November 7, 2025

Embedded insurance is changing how people buy and manage coverage, making it faster and easier by integrating insurance options directly into everyday purchases. Consumers now expect insurance to be simple, personalized, and available instantly. This shift is driven by:

North America leads in this space, with the U.S. projected to generate over $70 billion in embedded insurance premiums by 2030. Key enablers include advanced digital infrastructure, APIs, AI, and cloud systems. Businesses benefit from new revenue streams, stronger customer loyalty, and actionable data insights. The future will focus on hyper-personalized coverage, IoT integration, and automated claims.

Embedded insurance is becoming a standard feature across industries, offering consumers and businesses a streamlined way to manage risk and protection.

Three key shifts in consumer behavior are fueling the rapid growth of embedded insurance across North America. These changes highlight how consumers are adapting to digital services and making choices, shedding light on why embedded insurance has become a must-have for many industries.

People now expect digital interactions to be tailored to their needs - and insurance is no exception. Consumers want coverage options that match their unique risk profiles, lifestyles, and buying habits.

Gone are the days of one-size-fits-all policies. Today, individuals expect advanced systems to analyze their data and suggest relevant coverage options automatically. For instance, a frequent business traveler might need comprehensive travel insurance, while someone purchasing electronics online may look for device protection.

Data such as age, location, purchase history, and behavior patterns enable insurers to offer personalized pricing and coverage recommendations right at checkout. On top of that, customers expect policies to be activated immediately, which has driven insurers to improve their underwriting algorithms for faster decisions. This push for personalization aligns with the broader demand for seamless and efficient insurance solutions.

Convenience is king. Consumers are increasingly drawn to insurance options that are quick and simple. Complex processes, like lengthy forms or multi-step transactions, often lead to abandoned purchases, forcing the industry to focus on minimizing friction.

Embedded insurance streamlines the experience by integrating directly into the purchase process. Similar to how digital platforms save preferences and payment details, these systems use stored customer data to recommend the right level of coverage automatically.

Mobile optimization is a critical piece of this puzzle. With many North Americans using smartphones for online shopping, insurers have developed features like one-tap activation and easy-to-navigate mobile apps for managing policies. Consumers also expect hassle-free claims filing and responsive customer service, prompting innovations in automated claims processing and digital-first support.

The COVID-19 pandemic profoundly reshaped consumer attitudes toward risk and insurance. Events once considered rare - like travel cancellations, supply chain issues, and health emergencies - became part of everyday life, increasing demand for accessible and comprehensive coverage.

"The COVID-19 pandemic of 2020 drastically changed the face of travel, putting protection at the forefront of every traveler's concerns - not only for health-related risks but also for cancellations and unexpected changes." – Openkoda [1]

"Travel insurance has evolved from an optional add-on to an essential component of travel planning. Today, it must be comprehensive, covering all types of uncertainties and potential disruptions." – Openkoda [1]

In the travel sector, insurance has shifted from being a nice-to-have to an essential part of trip planning. This heightened focus on protection has extended to other areas, including online purchases, rentals, and subscriptions.

The pandemic also sped up the adoption of contactless transactions, boosting consumer confidence in managing financial matters online. These behavioral changes have created a solid foundation for the continued expansion of embedded insurance solutions.

Technology is the backbone of embedded insurance, driving the improvements needed to meet the fast-changing expectations of today’s consumers. With digital-first insurance becoming the norm, three key advancements are helping integrate insurance seamlessly into everyday transactions while delivering the speed and personalization people now expect.

APIs (Application Programming Interfaces) are the essential connectors that make embedded insurance possible. They allow businesses to link directly with insurance providers, enabling real-time, contextual coverage offers. These digital connections ensure customer data flows smoothly between systems, triggering insurance options tailored to the individual at just the right moment.

Here’s how it works: Imagine booking a flight, buying a new smartphone, or signing up for a subscription service. APIs can instantly analyze your profile, purchase details, and risk factors to present customized insurance options - practically on the spot. This kind of instant, personalized coverage is part of what’s being called Embedded Insurance 3.0.

"A forward-thinking API strategy could help group insurers deliver personalized experiences and improve operational efficiency." - Deloitte [2]

Real-time processing ensures that quotes, underwriting, and policies are completed in seconds, aligning with the modern demand for instant results. Regulatory frameworks are also stepping up to support these advancements. For instance, Deloitte highlighted Brazil’s Open Insurance initiative as a standout example of how regulations can encourage personalized insurance offerings and open up new distribution channels [2]. Alongside APIs, technologies like cloud computing and AI are pushing these capabilities even further.

