December 31, 2025

Borrowing is changing fast in the U.S., and most consumers don’t even realize it. Payment protection insurance, once an optional add-on, is now being seamlessly included in loans, thanks to advanced technology and behavioral psychology. Here's why this matters:

While this approach simplifies borrowing, it raises concerns about transparency and choice. The shift is reshaping lending, making protection automatic and almost invisible to borrowers.

The lending industry is shifting gears from the old-school "Would you like to add protection?" checkbox to a more seamless approach. Now, payment protection is integrated directly into the loan application process, often so smoothly that borrowers might not even notice it. This transformation is driven by behavioral economics and advanced API technology, making protection feel like a natural part of borrowing rather than an extra add-on.

One key factor at play here is default bias - a psychological tendency where people are more likely to stick with pre-selected options. When protection is automatically included, customers don’t need to opt in - it’s already there. And the stats are telling: 83% of lenders serving consumers now offer at least one embedded lending product[5], while 47% of lenders globally focus solely on embedded lending[5]. This is no passing trend; it’s quickly becoming the norm.

Modern API-driven platforms are revolutionizing how underwriting decisions are made. By using real-time data like credit scores, transaction histories, and behavioral insights, these platforms eliminate the need for clunky, multi-step processes[6][7]. A standout example is the partnership between Root Insurance and Carvana in July 2022. They embedded auto insurance into the vehicle checkout process, allowing customers to skip tedious data entry. With pre-filled customer information and their "Coverage in 3 clicks™" feature, the process became effortless[1]. Alex Timm, CEO of Root Insurance, explained it best:

Talking to consumers at the time when they really need insurance - like when they're purchasing a vehicle - is a lot better customer experience than being bombarded with advertisements

.

And the impact? Embedded lending solutions have been shown to boost checkout conversion rates by 20% to 30%[6]. Plus, customers using these solutions in retail settings spend 20% more per visit compared to those who don’t[6]. Platforms like Walnut Insurance are leading the charge, offering API integrations that let lenders embed protection without massive technical overhauls. Whether it’s through a co-branded link or a fully headless API, lenders can now provide coverage exactly when borrowers need it. What was once a cumbersome, separate process is now a smooth, effortless part of the lending experience, paving the way for Walnut Insurance's refined embedded solutions.

Walnut Insurance uses an API-driven method to seamlessly incorporate payment protection into lending platforms. This approach allows lenders to integrate the service without making major changes to their existing systems. By leveraging real-time decision-making algorithms, the platform analyzes data like transaction histories and user behavior to provide instant feedback directly within the lender's interface. This ensures borrowers can stay within the loan application process, avoiding the hassle of navigating to external websites or separate applications[9][7].

To cater to lenders of all sizes, Walnut offers three integration options:

This tiered system makes it easy for even smaller lenders with limited IT resources to get started, ensuring a smooth and efficient integration process.

Walnut Insurance prioritizes a seamless borrower experience by keeping the entire process within the lender's platform. Borrowers benefit from an interface that mirrors the lender’s branding, including logos, colors, and overall visual identity. Pre-filled data fields further simplify the process, reducing the need for manual input and speeding up completion times[8][10].

