February 23, 2026

Property protection is being transformed by API-driven systems that integrate insurance, warranties, and rental protection into every stage of a property's lifecycle. The focus is on simplifying processes for businesses and consumers alike, from mortgage origination to ongoing maintenance.

Key insights:

For businesses, this means new revenue streams and better customer retention. For consumers, it means easier access to insurance, warranties, and rental protection without the hassle of traditional processes.

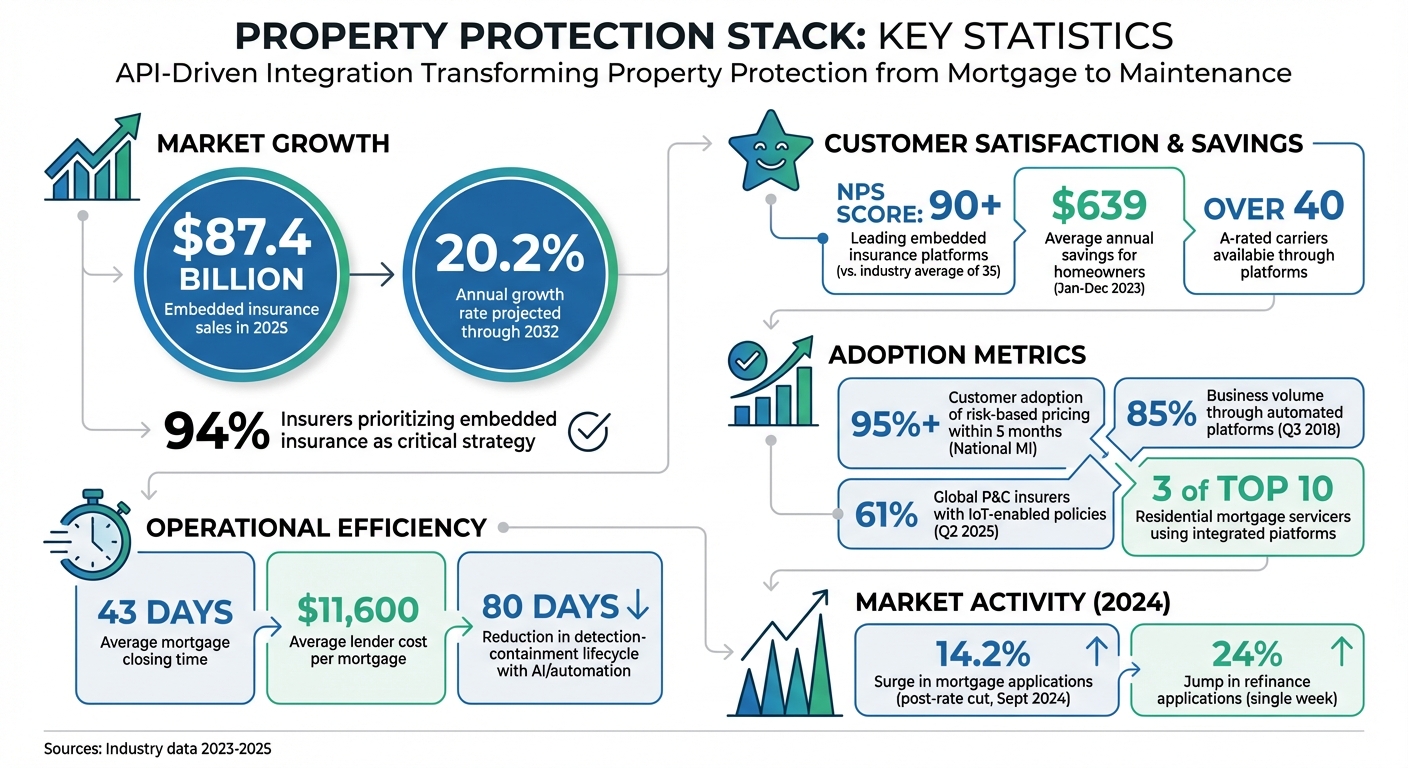

Mortgage insurance forms the backbone of the property protection stack, shielding lenders when borrowers make down payments of less than 20% on a conventional loan. In the past, obtaining quotes for private mortgage insurance (PMI) meant juggling multiple portals to input borrower data and compare rates. Today, API-driven platforms have streamlined this process, offering a single access point for all national MI providers. This shift in PMI integration is paving the way for similar advancements across the entire property protection lifecycle.