Cloud platforms have revolutionized how insurance solutions scale and perform. Unlike traditional systems that require heavy infrastructure investments, cloud-based platforms can expand or contract instantly to match demand, all while maintaining reliable performance.

AI takes things to the next level by processing massive amounts of customer data in real time. It can evaluate risk, determine the right coverage, and calculate pricing - all in milliseconds. This allows for highly personalized recommendations based on someone’s behavior, demographics, and purchase history.

No-code tools are another game-changer. They let businesses design and launch insurance solutions using simple visual interfaces and templates - no advanced coding skills required. This means companies can quickly configure branding, set coverage options, and customize the user experience without getting bogged down in technical details.

Together, cloud technology, AI, and no-code tools create a system where businesses can deploy insurance solutions that are fast, flexible, and easy to use. These advancements are also helping the industry tackle one of its biggest hurdles: outdated legacy systems.

Many traditional insurers are still stuck with old, clunky tech systems that weren’t built for the speed and flexibility demanded by embedded insurance. These legacy systems often create bottlenecks, slowing down real-time processing and making integration with modern platforms a challenge. To address this, insurers are investing in long-term cloud-based transformations. These efforts aim to modernize core systems and unify fragmented data, making it easier to deliver AI-driven personalization and improve the customer experience.

However, with increased API connectivity comes the risk of cyber vulnerabilities. That’s why modern embedded insurance platforms are prioritizing robust security measures and strict data handling practices. Strong cyber defenses and compliance frameworks are essential to protect customer information and maintain trust. Additionally, partnerships between insurers and tech providers are helping to streamline the shift from outdated systems to cutting-edge solutions, speeding up deployment while reducing the complexity of the transition.

Embedded insurance, powered by advancements in APIs and AI, has evolved to meet the needs of today’s digital-first consumers. By integrating insurance options seamlessly into purchasing experiences, these models align with modern buying habits and offer a more intuitive way to access coverage.

Point-of-Sale Coverage is the most straightforward embedded insurance model. It offers coverage right at the moment of purchase - whether it’s for electronics, travel, or other significant transactions. The insurance is directly tied to the item or service being bought, making it easy for customers to understand and opt in with just a few clicks. This approach not only simplifies the process but also boosts customer confidence in their purchase.

Usage-Based Insurance takes a more tailored approach by adjusting coverage and pricing based on real-time data. For example, auto insurance can track driving habits, or device protection can adapt to how often a smartphone is used. This model appeals to consumers who value fairness and want their premiums to reflect their actual risk levels rather than general demographic averages.

Micro-Insurance focuses on small, affordable policies designed for specific risks or short-term needs. These bite-sized plans are often used for temporary device protection, short-term travel, or event-specific coverage. Their simplicity and low cost make them particularly attractive to younger consumers and those seeking flexible, on-demand options.

Each model caters to different needs: point-of-sale coverage suits high-value purchases made in the moment, usage-based insurance resonates with those seeking personalized pricing, and micro-insurance appeals to budget-conscious buyers looking for adaptable protection.

North America offers a variety of embedded insurance applications across industries, reflecting regional consumer behaviors. In e-commerce, major retailers now integrate device protection directly into checkout flows. For instance, when purchasing a smartphone or laptop, customers can add tailored protection without leaving the retailer’s site - a convenience that has proven especially popular.

In financial technology, digital banking platforms bundle travel insurance into card transactions for trip bookings, while investment apps include account protection as part of premium service plans. These integrations enhance the overall value of financial services.

The mobility sector has also embraced embedded insurance. Ride-sharing apps provide trip-specific coverage that activates automatically, while car rental platforms offer instant insurance options during booking. Electric scooter and bike-sharing services now include liability and damage protection, addressing safety concerns while maintaining ease of use.

