February 11, 2026

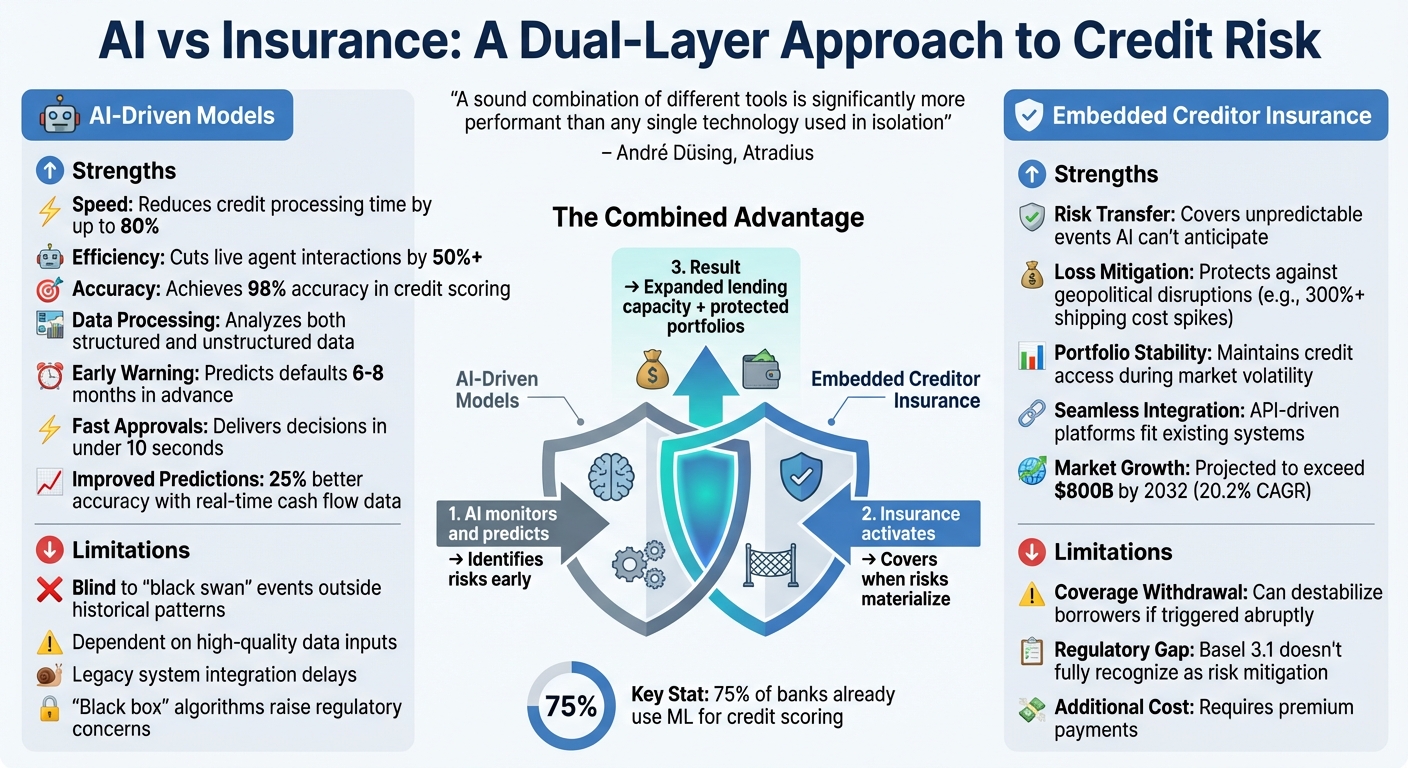

Lenders are facing a new era of credit risk management. AI-powered models now analyze real-time data to predict defaults with high accuracy, often months in advance. But these systems aren't foolproof, especially during unforeseen events like geopolitical disruptions or economic shocks. That's where embedded creditor insurance steps in, providing a financial safety net when AI predictions fall short.

This combination enables lenders to extend credit confidently while protecting their portfolios from unexpected risks. By blending predictive analytics with risk-transfer mechanisms, the lending industry is better equipped to navigate today's uncertain markets.

In the past, traditional credit models only reviewed borrower data at set intervals, often missing significant changes that occurred during the year. Dynamic AI-driven models have changed the game, offering continuous monitoring by analyzing live data streams to identify emerging risks as they happen.

The results speak for themselves. For example, in February 2025, Lender Toolkit incorporated Ocrolus's AI-powered document analysis into its "AI Underwriter" platform. This upgrade allowed mortgage lenders to automatically extract data from unstructured documents - like bank statements and pay stubs - with an impressive 99% accuracy rate. Over 300 lending institutions benefited by processing a variety of document types seamlessly within their existing loan origination systems, completely removing the need for manual reviews [6].