PMI now uses risk-based pricing models to generate quotes tailored to each borrower's specific credit profile, loan-to-value ratio, and property details [7]. National MI's introduction of its risk-based pricing engine, Rate GPS, saw rapid adoption - over 95% of customers embraced it within five months of its launch. By the third quarter of 2018, the platform accounted for about 85% of National MI's business [7]. These platforms now deliver instant, customized quotes across five standard product types - monthly MI, single premium MI, split premium MI, and lender-paid MI (LPMI) - with just a single click [5].

The technology doesn’t stop at quoting. It ranks options using "Best-Ex" logic to pinpoint the lowest costs for borrowers. Meanwhile, "Risk-Allocation" algorithms help lenders manage their exposure by spreading business across various providers [5]. Brad Finkelstein, Originations Editor at National Mortgage News, highlighted the benefits of these models, stating, "risk-based pricing on PMI may help lenders better compete for homebuyers with strong credit profiles, while rate-card pricing may lower costs for less creditworthy borrowers" [7].

API integration has brought MI quoting directly into loan origination systems like Encompass by ICE Mortgage Technology. This ensures consistent data flow, reduces closing delays, and automates detailed MI cost breakdowns to meet disclosure and regulatory standards - all while simplifying compliance [5]. Such seamless integration is setting the stage for broader innovations in property protection.

In 2019, National MI partnered with PMI Rate Pro to launch an API integration. Norm Fitzgerald, Chief Sales Officer at National MI, remarked:

"The platform's new API provides our lender clients with even more innovative, technology-enabled tools for ordering mortgage insurance. By reducing the time and costs associated with the mortgage process, our collaboration ultimately benefits consumers as well"

.

Today, three of the top 10 residential mortgage servicing companies use integrated insurance platforms to enhance borrower experiences throughout the mortgage lifecycle [4]. This development in mortgage insurance integration is part of a larger API-driven transformation, extending into homeowners insurance, warranty services, and the entire property protection ecosystem.

Homeowners insurance plays a key role in safeguarding both lender interests and borrower investments. In the past, insurance-related delays often disrupted closings and jeopardized deals. However, API-driven integration has changed the game, embedding insurance directly into loan origination systems (LOS). This shift has turned a once cumbersome process into a smooth step in the mortgage journey, speeding up closings and enabling real-time quoting and compliance automation.

By extracting key data from the LOS, platforms now pre-fill applications, eliminating the need for manual data entry [8]. Borrowers can compare quotes from multiple A-rated carriers side by side and bind policies without leaving the mortgage portal. This efficiency matters, considering the average mortgage takes 43 days to close and costs lenders around $11,600 - with insurance delays being a major contributor to those costs [2][8][9]. Between January and December 2023, Matic's embedded insurance platform helped homeowners save an average of $639 annually by pulling quotes from over 40 A-rated carriers [9].

Real-time quoting also ensures Debt-to-Income (DTI) accuracy. Late-arriving insurance estimates can lead to unexpected premium increases, potentially pushing borrowers over DTI limits and derailing deals during final underwriting. Instant quotes provide accurate premium data early in the process, avoiding these last-minute surprises. For example, following a rate cut in September 2024, mortgage applications surged by 14.2%, while refinance applications jumped by 24% in a single week, highlighting the growing need for automated processes [9]. Fast and precise quoting not only supports compliance efforts but also ensures regulatory standards are met without delays.

Embedded insurance solutions simplify compliance with regulations like GLBA and RESPA [2][8]. Platforms with jurisdiction-aware configurations automatically handle state-specific requirements and generate evidence of insurance (EOI) documents, which are then sent directly to lender operations teams [8]. This reduces the need for agent involvement and accelerates the clear-to-close timeline.

These systems also continuously monitor policies to prevent lapses, protecting both the borrower’s equity and the lender’s collateral while avoiding the high costs of lender-placed insurance [8]. Ross Diedrich, CEO of Covered, highlighted the importance of this shift:

"Embedded insurance is emerging as a strategic lever for forward-thinking lenders and servicers who want to unlock new revenue, improve the borrower experience, and future-proof their operations"

.