Digital health platforms are another growing area. Telemedicine services offer consultation insurance for follow-up care, and fitness apps provide injury coverage for users engaging in their workout programs. These applications meet the rising demand for consumer protection in digital health services.

| Model | Benefits | Limitations | Best Use Cases |

|---|---|---|---|

| Point-of-Sale | Simple, contextually relevant, high conversion rates | Limited to purchase moment, less personalization | Electronics protection, travel insurance, warranties |

| Usage-Based | Personalized pricing, fair risk assessment, ongoing engagement | Requires data sharing, complex pricing, privacy concerns | Auto insurance, device protection, health coverage |

| Micro-Insurance | Low cost, flexible, easy to understand | Limited scope, frequent repurchases, lower profit margins | Event-specific coverage, short-term needs |

The ideal model often depends on the industry and customer journey. Point-of-sale works best for retailers and service providers where purchase decisions are deliberate. Usage-based insurance thrives in sectors like automotive or health, where ongoing data collection is natural. Meanwhile, micro-insurance is perfect for customers seeking quick, flexible coverage.

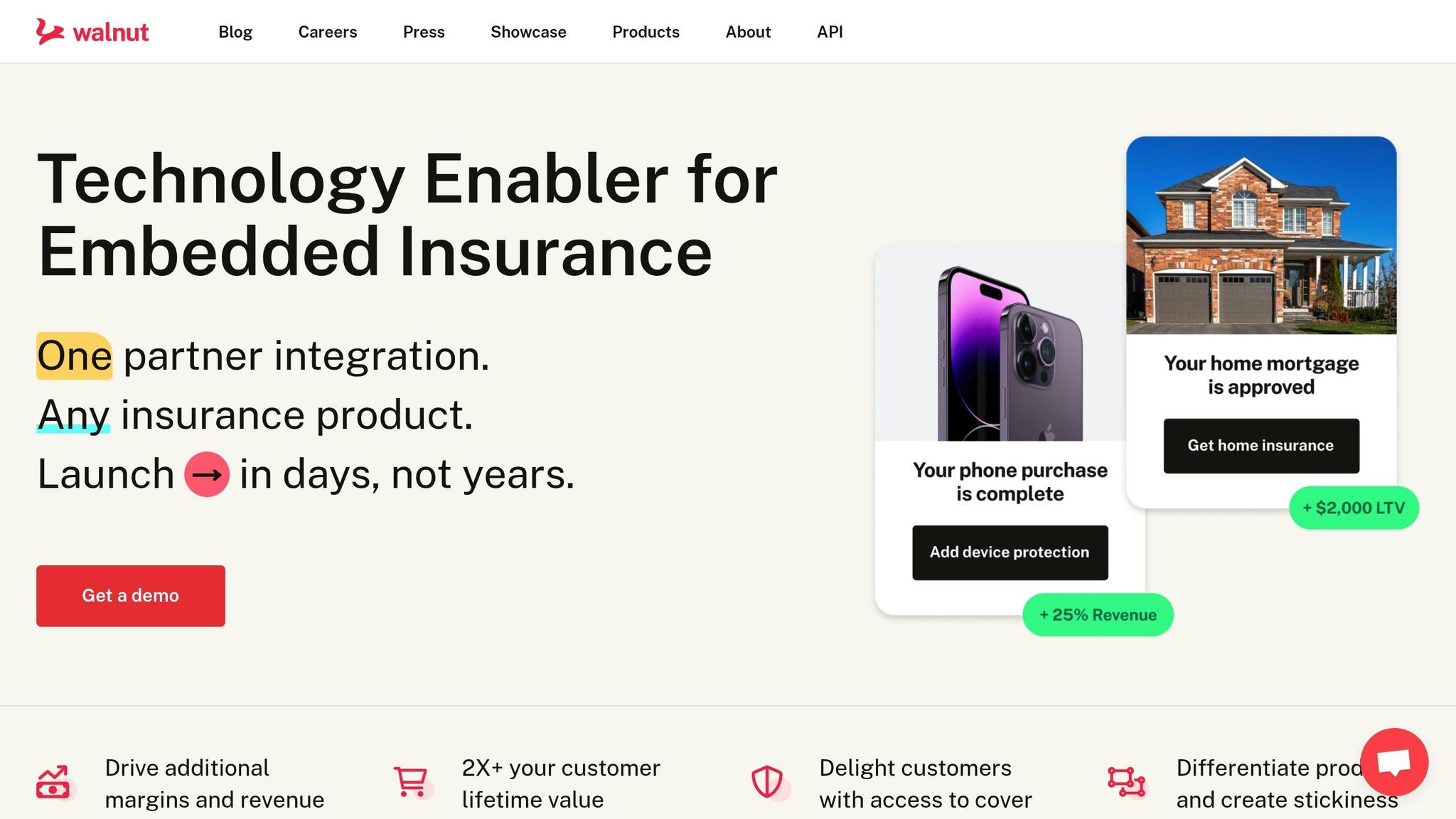

Walnut Insurance’s platform supports all three models with flexible integration options. Their Co-Branded Link Out method is ideal for businesses exploring point-of-sale insurance. The Data-Driven Referral Link suits usage-based applications, while the Headless API enables deep integration for complex micro-insurance solutions.