Another standout example is Moody's "Credit Sentiment Score" tool, which uses massive real-time data analysis to send out early risk warnings - often well before major credit shifts occur [3]. By processing data at lightning speed, these AI models not only make risk assessments faster but also allow lenders to anticipate and respond to risks far earlier than ever before.

The ability to continuously analyze data doesn't just improve risk detection - it also helps lenders stabilize their portfolios. During periods of economic uncertainty, real-time sequence models provide early predictions of defaults, giving lenders a much longer lead time compared to traditional scorecards. This advantage becomes even more critical during recessions, where macro-conditional hazard models - combining macroeconomic indicators with individual borrower behavior - outperform static approaches by a wide margin [1].

This extended warning period gives lenders the opportunity to take proactive steps, such as adjusting credit terms, increasing oversight, or implementing protective measures months before defaults occur. André Düsing, Senior Manager Corporate Strategy at Atradius, explains:

"AI models might also be sensitive to patterns and trends that might be missed by human observers, thus enhancing the precision of risk assessments"

.

These dynamic models are a key piece of a larger strategy, where tools like embedded insurance act as a safety net to protect portfolios from unexpected risks.

Today, 75% of banks already rely on machine learning for credit scoring, early risk detection, and pricing [7]. The goal isn’t to replace existing systems but to enhance them. Modern AI platforms are built with modular architectures, making it easy to integrate real-time capabilities into older infrastructures without requiring a complete system overhaul.

A great example of this is Sunrise Communications AG, a leading Swiss telecom provider. In 2024, they adopted INFORM's RiskShield, a cloud-based credit risk scoring system. This tool combined internal and external data to evaluate customer risk during onboarding. The result? Sunrise successfully balanced customer acquisition with controlled credit exposure and reduced bad debt - all while seamlessly integrating the solution into their existing systems [8].

This kind of flexible digital infrastructure not only improves immediate credit operations but also lays the groundwork for integrating embedded creditor insurance, offering another layer of protection against unpredictable risks.

Embedded creditor insurance, like Walnut Insurance, offers a practical layer of financial protection that works alongside AI's ability to identify risks. By integrating directly into lenders' systems through API-driven platforms, solutions like these analyze unstructured data sources - such as real-time news, social media sentiment, and cybersecurity metrics - to uncover patterns that might go unnoticed by human analysts. These insights allow embedded insurance to respond dynamically, activating tailored coverage as soon as risk signals emerge [4][5][3].

Embedded insurance doesn’t just detect risks; it acts on them. When AI models flag heightened risks, these solutions can kick in with protective measures automatically. For instance, in February 2024, Company Watch introduced a Scoring API and historical index on Google Analytics Hub. This tool enables lenders to integrate financial analytics - like the "H-Score®" - into their systems, offering real-time insights into risk conditions [4].

This capability is particularly valuable when dealing with unpredictable events like job losses, disabilities, or sudden business disruptions. By stepping in during these moments, embedded insurance helps mitigate the financial impact, reducing delinquencies and defaults, and strengthening lending portfolios against unexpected shocks.

In addition to real-time responses, embedded insurance plays a critical role in stabilizing credit portfolios during uncertain times. For digital lenders navigating liquidity challenges or economic volatility, these solutions offer more than just immediate coverage. By combining B2B transaction data with AI-driven financial insights, lenders can make more informed decisions about coverage. This approach ensures credit availability during market disruptions, allowing lenders to manage risk through insurance rather than restricting access to credit [3].

Walnut Insurance's platform is designed to fit seamlessly into existing systems, offering a range of integration options. From no-code solutions for quick deployment to fully headless APIs for a deeply integrated, branded experience, the platform adapts to different needs. For those seeking a middle ground, the Data-Driven Referral Link provides a faster setup while still enabling data sharing.

This flexibility means lenders can implement embedded insurance without needing to overhaul their systems. Rather than replacing AI underwriting, these solutions complement it, creating a robust risk management framework. Together, predictive analytics and embedded insurance form a partnership that protects portfolios from both predictable and unforeseen risks.

As lenders transition from static to dynamic risk management, combining AI insights with embedded creditor insurance creates a dual-layer approach to tackle both predictable risks and unexpected challenges.