Leading embedded insurance platforms have achieved Net Promoter Scores (NPS) exceeding 90, far surpassing the insurance industry average of 35 [8].

While mortgage and homeowners insurance focus on protecting a property during the buying process, warranty services step in to cover everyday maintenance needs once the deal is done. After closing, homeowners often encounter surprise repair bills for essential systems like HVAC units or water heaters. Home warranties help cover these costs, ensuring major systems and appliances are repaired or replaced when they break down due to regular use - something standard homeowners insurance typically doesn’t handle. This added layer of protection addresses maintenance issues that traditional insurance policies leave out.

Home warranties function as service contracts that cover essential home systems and appliances like HVAC, plumbing, electrical systems, refrigerators, dishwashers, and water heaters when they fail from normal wear and tear [12][14]. Instead of paying the full repair cost upfront, homeowners pay a service fee ranging from $75 to $150 per visit [15][16]. On average, the annual cost for a home warranty is about $747, with monthly payments averaging $62.33 as of 2025 [13][16].

The home warranty market in the U.S. is expected to grow steadily, with annual increases between 4% and 7% projected through the early 2030s. This growth is fueled by homeowners seeking predictable repair costs [10]. Interestingly, more than half of home warranty purchases now occur directly through consumers rather than being tied to real estate transactions [10]. Modern home warranties are also evolving. By the second quarter of 2025, over 61% of global property and casualty insurers had adopted IoT-enabled policies. These policies use real-time data from devices like moisture sensors, leak detectors, and HVAC monitors to predict and prevent damage before it happens [11].

Adding warranties to a homeowner’s protection plan provides financial stability by replacing unpredictable repair bills with fixed costs. This not only benefits homeowners but also helps lenders by lowering the risk of loan defaults [3].

Thanks to API-driven technology for embedded insurance, mortgage companies can now offer home warranty options directly within their post-closing services. This seamless integration eliminates the need for homeowners to search for warranties separately, ensuring continuous coverage. As the Select Editorial Team explains:

"A home warranty is not just something you buy when selling or purchasing a home. It is a practical tool for homeowners who want predictable repair costs and protection for aging systems"

.

For property investors, rental protection is a step beyond standard homeowners insurance. Once a property is rented out, traditional coverage no longer cuts it. This is where landlord insurance policies, particularly DP-3 (Dwelling Fire Form 3) policies, come into play. These policies operate on an open-peril basis, covering all risks except those explicitly excluded [17][21]. While DP-3 policies typically cost about 20% more than standard homeowners insurance, they offer tailored protection that rental properties require [18].

DP-3 policies are designed not only to protect the physical structure of rental properties but also to address the unique financial risks landlords face. A key feature is Fair Rental Value coverage, which reimburses landlords for lost rental income if the property becomes uninhabitable due to a covered event, such as a fire or storm [17][19]. This coverage usually caps at 20% to 25% of the total dwelling coverage limit [19]. As Jeremy Layton, Web Marketing Lead at Steadily, explains:

"Loss of rent insurance isn't just useful - it's essential"

.

In addition to income protection, these policies include liability coverage to protect landlords' assets against legal judgments and medical expenses if a tenant or guest is injured on the property [17][18]. For those looking to guard against tenant non-payment, specialized rent guarantee insurance is available. This coverage specifically addresses lost income due to tenant default, separate from physical damage protection [19][20]. Modern API-driven platforms have even integrated rent protection products - typically costing about 5% of the monthly rent - into the leasing process. These tools help stabilize landlord income by covering missed payments for several months [3].

Beyond coverage, rental protection policies offer financial perks through tax benefits. All landlord insurance premiums are fully tax-deductible as ordinary business expenses on Schedule E (Form 1040), Line 9 [23]. This includes specialized policies like loss-of-rent, flood insurance, and umbrella coverage. Unlike personal residences, which are subject to the $10,000 SALT cap, property taxes on rental properties are deductible as business expenses with no such limitation [22]. Stessa highlights this advantage:

"Insurance premiums for rental properties qualify as a deductible operating expense because the IRS recognizes them as part of your routine costs as a rental real estate owner"

.

Additionally, Private Mortgage Insurance (PMI) on investment properties is entirely deductible as a necessary business expense, a benefit unavailable to primary residence owners [22]. These tax advantages help offset the cost of comprehensive rental protection, making it a financially sound choice for safeguarding cash flow and long-term asset value. Combined with API-driven solutions, these policies streamline property protection throughout the investment lifecycle.