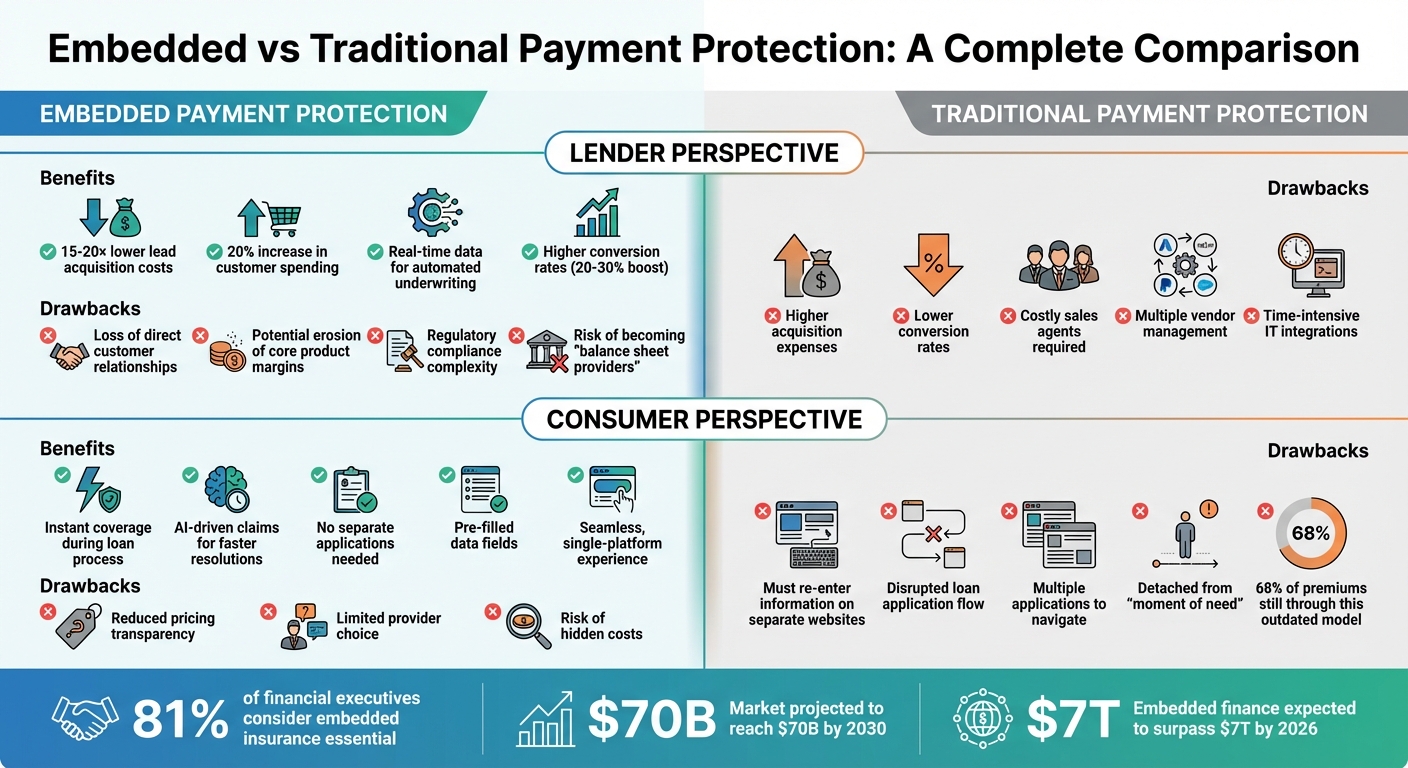

Traditional payment protection models operate quite differently from modern embedded solutions like Walnut. These older systems keep protection services separate from the loan application process, relying heavily on manual steps and lengthy bank approvals[12]. Borrowers are often redirected to external platforms to complete additional forms, creating a fragmented and cumbersome experience[13]. For lenders, this setup involves juggling multiple vendors and enduring time-intensive IT integrations. Insurance in these systems exists as a standalone product, detached from the loan journey, which causes friction at nearly every step - from obtaining quotes to finalizing policies. This disjointed approach often leaves borrowers frustrated and slows down the overall process.

Borrowers using traditional models face significant hurdles. They must re-enter their information on separate websites, disrupting the flow of their loan application. This interruption contrasts sharply with the ease of embedded solutions, where everything is integrated into a single platform.

Currently, 68% of U.S. auto insurance premiums are still generated through direct-to-consumer sales or exclusive agents[1]. This outdated approach keeps insurance detached from the critical "moment of need" during the loan process. As a result, borrowers are left to navigate multiple applications and vendor relationships, adding unnecessary complexity to their experience.

The inefficiencies of traditional models come with a financial cost. Poor integration leads to higher acquisition expenses and lower conversion rates[2][4]. Borrowers often drop off during the cumbersome sign-up process, resulting in lost revenue opportunities[13]. Additionally, these systems rely on costly sales agents, separate marketing efforts, and standalone platforms, all of which drive up distribution costs[3].

Embedded solutions, on the other hand, streamline these processes and achieve higher attachment rates for the same products. Traditional models fail to capitalize on presenting protection options contextually within the loan journey, forcing lenders to spend more on marketing for fewer results. These inefficiencies highlight why many lenders are moving toward integrated solutions to maximize revenue and improve customer retention.

Compliance is another area where traditional models struggle. Regulatory requirements demand that non-financial sellers obtain licenses in each state, creating additional administrative burdens and delaying market entry[1]. Regulators also keep a close eye on these systems to ensure pricing transparency and prevent borrowers from feeling pressured into purchasing protection to secure better loan terms[1].

Moreover, the shared-responsibility model for compliance means lenders must manage data protection, privacy issues, and consumer complaints in partnership with their insurance providers. These added complexities increase operational costs and make it harder for lenders to adapt to regulatory changes quickly. All of these factors combine to make traditional models less efficient and less appealing in today’s lending environment.

Embedded payment protection is reshaping how lenders and consumers experience loan-related coverage by seamlessly integrating it into the borrowing process. This shift brings a mix of advantages and challenges for both parties.

For lenders, the benefits are clear. Acquisition costs can drop significantly - up to 15–20 times lower than traditional methods [6]. Additionally, embedded payment protection can lead to a 20% boost in customer spending [6] and improve underwriting accuracy with real-time data [6][12]. But it’s not all upside. Lenders risk losing direct relationships with customers, as platforms often take ownership of the customer experience, leaving lenders as mere "balance sheet providers" [1][2]. There’s also the potential for cannibalization of high-margin core products [2], and navigating regulatory compliance can add complexity [1][15].

