May 11, 2026

Here’s the problem: Most income disruptions for Americans last less than 90 days, but current insurance products don’t cover these short-term gaps. Instead, they focus on long-term or catastrophic events, leaving many households unprotected when they face temporary income loss due to medical leave, reduced hours, or layoffs.

Key facts:

The solution: Short-term income protection fills this gap by offering quick payouts for income losses under 90 days. These products are integrated into banking and lending platforms, making them easy to access when people need them most. Companies like Walnut Insurance are leading the way by embedding these solutions directly into financial tools, offering coverage for as little as $3–$10 per month.

With over 50% of consumers showing interest in income protection, embedded insurance is reshaping how financial safety nets are delivered.

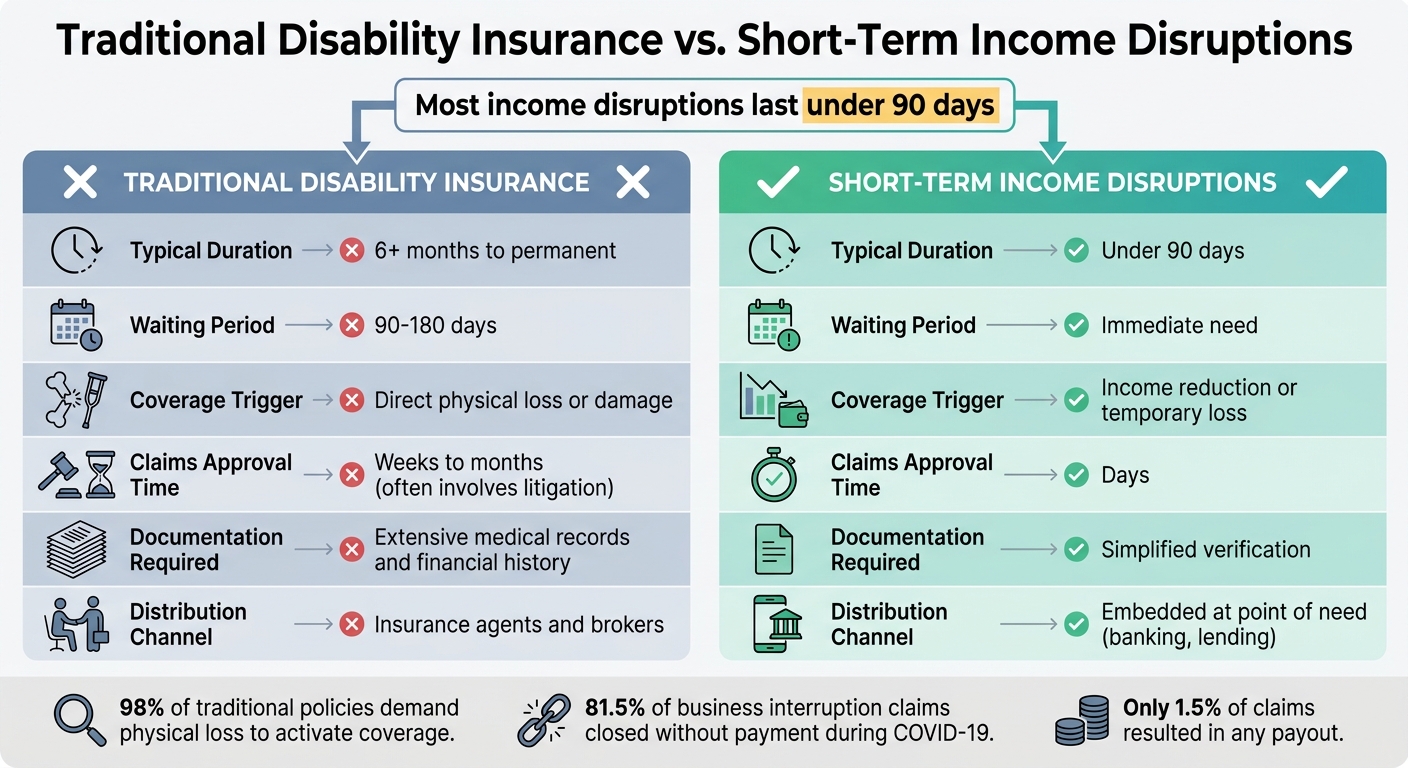

Traditional income protection products are built to handle long-term, catastrophic events, but they often leave people unprotected when it comes to short-term income disruptions. Since most income interruptions last less than 90 days, these products don't align with the financial realities many face today. Let’s break down why these gaps exist.

Traditional disability insurance is essentially useless for short-term needs. Policies typically come with elimination periods of 60 to 180 days. This means you have to wait that long before benefits kick in - acting as a time-based deductible.

