February 4, 2026

Embedded insurance is reshaping how people buy coverage by integrating it directly into platforms like travel apps, rental services, and loan marketplaces. Instead of seeking standalone policies, users can now access insurance options during everyday transactions - like booking a flight or signing a lease. This approach has driven rapid growth, with premiums expected to jump from $13 billion to $70 billion by 2030.

At its core, embedded insurance relies on a modular system called the insurance stack, which connects platforms to insurance providers through APIs. Key features include:

This system benefits both businesses and consumers:

Industries like lending, rentals, and travel are using the same playbook to offer insurance tailored to their user journeys. For example:

Walnut, a platform powering embedded insurance, simplifies integration by handling pricing, compliance, and claims through a single system. Businesses can deploy insurance offerings quickly with no-code tools or deep API integrations, scaling efficiently without building their own infrastructure.

Embedded insurance is becoming a key part of the customer experience, offering convenience, cost savings, and new revenue opportunities for businesses.

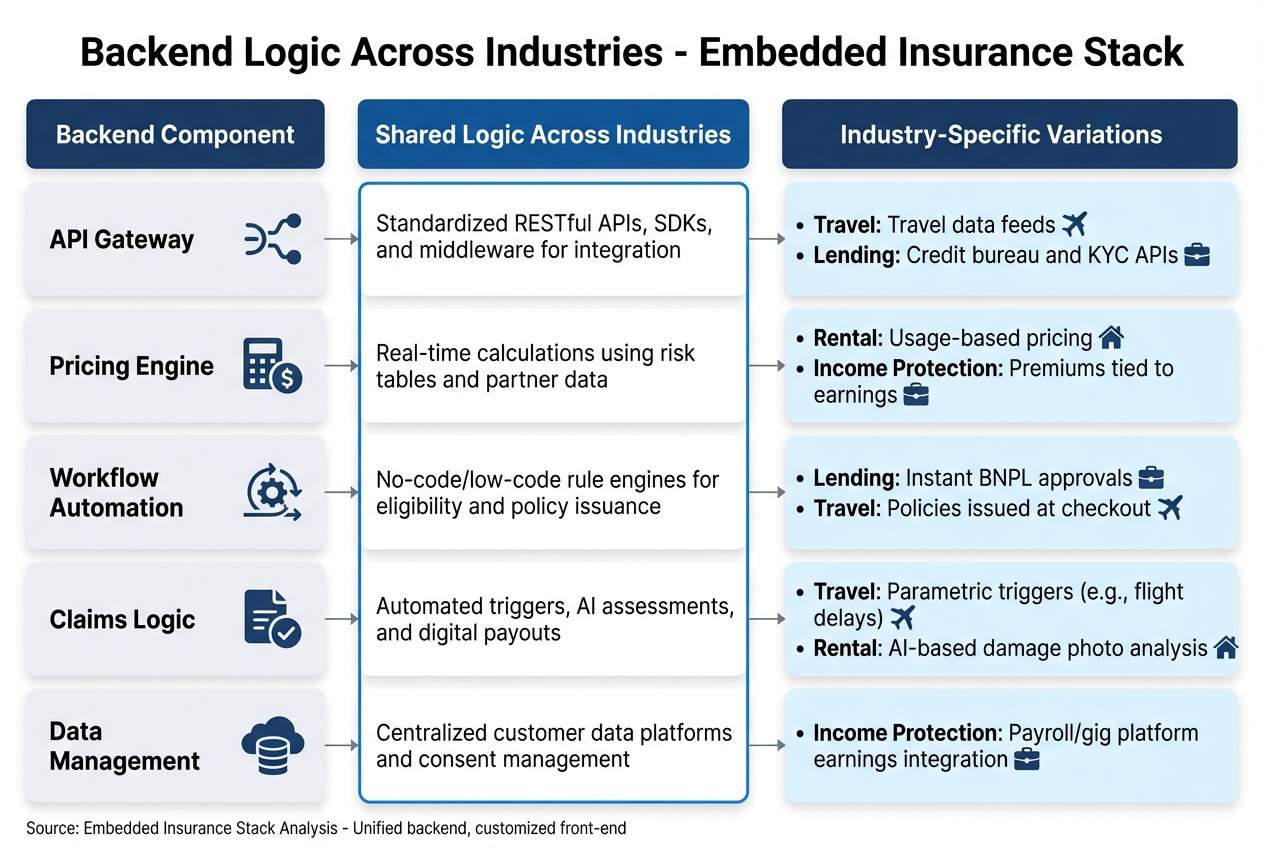

The embedded insurance stack is built on three interconnected layers: distribution APIs, pricing engines, and claims automation. These layers work independently but connect seamlessly through standardized interfaces, enabling scalable and modular integration across various industries [2][3].

"Embedded insurance is no longer just an add-on; it is becoming a native function of next-generation insurance technology platforms." - BCG

This design prioritizes configuration over coding, making it possible to adjust coverage and pricing quickly without requiring new development [2][3].

Distribution APIs act as the bridge between insurance providers and digital platforms. These plug-and-play tools allow apps for travel, lending, rentals, and more to embed insurance quotes directly into their user flows. For example, when someone books a flight or signs a lease, the API instantly fetches coverage options and pricing through standardized endpoints, ensuring real-time communication [2][3].

The technical backbone of these APIs often relies on REST-based frameworks (or similar), which handle tasks like generating quotes and binding policies. This streamlined approach simplifies integration for platforms while maintaining functionality.

Dynamic pricing engines calculate premiums on the spot, drawing from multiple data sources. These might include telematics from connected vehicles, IoT sensors in machinery, or health data from wearables. Algorithms then process this data to adjust rates in real time [2][4].

This shift from batch processing to real-time calculations ensures instant quotes and more accurate pricing. For industrial applications, where unplanned equipment downtime can cost manufacturers around $50 billion annually, embedded insurance taps into predictive maintenance data. By monitoring machinery health, insurers can offer precise pricing and even discounts for well-maintained equipment [4].

