March 4, 2026

When you use property management software, you’re likely focused on rent collection or maintenance - not insurance. But many platforms now integrate insurance directly into their workflows, offering renters and landlords policies at key moments like lease signing. This shift is powered by APIs, which automate tasks like verifying coverage and sending reminders, saving time and reducing errors.

For example, Rentec Direct identified 20,000 uninsured tenants in October 2025 and helped over 500 renters secure policies in just days. Platforms like Walnut Insurance make it easy to offer embedded insurance, providing flexible integration options, instant quotes, and new revenue streams for property managers. By contrast, older insurance models require manual processes and redirect tenants to external sites, creating a fragmented experience.

Embedded insurance is reshaping property management by simplifying compliance, improving user experience, and boosting revenue. With the market expected to grow from $128.6 billion in 2023 to $828.68 billion by 2030, this trend is set to redefine how insurance is delivered.

Walnut Insurance operates using an Insurance-as-a-Service model, designed specifically for property platforms that want to offer embedded coverage. They provide three ways to integrate:

The API-first approach ensures that insurance offers are triggered at key moments, like when tenants are signing a lease or moving in. Andrew Chau, Co-founder & CEO of Neo Financial, highlighted Walnut's modern approach:

"We're excited to partner with Walnut, bringing insurance into the digital age and creating greater access to protection for all Canadians. We've been impressed with how their infrastructure has been able to support us in growing our product offering"

.

For platforms that lack developer resources, Walnut's no-code solution allows them to launch a branded insurance program in less than a day [1]. This flexibility not only simplifies operations but also opens the door to new revenue streams.

Walnut makes it easy for property platforms to increase their revenue. By integrating insurance services, these platforms can double customer lifetime value [1]. The model is straightforward: platforms earn a margin on every policy sold through their system, creating a new income source without adding extra work. For landlords, Walnut offers embedded rent protection at about 5% of monthly rent, which helps cover missed payments for several months [2]. This is a far more affordable option compared to eviction costs, which can quickly add up to thousands of dollars in legal fees and lost rent [2].

Walnut connects with over 14 insurance carriers to provide a range of policies, including tenant, landlord, home, auto, and commercial insurance [1]. This variety allows property managers to tailor their offerings to meet the needs of their tenants, which can boost both adoption rates and tenant retention. As Walnut puts it:

"Evictions are expensive - embedded rent protection is cheaper"

.

Walnut’s approach makes insurance almost invisible to the end user. According to the company:

"The best embedded insurance products are the ones customers never have to think about"

.