AI-driven models stand out for their speed and scope. These systems can slash credit processing times by up to 80% and reduce the need for live agent interactions by more than 50% [9]. They process structured data (like credit scores) alongside unstructured data (such as social media sentiment and real-time transactions) and have achieved up to 98% accuracy in credit scoring for Buy Now, Pay Later platforms [2]. As André Düsing, Senior Manager Corporate Strategy at Atradius, explains:

"AI models might also be sensitive to patterns and trends that might be missed by human observers, thus enhancing the precision of risk assessments"

.

However, AI has its blind spots. Rare, unpredictable "black swan" events - those that fall outside historical patterns - remain a challenge [10]. These models rely heavily on high-quality data, and any inconsistency or flaws in inputs can undermine their accuracy. Legacy systems can also create delays in applying real-time insights. Additionally, the "black box" nature of many AI algorithms raises regulatory concerns, especially when lenders must justify credit decisions under frameworks like the EU AI Act [5].

To complement AI, embedded creditor insurance steps in to transfer risk and mitigate losses when unforeseen events occur. For example, when shipping costs in the Red Sea skyrocketed by over 300% due to regional attacks, insurance covered losses that predictive models couldn’t anticipate [4]. This helps stabilize portfolios during economic uncertainty, ensuring credit remains accessible even in volatile markets. However, insurance has its own challenges. Abruptly withdrawing coverage based on AI signals can destabilize borrowers, forcing suppliers to demand advance payments and restricting liquidity [3]. Furthermore, regulatory frameworks like Basel 3.1 have yet to fully recognize credit insurance as an effective risk mitigation tool, limiting its broader application for lenders [4].

The integration of AI insights with timely insurance activation creates a comprehensive risk management framework. While AI pinpoints borrowers at risk and monitors potential issues in real-time, insurance steps in to absorb losses when risks turn into reality. As Düsing warns:

"We must also be weary of the AI delusion... a sound combination of different tools is significantly more performant than any single technology used in isolation"

.

The credit landscape is evolving toward live monitoring, leaving AI-only lenders exposed to certain risks. AI-driven models excel at identifying early warning signs of credit events, often up to 6–8 months in advance [3]. They can process real-time financial and behavioral data, delivering approvals in under 10 seconds [15]. However, when unexpected disruptions like geopolitical events, market volatility, or operational failures strike, no algorithm can fully mitigate the financial fallout.

This is where embedded creditor insurance fills the gap. Insurance transfers the residual risk that predictive models can’t eliminate. By combining AI with insurance, lenders can confidently expand their "buy box" - approving borrowers who might otherwise be rejected - while safeguarding portfolio stability when risks materialize [3][11]. For example, integrating real-time cash flow data into AI models can improve predictive accuracy by up to 25% compared to traditional credit scores [16]. When paired with automated insurance activation, lenders gain both sharper precision and a safety net. This dual-layer approach supports more resilient and adaptable credit portfolios.

The strongest credit portfolios don’t rely solely on AI or insurance - they harness both. AI handles initial assessments and continuous monitoring, flagging shifts in payment behavior or cash flow as they happen [13][15]. Meanwhile, insurance steps in to cover losses when flagged risks escalate into defaults. Industry experts agree that combining multiple tools is more effective than relying on any single solution [5].

In today’s unpredictable markets, lenders should adopt a two-pronged strategy: use AI for real-time sentiment and transaction monitoring to detect high-risk borrowers early, and embed insurance at the point of sale to address risks that models might overlook [3]. Investing in API infrastructure allows lenders to seamlessly integrate underwriting and insurance processes. With the embedded insurance market projected to exceed $800 billion by 2032, growing at a 20.2% CAGR, acting now is critical [12][14]. API-enabled integration strengthens this dual-layer approach.

Lenders who combine AI’s speed with insurance’s reliability will be best equipped to succeed in an uncertain future.

AI credit models can miss certain risks, such as abrupt changes in borrower behavior, large-scale economic disruptions, or unforeseen events - issues that become especially pronounced during economic downturns. These models often face challenges in adapting to real-time changes in external conditions, which can leave blind spots in their risk evaluations.

Embedded creditor insurance steps in during unforeseen circumstances such as job loss, disability, or death. In these cases, it can temporarily suspend or even cancel loan payments. This offers a safety net, reducing financial strain for borrowers while also protecting lenders from potential losses.

Lenders use embedded creditor insurance as an extra layer of protection to reduce risk, complementing their traditional underwriting methods. This type of insurance - like payment protection or debt cancellation - kicks in during specific situations, such as unemployment or disability. Integrated through APIs and digital platforms, it operates alongside AI-powered models, allowing for real-time risk evaluation and flexible pricing. This approach helps stabilize portfolios and lower default rates, all without requiring changes to the core underwriting processes.