On top of that, these policies have rigid definitions of what qualifies as a claim. They often require a direct physical loss, which excludes many common disruptions like mandatory closures or illnesses that don’t require hospitalization. James Lynch, Chief Actuary at the Insurance Information Institute, explains:

"The standard business interruption policy only applies when the business sustains direct physical loss or damage, such as a fire"

.

In fact, 98% of traditional policies demand physical loss to activate coverage [2]. For workers dealing with non-physical disruptions, this means no payout and no safety net.

Even beyond coverage limitations, the claims process for traditional income protection is slow and overly complicated. These policies require substantial documentation, including financial records, medical certifications, and income projections, to justify a claim [1]. This bureaucracy delays payouts at a time when people need cash urgently.

Take the COVID-19 pandemic as an example. U.S. insurers received 201,285 claims for business interruption losses. Of those, 164,178 claims - about 81.5% - were closed without payment. Only 3,001 claims, or roughly 1.5%, resulted in any payout [2]. Virus exclusions and physical-damage requirements often blocked even valid claims [2].

Feature

Traditional Disability Insurance

Short-Term Income Disruptions

6+ months to permanent

Under 90 days

90–180 days

Immediate need

Direct physical loss or damage

Income reduction or temporary loss

Weeks to months (often involves litigation)

Days

Extensive medical records and financial history

Simplified verification

Insurance agents and brokers

(banking, lending)

This table drives home the mismatch. Traditional disability insurance operates on timelines and criteria that simply don’t align with the realities of short-term income disruptions. These products aren’t built to address the immediate and more common financial challenges people face today.

A recent survey revealed that by the end of 2025, 66.6% of consumers were living paycheck to paycheck, with only 48.5% confident they could handle a $1,000 unexpected expense. Among those already struggling with bills, that confidence plummeted to just 22.4% [5]. This paints a stark picture: even brief income disruptions can create immediate financial strain.

The focus here isn't on long-term or catastrophic disability but rather on 30-, 60-, or 90-day interruptions - situations that happen far more often. Think of a short illness, a temporary business closure, or a brief medical leave. As PYMNTS Intelligence put it, “Small financial shocks now hit with the force of a crisis because there is little room left in the monthly budget” [5].

Short-term income protection steps in to provide quick liquidity, preventing temporary setbacks from escalating into long-term financial problems like high-interest debt or drained retirement savings. Research from Vanguard highlights this point: having just $2,000 in accessible savings can improve financial well-being by 21% [6]. This underscores the importance of short-term income protection in building financial resilience, addressing a growing need for tailored solutions in this space.

The demand for short-term financial safety nets is growing, as unexpected financial emergencies continue to disrupt households.

Labor market data sheds light on this reality. Over 50% of workers in hands-on roles - such as warehouse employees, delivery drivers, and retail staff - needed to access their earnings to cover essential expenses within the past 90 days. Even more striking, one in six workers faced cash shortfalls four or more times per quarter [7]. These stats highlight a cycle where critical expenses often outpace income.

Small businesses are no exception. In a 2024 survey, 31% of respondents named business interruption as a top global threat [1][2]. However, only 30% to 40% of small business owners carry business interruption insurance [2]. Even when they do, these policies often require direct physical damage to activate benefits. With standard coverage kicking in only after 30 days [1], traditional products fail to address the critical, short-term challenges businesses face.

Traditional insurance products often suffer from slow and disconnected processes, leaving many consumers frustrated. Embedded insurance offers a more direct and seamless alternative, addressing these challenges head-on. By integrating insurance into financial platforms like banking apps and lending portals, it becomes a natural part of the user experience.

Here’s how it works: when someone opens a bank account, applies for a loan, or activates a new financial product, API-driven enrollment can automatically trigger. This eliminates the need for separate forms or additional approvals. Coverage kicks in right when users are focused on their financial stability, making it incredibly timely and relevant.

Why does this matter? A recent fintech survey revealed that over 50% of consumers are interested in this type of protection. However, many shy away from traditional insurance policies because the process feels too complicated or disconnected from their immediate needs. By embedding income protection directly into financial workflows, platforms can deliver "relevant protection" at key moments - like when users are managing credit, dealing with income uncertainty, or making significant financial decisions [8].

Platforms have flexibility in how they implement this integration, depending on their technical capabilities. Some opt for fully embedded models, where insurance is seamlessly built into product plans. Others use headless integrations, which allow full control over the customer experience, or co-branded purchase flows, which require minimal technical effort for faster deployment. Opt-in premiums typically range from $3 to $10 per month, while fully embedded solutions often come at even lower rates [8].

This approach not only simplifies the user experience but also sets the stage for a more efficient, tech-driven infrastructure.