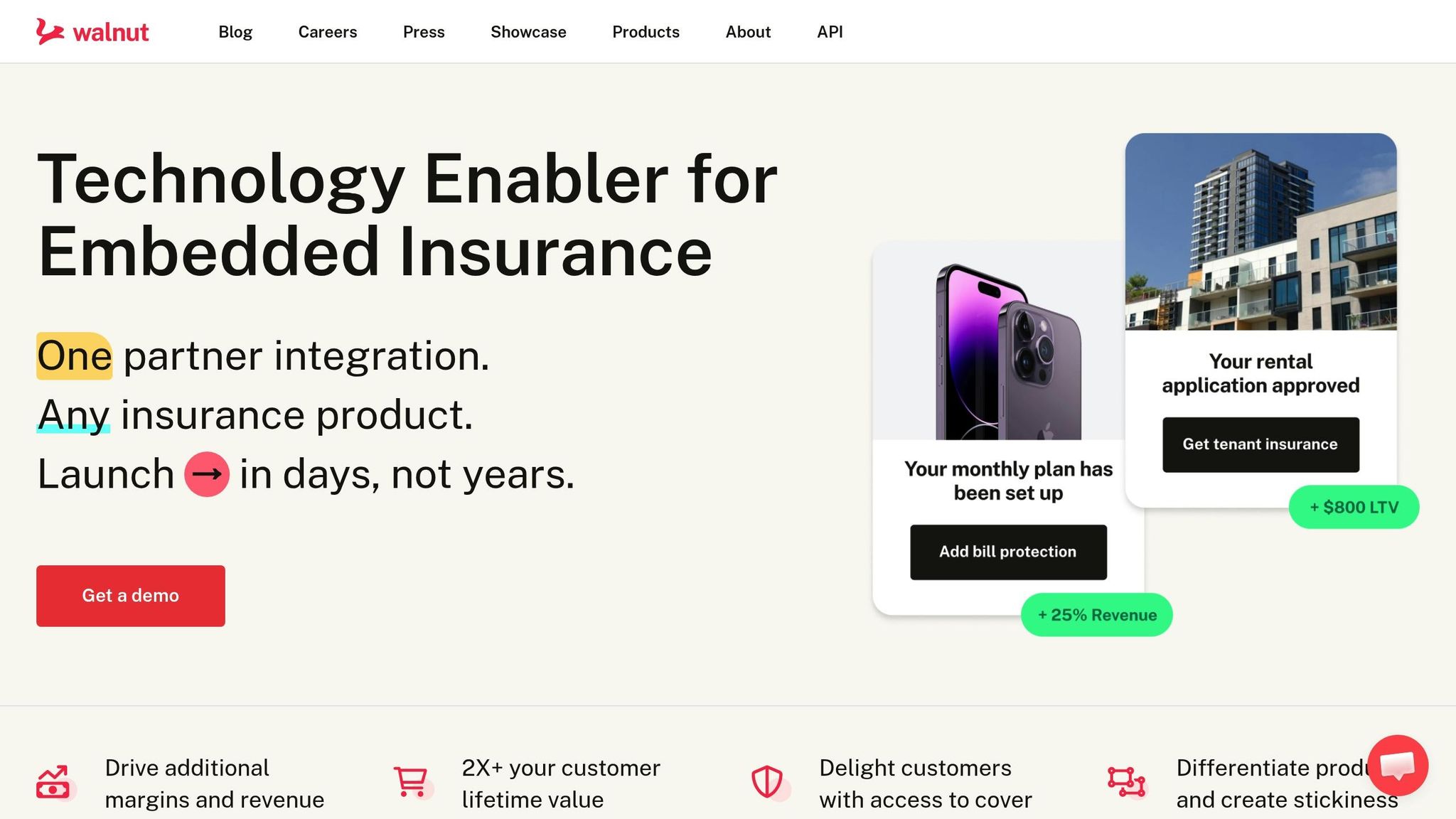

Instead of redirecting tenants to outside websites or requiring phone calls, insurance options are seamlessly integrated into resident portals or lease-signing workflows. Tenants can get instant quotes and secure coverage within minutes, all without leaving the platform they’re already using.

Walnut also takes care of the complicated parts, like compliance, licensing, and multi-channel broker support [1]. This means property managers don’t have to worry about navigating insurance regulations across different states. By embedding insurance into existing workflows, platforms see higher conversion rates because the offer appears at the exact moment tenants are most likely to act - when they’re signing a lease.

In traditional insurance, licensed agents and brokers are the go-to intermediaries for customers [3][5]. In the context of property platforms, this process remains a detached, standalone transaction. Instead of completing everything seamlessly within the platform, tenants or landlords are often redirected to a carrier's website or need to arrange a call with an agent [4].

This system relies heavily on outdated legacy systems that lack the capability to support modern API integrations [6]. These older methods stand in stark contrast to the more embedded insurance solutions that are reshaping property management today. Interestingly, while 92% of insurance executives agree that companies must evolve into "technology companies that happen to offer financial products", many standard distribution models are still stuck with infrastructure that prevents smooth integration [6].

The standard distribution model generates revenue primarily through one-time referral fees and commissions when customers are sent to an insurer. For producers, this means earning a single commission rather than enjoying the recurring revenue streams typically associated with embedded insurance models [5].

Independent agencies currently dominate about two-thirds of the commercial insurance market [5]. However, property platforms relying on standard distribution miss out on the potential for recurring commissions that embedded solutions can provide. This model often treats insurance as a price-driven commodity, rather than positioning it as a service that can strengthen customer relationships and boost lifetime value [6].

Unfortunately, this transactional focus also leads to a fragmented and less engaging customer experience.

Rather than simplifying real estate transactions, standard insurance distribution often adds unnecessary complexity [4]. For example, tenants are forced to exit their lease-signing process, fill out repetitive forms on external websites, and then wait for quotes instead of having access to immediate coverage options. This extra effort makes the insurance process feel disconnected from the property transaction itself.

The model prioritizes products over people, focusing on selling standardized policies instead of addressing specific customer needs as they arise [6]. While 90% of insurance executives believe success increasingly depends on participating in broader ecosystems rather than excelling as standalone entities, standard distribution continues to isolate insurance as a separate, inconvenient purchase [6].

When property platforms decide between embedded insurance gateways and traditional distribution methods, they shape the speed of integration, revenue potential, and overall user experience.