The move toward unified property protection is being powered by modern APIs that bring together mortgage, homeowners, warranty, and rental protection into a single, cohesive system. These integrations simplify operations while ensuring compliance remains intact. As lenders and property platforms increasingly adopt embedded insurance, they face a critical choice: opt for no-code solutions for speed or headless API models for greater customization. This unified API strategy connects coverage from the start of the loan process through post-closing, reinforcing a seamless property protection framework.

No-code platforms offer quick, out-of-the-box integrations, making them ideal for rapid deployment within existing mortgage systems. These tools streamline implementation and create a smooth borrower experience without the need for custom development [26].

However, while no-code solutions are faster to implement, headless APIs provide deeper control, allowing businesses to tailor borrower experiences more precisely. For example, in 2023, Arch MI integrated its RateStar risk-based pricing tool with BeSmartee POS. This integration enabled mortgage insurance (MI) fees to be automatically populated into initial disclosure documents, which borrowers could view and sign electronically [25]. This bi-directional setup allowed lenders to access, monitor, and update data in real-time [28]. Led by Arch MI EVP Carl Tyree and BeSmartee co-founder Arvin Sahakian, this collaboration helped attract more borrowers with competitive rates while accelerating the closing process [25].

Headless APIs also support full lifecycle management by leveraging existing customer data to create coverage, retrieve detailed policy information, and handle cancellations through dedicated endpoints. This approach allows businesses to integrate protection products directly into their platforms while maintaining control over their branding. However, it does require additional development resources to manage API keys, headers, and endpoint integrations [24].

Expanding on these integrated models, multi-carrier access enhances competitive quoting while ensuring compliance throughout the property lifecycle. Platforms with access to over 65 carriers can offer borrowers personalized rates based on their risk profiles, financial situations, and bundling opportunities. For instance, bundling home and auto insurance can help reduce debt-to-income ratios [26]. These networks typically operate nationwide, with companies like Arch MI authorized to provide mortgage insurance across all 50 states, the District of Columbia, and Puerto Rico [25].

Compliance is embedded into the design of these platforms, adhering to state and federal regulations such as GLBA and RESPA. Features like internal controls, SOC 2 Type II certification, and alignment with CFPB guidelines ensure they meet the highest standards for settlement service providers and financial marketplaces [26]. For example, the Baldwin Group's Embedded Insurance platform offers a RESPA-compliant structure by combining carrier partnerships, advanced technology, and policy servicing expertise [27]. This robust setup enables continuous portfolio monitoring, escrow optimization, and prevention of lender-placed insurance, ultimately protecting borrower satisfaction while safeguarding lenders’ financial interests [26].