The integration benefits of embedded insurance are amplified by API-driven technology, which enables rapid scaling. Modern platforms take a developer-first approach, using straightforward API integrations that allow financial institutions to maintain control over the customer journey without disruptive handoffs. Real-time data analytics further enhance the experience by personalizing coverage to meet individual needs [3].

APIs do more than just streamline enrollment - they also power instant quotes and policy bindings while drastically reducing claims processing times. What used to take 48–72 hours can now happen almost instantly [9][1]. For financial platforms, embedding income protection isn’t just about convenience; it’s a strategic move that adds significant business value. It differentiates their offerings, improves customer retention, and boosts lifetime value.

When insurance feels like a natural part of the service rather than an optional add-on, conversion rates go up, and customers stay engaged for longer periods. This combination of seamless integration and advanced technology is transforming how income protection is delivered, making it more accessible and effective than ever before.

Walnut tackles the gap between traditional insurance coverage and short-term needs by embedding income protection directly into users' digital financial routines. By leveraging the benefits of embedded insurance, Walnut offers three integration options to suit different partners: Co-Branded Link Out, Data-Driven Referral Link, and Headless API. These options allow banks and lending platforms to seamlessly incorporate income protection without requiring major infrastructure changes.

Walnut’s integration models are designed to meet varying partner needs:

Monthly premiums for opt-in models typically range between $3 and $10, while fully embedded solutions can often be delivered at even lower costs [8]. These options make it easy for digital financial services to integrate income protection seamlessly into their offerings.

Walnut partners with over 14 insurance carriers, offering instant quote and bind capabilities that eliminate the delays common with traditional disability insurance. The platform supports compliance for partners in the U.S. and Canada. Coverage includes involuntary job loss, disability due to chronic illness or accidents, critical illness, and life insurance, providing comprehensive protection against short-term income disruptions [8].

Walnut’s embedded approach enhances Lifetime Value (LTV) by helping partners stand out with timely income protection options. The Headless API maximizes conversion rates through a seamless customer experience and integrated billing, while the Co-Branded Link Out offers a quick way to gauge demand. With over 50% of consumers showing interest in income protection, adding this feature enables platforms to differentiate themselves and build stronger customer relationships [8].

Many workers face income gaps that last only a few days or weeks, yet these shortfalls can create significant financial stress. In fact, over half of Labor Economy workers reported needing access to their earnings early to cover essential expenses within the past 90 days [7]. Unfortunately, traditional disability insurance isn’t designed to address these short, recurring disruptions. Its long waiting periods and strict claim requirements make it unsuitable for such situations.

Traditional insurance products often require physical injury to trigger coverage, completely overlooking the issue of income volatility [2][4]. This leaves workers caught in a cycle of financial stress, where borrowing against future paychecks only worsens the strain on their next payday. These challenges highlight the urgent need for a more immediate, adaptable solution.

Embedded income protection fills this gap by targeting 30-, 60-, and 90-day income disruptions. These solutions integrate directly into banking and lending platforms, providing coverage precisely when workers face financial pressure. Unlike traditional insurance, embedded options eliminate the friction of complex distribution processes. Walnut’s API-driven platform makes this approach seamless, offering flexible integration, access to over 14 carriers, and full compliance across the U.S. and Canada.

Short-term income protection is not only practical but scalable. More than 50% of consumers have shown interest in such products [8]. By embedding these solutions, platforms can stand out while increasing customer loyalty and lifetime value. With monthly premiums ranging from $3 to $10 for opt-in models - or even less for fully embedded options [8] - these products deliver meaningful protection without complicating the user experience.

Walnut’s platform demonstrates how embedded solutions can tackle today’s financial challenges head-on. With its efficient, API-driven infrastructure, Walnut enables businesses to offer compliant, scalable income protection exactly where it’s needed most - bridging the gap between digital finance and the everyday financial pressures workers face.

A short-term income disruption refers to an event that interrupts income for less than 90 days. These situations are often managed with short-term disability insurance, which generally offers benefits for a period of 90 to 180 days. Common examples include a temporary job loss or taking a brief medical leave.

Disability insurance is primarily meant to provide long-term financial protection, usually kicking in after a waiting period of at least 90 days. These policies aren't designed to handle shorter interruptions in income, as their focus is on covering prolonged periods of disability rather than addressing brief, temporary setbacks.

Embedded income protection works by connecting directly to bank or loan apps through APIs. This allows users to effortlessly enroll in coverage while opening an account or applying for a loan. It becomes a seamless part of the financial experience, offering quick setup and affordable monthly premiums - typically ranging from $3 to $10. By tackling short-term income disruptions, this approach delivers both convenience and peace of mind, without the need for separate insurance applications or processes.