The next step in the process is automated claims processing, which ties the entire system together.

AI-powered claims automation streamlines the verification and payout process. Advanced systems use parametric models, which trigger claims based on verified events rather than manual assessments. For instance, if a flight is delayed by over three hours, the system automatically checks airline records and processes the payment - no paperwork required [2][7].

"APIs allow real-time eligibility checks, smart contracts can automate claims, and open standards enable insurers and partners to scale without reinventing integrations for every geography." - Adam Feiler, SVP of Global Sales, Air Doctor

These systems go beyond simple triggers. They automate tasks like eligibility verification, fraud detection, and payment processing with minimal human involvement. The result? Faster resolutions, lower administrative costs, and a smoother experience for users - all while improving operational efficiency for platform operators [2].

The embedded insurance stack operates on consistent backend principles across industries - distribution APIs, dynamic pricing engines, and automated claims. However, the way this framework is tailored for each sector depends on the specific user journey. This approach ensures a stable backend while allowing the front-end experience to align with the unique demands of different industries.

Lenders incorporate creditor protection directly into loan applications using real-time API connectivity. When a borrower applies for a loan, the system instantly retrieves loan details to provide a quote within seconds. The insurance policy is automatically bound during checkout, removing the need for separate applications [6].

Dynamic pricing takes this further by using real-time data to adjust premiums. For instance, equipment financing platforms can leverage telematics from vehicles or sensors on heavy machinery to monitor usage and operator behavior. This allows insurers to price coverage more precisely and even offer discounts for well-maintained assets [4][1]. Considering that industrial manufacturers face losses of up to $50 billion annually due to unplanned downtime, breakdown coverage becomes a valuable add-on for leasing platforms [4].

Rental platforms use similar modular systems to embed tenant insurance during the lease-signing process. APIs pull property details to calculate tailored premiums without requiring additional coding. Flexible product engines adjust coverage options - such as liability or contents insurance - based on user needs [2].

The workflow also integrates policy issuance, premium payments, and claims handling. Platforms can enhance personalization further by incorporating data from smart home sensors or lease histories, moving beyond generic pricing models.