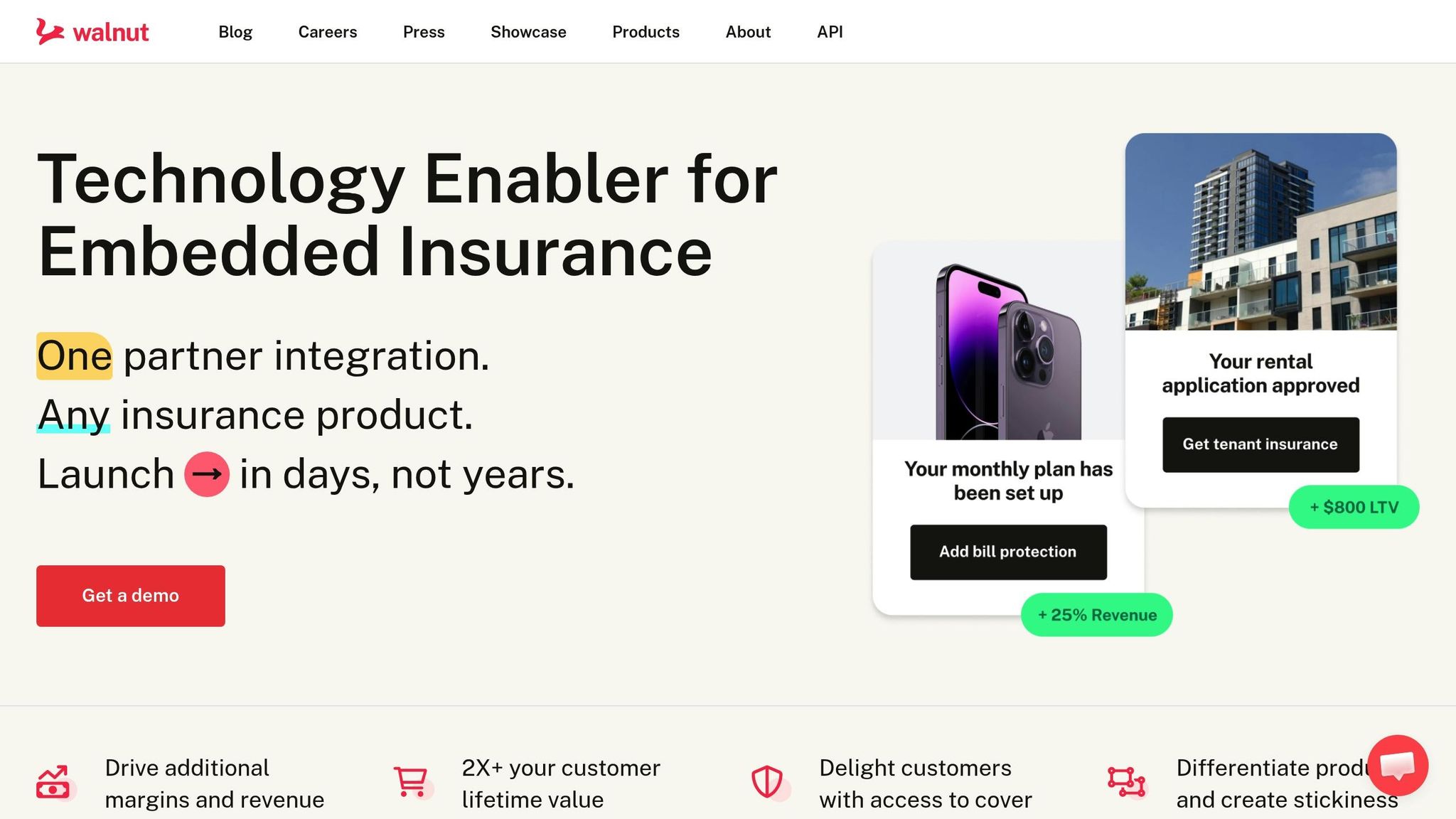

Walnut Insurance offers a platform that simplifies property protection, seamlessly embedding it into every stage of a property's lifecycle. By leveraging an API-driven approach, the platform integrates homeowners insurance, warranties, and other protection services directly into mortgage and property management systems. Built on a REST-based API using JSON and standard HTTP methods, this infrastructure allows businesses to incorporate insurance at any stage - from loan origination to ongoing maintenance after closing [30].

Walnut’s platform provides three integration tiers tailored to varying technical needs and business goals:

All integration models use a straightforward header-based API key (x-api-key) for authentication. This key is included in requests to access various protection products, including home warranties and digital protection [24][29].

"The

The platform supports complete lifecycle management, offering businesses a dynamic, efficient way to integrate insurance solutions [24].

Walnut connects businesses to a robust carrier network, streamlining access to over 14 carriers and more than 30 protection products across personal, commercial, and group insurance lines - all through a single integration [1][31]. This setup includes instant quote and bind functionality, allowing businesses to offer competitive rates without the hassle of managing individual carrier relationships. Walnut also handles licensing, compliance, and policy servicing, removing operational complexities for its partners [31].

One standout example is Neo Financial, a Canadian digital bank with over 1 million customers. Neo partnered with Walnut to embed insurance products, including credit card insurance, extended warranties, rental insurance, and mobile phone protection, into its platform. Andrew Chau, Neo’s co-founder and CEO, highlighted the value of this partnership:

"We're excited to partner with Walnut, bringing insurance into the digital age and creating greater access to protection for all Canadians. We've been impressed with how their infrastructure has been able to support us in growing our product offering."

Walnut’s platform demonstrates how businesses can rapidly launch comprehensive insurance programs while maintaining brand consistency. Covering everything from mortgage origination to post-closing protection, it offers a unified property protection solution that can be implemented in days rather than years [1][31].