These models reflect shifting consumer expectations, creating opportunities for businesses to enhance their offerings while opening new revenue streams through embedded insurance. The next section will explore how these partnerships can deliver value to both consumers and businesses alike.

The rise of embedded insurance is proving to be a game-changer for both consumers and businesses. By weaving insurance options directly into the customer journey, companies are unlocking fresh revenue streams while meeting the demand for seamless, hassle-free experiences. These consumer-focused benefits naturally pave the way for business growth and strategic partnerships across industries.

Embedded insurance takes the headache out of buying coverage. Instead of juggling multiple providers, comparing policies, or navigating tedious forms, consumers can secure the protection they need at the exact moment they need it.

This approach offers personalized coverage with clear pricing and instant activation. For example, someone purchasing a $1,200 laptop can immediately add coverage tailored to that device, while a traveler booking a weekend getaway can opt for trip insurance customized to their itinerary. Because embedded insurance eliminates many traditional distribution and intermediary costs, consumers often enjoy more competitive premiums.

On top of that, managing both the purchase and insurance within a single platform creates a unified experience. There's no need to deal with separate vendors, track renewal dates, or juggle multiple customer service channels. This convenience adds to customer satisfaction and builds trust.

The advantages of embedded insurance extend well beyond the consumer. Businesses integrating insurance into their offerings stand to gain in several key ways, from boosting revenue to deepening customer loyalty.

1. New Revenue Streams

Embedded insurance allows businesses to generate recurring income through commission-based models. Companies earn a percentage of premiums for policies sold through their platforms, all while leaving the heavy lifting - like underwriting, claims, and customer service - to the insurance provider.

2. Improved Customer Retention

When insurance is part of the package, customers are more likely to stick around. Switching platforms could mean losing their insurance benefits, which creates a built-in loyalty factor. This is especially valuable in competitive markets where acquiring new customers can be costly.

3. Competitive Differentiation

Offering insurance as part of a broader solution sets businesses apart. For instance, a travel platform that includes trip protection or an electronics retailer that offers device insurance adds more value for customers. This added convenience can justify higher pricing and strengthen a company’s position in the market.

4. Actionable Data Insights

Embedded insurance programs provide valuable data about customers' preferences and risk profiles. Businesses can use this information to refine their products, target marketing efforts more effectively, and better segment their audience. These insights often go beyond the core business, offering a deeper understanding of customer behavior.

5. Building Trust

When companies provide relevant insurance options, they show a commitment to their customers' well-being. This effort to go beyond the transaction fosters trust, which can lead to increased customer lifetime value and positive word-of-mouth recommendations.

Walnut Insurance takes these opportunities a step further by offering a platform that simplifies the integration of embedded insurance while tackling technical and regulatory challenges. Their solutions are designed to be both flexible and user-friendly, making it easy for businesses to get started.

Walnut provides access to over 14 carriers and handles licensing, compliance, and carrier relationships. Depending on a partner’s needs, they offer three integration options:

This multi-carrier approach ensures that businesses aren’t tied to a single provider’s products or pricing. Partners can offer customers the best options tailored to their needs, which is especially helpful for companies new to the insurance space. Walnut also removes the complexity of navigating regulatory requirements, making the process even smoother.

Walnut’s platform includes Instant Quote and Bind Capabilities, enabling customers to get quotes, select coverage, and activate policies in real-time - all without leaving the partner’s platform. This keeps the customer journey uninterrupted while adding meaningful protection options.

To help businesses get the most out of their insurance programs, Walnut offers Revenue Optimization tools. These analytics provide insights into customer preferences, pricing strategies, and areas for improvement. Additionally, their Multi-Channel Broker Support ensures ongoing assistance with program management, customer queries, and claims, allowing businesses to deliver professional insurance services without needing in-house expertise.

Walnut’s approach goes beyond just technical solutions. By combining technology, compliance, carrier partnerships, and dedicated support, they help businesses create insurance programs that benefit both their bottom line and their customers.

The world of embedded insurance is undergoing a transformation, fueled by evolving consumer behaviors and rapid technological advancements. This shift is reshaping how businesses and individuals interact with insurance, ushering in an era of smarter, more integrated solutions.