Gig economy platforms embed income protection insurance by performing real-time eligibility checks and applying usage-based pricing. For example, when a driver begins a shift or accepts a ride, the system automatically activates coverage. Premiums are adjusted based on factors like miles driven, hours worked, or active status, leveraging data the platform already collects [5][8].

Hybrid workflows streamline claims processing, with minor claims handled automatically and more complex cases routed for manual review. Experts predict that by 2029, 30% of all insurance transactions will occur through embedded channels, with gig platforms and other digital-first ecosystems leading the charge [5].

Travel platforms adapt the embedded insurance model for destination-specific needs. Insurance is offered during checkout, with APIs using trip details - such as destination, duration, and traveler profile - to generate instant quotes. These systems also support multi-currency transactions, allowing users to purchase coverage in their local currency no matter where they are traveling [2][8].

Parametric claims make travel insurance especially efficient. For instance, if a flight is delayed by more than three hours, the system automatically checks airline records and processes the payout - no forms, no waiting. This is possible because the trigger (flight delay) is both objective and verifiable through external data sources [2].

This section ties together the key elements of pricing, distribution, and claims management, creating a unified approach that works across industries.

At the heart of this system is a shared embedded insurance architecture. It’s built on standardized APIs, real-time pricing capabilities, and automated claims processing. While the back-end remains consistent, the front-end is tailored to match the unique user journey of each industry.

Insurers only need to build this infrastructure once, after which it can be deployed across various sectors. Business users can quickly define policy types and adjust terms without requiring new code. For instance, a rental platform could introduce tenant insurance in just weeks rather than months, thanks to a flexible product engine that simplifies customization.

"The tech-driven nature of embedded insurance also gives insurers the ability to dynamically define, monitor, and adjust their insurance propositions using real-time data." – Félix Bejarano, Managing Director & Senior Partner, BCG

Even though the front-end integrations differ - such as travel platforms relying on flight data APIs or lending platforms integrating with credit bureaus - the orchestration layer that handles quotes, policy issuance, and claims remains uniform across industries.

Backend Component

Shared Logic Across Industries

Industry-Specific Variations

Standardized RESTful APIs, SDKs, and middleware for integration.

Credit bureau and KYC APIs.

Real-time calculations using risk tables and partner data.

Premiums tied to earnings.

No-code/low-code rule engines for eligibility and policy issuance.

Policies issued at checkout.

Automated triggers, AI assessments, and digital payouts.

AI-based damage photo analysis.

Centralized customer data platforms and consent management.

Payroll/gig platform earnings integration.

Scalability is a cornerstone of this framework. As insurers expand into micro-policies and short-term coverage, backend systems must process thousands of transactions per second. Cloud-based infrastructure ensures both horizontal and vertical scaling, maintaining performance even under heavy loads. This approach enables Walnut to deliver embedded insurance solutions that are both scalable and secure, supporting rapid growth without compromising efficiency.

Walnut simplifies embedded insurance integration by leveraging a unified framework that manages pricing, distribution, and claims logic. With this approach, the platform handles everything from instant quotes and policy issuance to compliance and claims - all through a single integration point. This system is designed to work seamlessly across industries like lending, rentals, and travel.

Walnut's API delivers quotes in under two seconds, pulling data directly from partner systems. Businesses can choose between a deep API integration for tailored experiences or a no-code solution that can be deployed in less than a day. For example, a rental platform might use Walnut's no-code dashboard to offer tenant protection insurance during lease sign-up. The system automates risk assessment and pricing based on property details, enabling quick, real-time integration for various insurance applications.

Additionally, Walnut's continuous underwriting feature updates pricing dynamically as customer data evolves. This allows lending platforms to provide creditor insurance quotes that adjust based on factors like loan amounts, terms, or borrower profiles.

Walnut's modular product engine allows businesses to tailor insurance programs to meet specific market needs. For instance, a gig economy platform could configure income protection plans with premiums tied to workers' earnings, while a travel site might design coverage based on trip costs and destinations.