Creating a seamless property protection system means strategically layering the right tools at each stage of the property lifecycle. For example, mortgage insurance and homeowners coverage are critical during loan origination, while home warranties and rental protection come into play after closing. The trick is to weave these products into existing workflows without disrupting them.

One way to achieve this is through API-driven integration, which removes the need for manual data transfers between systems. With a unified data stream, tasks like validating borrower income and credit can happen alongside generating homeowners insurance quotes and binding coverage. This not only reduces redundancies but also ensures compliance requirements are met without piling on administrative work.

Before adding new tools, businesses should focus on tightening up their current systems to reduce vulnerabilities. Consolidating fragmented solutions into a single platform can help avoid "tool sprawl." This is a growing problem - 69% of organizations that rely on more than 10 detection and response tools face increased security risks instead of reducing them [32]. A unified platform simplifies operations and sets the stage for dynamic, real-time monitoring.

Once the foundation is in place, real-time monitoring becomes essential for managing portfolio risks effectively. API endpoints can provide instant insights into portfolio coverage, eliminating the need for time-consuming manual audits [24]. For landlords managing multiple properties, embedded rent protection (typically around 5% of monthly rent) helps stabilize cash flow by covering missed payments for several months, reducing the financial strain of evictions [3].

Automation also plays a key role in lifecycle management, keeping track of important dates like start times, renewals, and cancellations across all types of coverage. For instance, incorporating creditor insurance at the origination stage can protect payments in cases of borrower job loss or illness. This proactive approach prevents defaults and shifts lenders from reactive collections to forward-thinking risk management [3].

Organizations leveraging AI and automation in their protection systems have seen impressive results, cutting the average detection-and-containment lifecycle by 80 days [32]. This tech-driven approach not only boosts operational efficiency but also strengthens the stability of entire property portfolios. With these practices in place, businesses can safeguard individual policies while reinforcing the broader property protection framework.

Property protection is shifting toward a seamless, integrated approach that spans every phase of ownership. This transformation goes beyond convenience - it's reshaping how businesses manage risk and how customers access the protection they need. With 94% of insurers identifying embedded insurance as a critical part of their strategy, the shift is well underway [3].

For businesses, this new model offers clear advantages: lower costs to attract customers, improved conversion rates, and fewer losses from defaults or evictions thanks to proactive risk management. For customers, it means immediate coverage without extra hassle, providing a safety net when unexpected challenges arise.

"Insurance isn't a product anymore - it's a feature hidden inside your payments." - Walnut Insurance

Walnut Insurance is leading this charge with its advanced API infrastructure and extensive carrier network, enabling quick and branded insurance integration. Its fully managed brokerage layer takes care of licensing, compliance, and broker-of-record responsibilities, removing the regulatory hurdles that often slow innovation. These tools mirror the API-driven strategies that have already modernized other aspects of the property lifecycle.

As AI continues to take over repetitive tasks and real-time risk adjustments become the norm, property protection will only become smarter and more efficient [3]. Companies that adopt API-first systems and use behavioral insights to guide their strategies will be better equipped to scale effortlessly as the industry advances. The future of property protection isn’t about selling more policies - it’s about minimizing risk and embedding financial security directly into the customer experience. From the start of a mortgage to ongoing maintenance, this integrated model signals a new chapter in property protection.

A property protection stack is a system designed to manage property-related risks at every stage of ownership or management. It combines mortgage insurance, homeowners insurance, warranty services, and rental protection into one cohesive solution. Powered by API-driven technology, this setup ensures smooth integration across services. The result? Simplified processes, better risk control, and the flexibility to adjust as needs evolve - offering property owners and managers a more efficient and convenient way to safeguard their investments.

Embedded insurance speeds up mortgage closings by automating the process of securing homeowners insurance. This automation cuts down on manual work and allows policies to be issued in real time, making it easier to meet tight closing deadlines. By simplifying these steps, it improves coordination among lenders, insurers, and buyers, ensuring a smoother process overall.

Homeowners insurance steps in to protect against unexpected events like fires, storms, or theft that might damage your home’s structure or personal belongings. It also includes liability coverage, which can help if someone gets injured on your property.

A home warranty, however, works differently. It’s essentially a service contract designed to cover the repair or replacement of major home systems and appliances when they break down from normal wear and tear - think heating systems, refrigerators, or plumbing issues.