Deployment speed is a major differentiator. Embedded insurance gateways can integrate into digital platforms in as little as 30 to 90 days, while traditional methods often take years to implement [7]. Industry experts point out that API-enabled embedded solutions significantly outpace traditional digitization methods. These differences influence not only operational efficiency but also revenue models and user engagement.

The revenue model varies between the two approaches. Embedded gateways operate on a profit-sharing basis, removing upfront marketing expenses for partners [7]. In contrast, traditional distribution platforms rely on subscription fees or fee-for-service models, requiring ongoing payments regardless of actual insurance sales [8]. For property platforms, the ability to generate revenue without initial capital investment is a major benefit.

User experience is where the two models diverge most noticeably. Embedded solutions offer instant quotes and policy binding directly within the property platform, ensuring tenants and landlords remain within their familiar workflow [7]. Traditional distribution, on the other hand, forces users to navigate external administrative portals for tasks like licensing, renewals, and compliance tracking - steps that feel disconnected from the core property management process [8]. By integrating insurance into the existing workflow, the embedded approach enhances efficiency and keeps the focus on the property transaction.

Feature

Embedded Insurance Gateways (API-driven)

Traditional Distribution Models

API-driven, "headless", co-branded UI, or advisor-driven

Profit sharing; no upfront marketing costs

Subscription-based or fee-for-service

Instant quote and bind within the platform

Administrative portals for licensing and compliance

Automated processes via embedded infrastructure

Compliance-focused, emphasizing regulatory audits

Generating new revenue streams and boosting ARPU

Simplifying producer onboarding and ensuring compliance

Property platforms today face a pivotal decision: stick with traditional distribution channels or embrace embedded gateways. The embedded approach offers advantages like faster deployment, automated compliance, and instant quote-and-bind capabilities - all while keeping users within their existing workflows. On the other hand, traditional models often involve manual verification, separate portals, and fixed subscription fees, regardless of performance.

For platform operators, this decision hinges on balancing revenue goals with technical capabilities. Embedded solutions present a compelling case, potentially boosting revenue per user by 2x to 5x through profit-sharing models [10]. Case studies back this up: property platforms incorporating embedded banking and insurance services have seen customer lifetime values soar to 4x those of platforms without these features [10]. Additionally, some platforms have cut customer acquisition costs by 50% after implementing embedded solutions [10].

For multi-unit platforms grappling with insurance compliance, tenant liability waivers offer a streamlined solution. With 45% of U.S. renters still uninsured [11], these waivers provide 100% automatic compliance by integrating directly into leases. They typically cost tenants between $10 and $25 per month and can lower primary property insurance premiums by around 10% annually by mitigating resident-caused claims [11].

The embedded insurance market is on a steep growth trajectory, expected to expand from $128.6 billion in 2023 to $828.68 billion by 2030. By 2033, platform-based solutions could capture 15% of global gross written premiums, with the property and casualty sector potentially claiming up to 30% market share [9]. This marks a profound shift in how insurance is delivered - integrated seamlessly into property transactions rather than treated as an afterthought.

If seamless integration, automated workflows, and new revenue streams are your priorities, embedded insurance is the way forward. However, traditional distribution might still make sense for high-value or complex properties that benefit from expert consultation or for platforms with strong existing agent relationships. Walnut’s API-driven platform exemplifies how this evolution in insurance gateways is reshaping property management, improving tenant experiences, and enhancing operational efficiency.

Embedded insurance works by integrating directly into the lease-signing process via digital property management systems and rental platforms. This setup allows tenants to choose and purchase coverage, such as renter’s insurance, during the application process - without ever leaving the platform. Using APIs, these systems provide real-time quotes, handle policy management, and perform compliance checks. Features like automated policy verification and reminders simplify the process even further, cutting down on administrative tasks while ensuring smooth coverage for both tenants and property managers.

To quote and verify insurance coverage, property platforms must exchange crucial details, including tenant personal information and property specifics. They are also required to share policy data, such as its status, expiration dates, and coverage limits, to ensure everything stays compliant.

Additionally, securely storing insurance documents is a must. Automating notifications for policy updates or approaching expirations helps maintain accuracy while simplifying the entire process.

Platforms that facilitate property transactions often share revenue from various sources, such as insurance premiums, tenant fees, or additional services. A common example is earning commissions through embedded insurance, seamlessly integrated into processes like rent collection.

In this setup, platforms typically shoulder compliance responsibilities. This includes adhering to regulatory requirements, securely managing customer data, and ensuring transparent disclosures for users. To stay on top of these obligations, many platforms rely on automation tools and APIs, which help streamline compliance efforts and maintain regulatory standards within the U.S. market.