized [5], taking proactive steps is no longer optional - it’s essential for keeping portfolios stable and borrowers secure.

Higher interest rates make defaults more expensive for everyone involved. For lenders, the stakes are higher because they face bigger losses from charge-offs, recovery costs, and missing out on the expected interest income. On the other hand, borrowers feel the pinch through increased monthly payments, which can lead to late fees, hits to their credit scores, or even losing their collateral. In a high-rate environment, these issues amplify the financial strain defaults bring.

Student loans saw a sharp rise in delinquency during the first quarter of 2026. The percentage of loans overdue by 90 days or more climbed to 10.3%, up from 9.6% in the previous quarter. On a year-over-year basis, the situation worsened further, with serious delinquency flows increasing from 8.04% to 10.86%.

In contrast, other types of debt remained relatively steady. Mortgage delinquencies edged up slightly, moving from 1.4% to 1.5%, while credit card and auto loan delinquency rates either showed little fluctuation or small improvements. This highlights a growing divergence in how different types of debt are being managed.

Creditor insurance serves as a built-in safety net, stepping in to cover loan payments during tough times like unemployment, disability, or severe illness. It helps borrowers stay on top of their payments, shielding them from defaults and protecting their credit scores. At the same time, lenders benefit by avoiding the expenses tied to collections and charge-offs. By integrating this coverage directly into the loan process, it provides a layer of financial security for both parties.