The platform supports distribution across multiple channels, including web embeds, mobile SDKs, and partner portals. A notable example is Neo Financial, which in January 2025 integrated credit card insurance directly into its digital platform. CEO Andrew Chau highlighted how Walnut's infrastructure enabled product expansion [9].

Walnut ensures compliance by managing licensing and broker support while adhering to state-specific regulations. The platform automates compliance checks, enforces data privacy controls, and maintains audit trails, making it easier for businesses to navigate regulatory requirements.

Built on a cloud-native architecture, Walnut scales effortlessly to handle peak traffic - whether it's a holiday travel rush or a surge in loan applications. With a 99.99% uptime guarantee and fault-tolerant systems, the platform supports growth from hundreds to millions of policies. Automated accounting reconciliation further streamlines operations, managing revenue splits among brokers, enterprise partners, and insurers without manual intervention.

The embedded insurance stack is changing how businesses in industries like lending, rental, and travel offer coverage to their customers. With standardized APIs, automated risk engines, and adaptable product options, insurance can now be seamlessly woven into customer experiences. This approach not only simplifies compliance but also allows for real-time pricing updates based on specific transaction data, paving the way for a more advanced way to deliver insurance.

In the U.S., property and casualty embedded insurance is expected to grow to $70 billion by 2030, while the global market could reach an impressive $700 billion by the same year[1][2].

"Embedded insurance is no longer just an add-on; it is becoming a native function of next-generation insurance technology platforms." - BCG

Walnut’s platform makes it easier for businesses to integrate insurance without relying on outdated legacy systems. It offers tools like instant quote generation, automated compliance management, and scalable cloud-based architecture. These features form the backbone for embedding insurance across a variety of industries. Key components such as distribution APIs, dynamic pricing, and automated claims processing reduce the need for manual underwriting, making operations more efficient.

As digital platforms continue to advance, embedding insurance directly at the point of need is becoming a way for businesses to stand out. Companies that adopt embedded insurance today can unlock new revenue opportunities while building stronger customer relationships through added protection and peace of mind.

Embedded insurance brings clear benefits to both consumers and businesses by weaving insurance coverage directly into the purchase process. For consumers, it’s all about simplicity and convenience. By bundling insurance with products or services they’re already buying - like travel bookings, car purchases, or rental agreements - it eliminates extra steps. This integration not only saves time but often lowers costs, making coverage easier to access. It’s especially appealing to Millennials and Gen Z, who value digital-first, low-effort solutions that fit seamlessly into their lives.

For businesses, embedded insurance opens doors to new revenue streams and deeper customer connections. Including insurance as part of their offerings can boost sales, improve profit margins, and add extra value for customers. Plus, it smooths out the buying process and allows for real-time tweaks to pricing and policies, thanks to advanced tech platforms. In short, embedded insurance helps companies stay competitive while delivering the convenience and efficiency today’s consumers expect.

The embedded insurance stack operates on a flexible, modular framework designed for effortless customization and growth. It leverages real-time data processing, making it possible to deliver dynamic underwriting and tailored pricing options for customers.

Core features include APIs that integrate smoothly with existing platforms, ensuring an uninterrupted user experience, and efficient claims processes that make resolutions quicker and simpler. This setup creates a cohesive system that can be applied across industries such as lending, real estate, and travel, offering protection solutions tailored to various needs.

Businesses can easily integrate embedded insurance into their platforms using API-driven solutions or no-code tools.

With API integrations, companies can enable real-time data exchange, automate policy issuance, and streamline claims processing. This approach offers a flexible setup that can be tailored to fit the platform's user experience. Typically, implementing an API-driven solution takes about 2 to 4 weeks, ensuring both scalability and operational efficiency.

For those looking for a quicker route, no-code platforms make it possible to embed insurance in under 24 hours. These tools manage backend operations and require little to no technical expertise, allowing businesses to focus on delivering a seamless customer experience. Both methods are designed to ensure compliance, allow for customization, and integrate smoothly with existing systems, making embedded insurance adoption straightforward and effective.