Analysts predict steady growth for the embedded insurance market in the coming years, reflecting a major shift toward integrated insurance experiences that blend seamlessly into digital platforms. Consumers are increasingly drawn to insurance options that feel effortless and natural within their everyday interactions.

One key trend is hyper-personalization. With AI and machine learning at the forefront, insurers can now perform real-time risk assessments and offer dynamic pricing models, tailoring coverage to the unique needs of each individual.

Integration with IoT, smart homes, and connected vehicles is also becoming more common. Imagine home insurance that adjusts coverage based on data from smart security systems, or auto insurance that tweaks premiums in real time based on driving behavior captured by telematics.

Additionally, automated claims systems are cutting down on processing times, removing traditional pain points and creating smoother experiences for policyholders.

Looking forward, regulatory changes in Canada and the U.S. are expected to pave the way for even more innovative embedded insurance solutions, ensuring the industry keeps pace with technological and consumer demands.

For embedded insurance to thrive, ongoing innovation is non-negotiable. API-driven solutions must evolve to provide seamless integrations while meeting stringent security and compliance standards.

Real-time data processing is becoming a cornerstone for instant risk analysis, quote generation, and policy binding. As consumers engage with brands across various platforms - mobile apps, websites, and even physical stores - cross-platform compatibility is more critical than ever.

Transparency is another priority. Consumers need clarity on how their data is used and what their coverage entails. Thoughtfully designed user interfaces can make complex insurance details easier to understand, building trust and encouraging adoption.

Lastly, automated regulatory compliance will be essential as embedded insurance expands into multiple jurisdictions. Intelligent systems capable of adapting to different state or provincial regulations will be a game-changer for scaling operations without compromising compliance.

These shifts call for proactive strategies from industry leaders to remain competitive and capitalize on emerging opportunities.

To stay ahead in this evolving landscape, business leaders must focus on integrating embedded insurance seamlessly into the customer journey. The goal is to make insurance feel like a natural extension of the primary purchase, not an afterthought.

Choosing the right partners is critical. Look for platforms that offer strong compliance support, flexible integration options, and the ability to adapt to market changes. Pilot programs can be a great way to test customer responses and fine-tune strategies before full-scale implementation.

Investing in customer education is equally important. Clear, simple explanations of embedded insurance benefits and coverage can help build trust and drive adoption. Using data analytics to track customer behavior, conversion rates, and satisfaction levels allows businesses to continuously improve their offerings.

Finally, keeping up with regulatory changes is a must. By staying informed about market-specific regulations and collaborating with experienced partners, businesses can ensure compliance while taking advantage of the growing potential of embedded insurance.

Companies that embrace innovation and maintain a customer-first mindset will be well-positioned to succeed in this rapidly evolving industry.

Embedded insurance weaves coverage directly into the purchase of products or services, making the entire process smoother and more convenient for consumers. Unlike the traditional approach, which often involves separate steps, forms, and transactions, embedded insurance is offered right at the point of sale. This integration saves both time and hassle.

For consumers, this model comes with several benefits. It simplifies the buying process, offers personalized coverage options, and can often lower costs by cutting out unnecessary administrative expenses. Plus, it ensures that protection is available exactly when and where it's needed, aligning perfectly with a person's lifestyle or the specific purchase they’re making.

Technologies such as AI and APIs are reshaping embedded insurance by making it more tailored and user-friendly. AI allows insurers to analyze customer data in-depth, enabling them to offer coverage options that align with individual needs. Meanwhile, APIs simplify the process by integrating insurance solutions directly into platforms that customers are already familiar with, creating a smoother experience for everyone involved.

These advancements also support real-time updates, speed up claims processing, and use predictive analytics to better understand and anticipate customer needs. By tapping into these tools, insurers can provide efficient, personalized solutions that keep pace with evolving consumer expectations.

Embedded insurance integrates insurance products directly into a business's offerings, creating a streamlined and tailored experience for customers. This approach simplifies the insurance process, addressing customer needs at the perfect moment, which helps build both trust and loyalty.

With the help of data insights, businesses can customize coverage options to match individual preferences, making these services more relevant and appealing. Beyond improving the customer experience, embedded insurance also provides new revenue opportunities. Companies can profit from offering these additional services while enhancing the overall customer journey. This model works particularly well in industries like travel, retail, and financial services, where convenience and personalization are top priorities.