For consumers, the convenience is undeniable. Coverage is offered exactly when it’s needed, right during the loan process, eliminating the hassle of separate applications. AI-powered claims processing speeds up resolutions, building trust in the primary brand. However, this streamlined approach can come with downsides. Pricing details and terms may become less transparent, limiting consumers’ ability to make fully informed decisions. Additionally, a poor claims experience with the embedded provider could harm the lender’s reputation [1].

Here’s a quick breakdown of these benefits and drawbacks:

15–20× lower lead acquisition costs

Loss of direct customer relationships

Instant coverage during the loan process; AI-driven claims for faster resolutions; no need for separate applications

Reduced pricing transparency; limited choice of providers; risk of hidden costs

The regulatory environment adds another layer of complexity. A recent study found that 81% of financial executives now consider embedded insurance essential rather than optional [11]. However, 42% of companies cite transparency and flexibility as major challenges during implementation [14]. For non-financial partners, like auto dealers, compliance with state-specific insurance licensing requirements can be another hurdle [1].

As embedded finance is expected to surpass $7 trillion by 2026 [12] and embedded insurance could reach $70 billion in gross written premiums by 2030 [15], it’s clear that this model is transforming the lending landscape. While the trade-offs are significant, they highlight the ongoing evolution in this space - a topic we’ll delve into further in the conclusion.

Embedded payment protection has become a cornerstone of modern lending. A striking 81% of financial executives consider it essential, and predictions suggest embedded finance will account for 20–25% of all retail and SME lending by 2030, up from the current 5–10% [6][11]. Lenders are drawn to this model for its significantly lower acquisition costs - 15 to 20 times cheaper than traditional methods [6] - and are using tools like automated underwriting and additional revenue streams to offset shrinking interest margins.

For lenders, the benefits include reduced costs and higher conversion rates, though these come with a trade-off: a weaker direct relationship with customers. On the consumer side, the experience is almost effortless. The protection is offered as a simple yes-or-no decision, often with pre-filled data, making the process seamless [11]. However, this ease of use can sometimes sacrifice transparency and limit choices. As Amy McNeece, Senior Vice President of Digital Consumer Partnerships at Chubb, notes:

The gist of embedded insurance is that it's often an easy yes-or-no choice

.

This seamless integration often goes unnoticed by consumers, as it’s built directly into the loan application process. Without extra forms or additional steps, it feels like a natural part of the transaction. This design taps into behavioral economics, reducing the "pain of paying" and making bundled offerings more appealing. It’s a stark contrast to outdated methods, as highlighted earlier with Walnut Insurance’s streamlined approach versus more fragmented alternatives.

The market’s response speaks volumes. Embedded insurance sales reached $87.4 billion, growing at an annual rate of 20.2% [3], with U.S. sales alone projected to hit $70 billion by 2030 [1]. Alex Timm, CEO of Root Insurance, emphasizes the advantage of this timing:

Talking to consumers at the time when they really need insurance - like when they're purchasing a vehicle - is a lot better customer experience than being bombarded with advertisements

.

With standardized APIs enabling nearly cost-free integration [6][15], this model is becoming increasingly irresistible to lenders.

The embedded approach is set to dominate the industry, offering a win-win for both lenders and consumers. Its ability to integrate protection seamlessly into the lending process - while remaining useful and fairly priced - may be its greatest strength.

Embedded payment protection is often built directly into loans or credit products, sparing consumers the need to manually opt in. While this setup can make financial protection easier to access, it also means borrowers might miss the chance to actively review or decline the coverage. In fact, many people may not even realize this protection is automatically included.

For lenders, this approach simplifies the process and boosts adoption rates, but it can come at the expense of transparency. Key details - like policy terms, exclusions, and costs - may not be clearly highlighted, leaving borrowers unsure about what they’re paying for or what the coverage actually offers. So, while embedded protection adds convenience, it may also limit borrowers' ability to make fully informed decisions.

Embedded payment protection brings several advantages to lenders. For starters, it can cut charge-off and default losses by about 20%, which directly boosts the performance of lending portfolios. On top of that, it helps improve borrower satisfaction and loyalty, making it easier to attract new customers and keep existing ones, all while reducing acquisition and abandonment costs.

By seamlessly integrating protection into the lending process, lenders offer extra value to borrowers without interrupting their experience. This creates a mutually beneficial arrangement for both lenders and borrowers.

Most borrowers may not even realize they're getting payment protection because it's built right into the loan process. Instead of asking borrowers to opt in separately, this protection is often automatically included, making it less apparent during the application.

On top of that, many people don’t fully understand how embedded payments function, so they might not notice that their loan comes with additional coverage. This setup is designed to make the process smoother and easier, but it can also leave borrowers unaware of the protection they’re benefiting from.