May 10, 2026

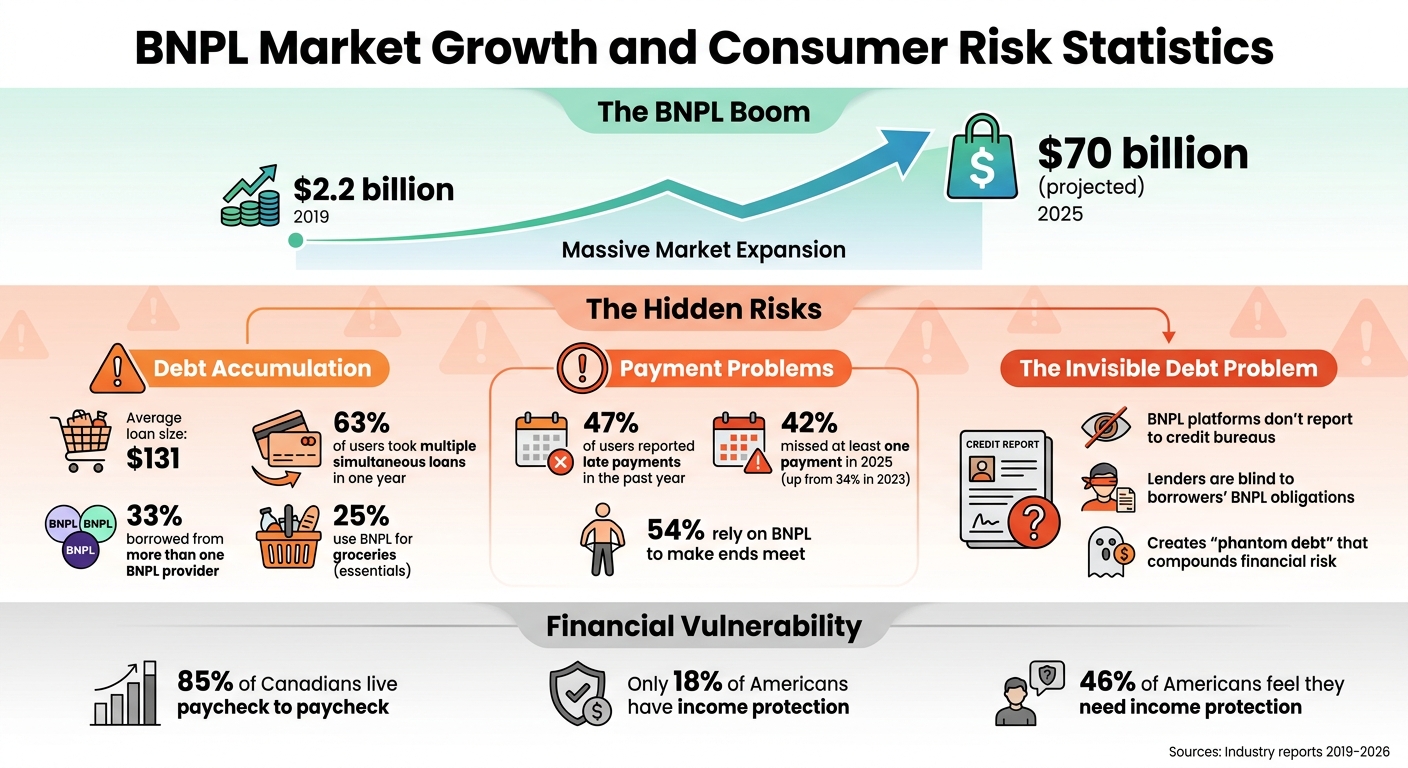

Buy Now, Pay Later (BNPL) services have grown exponentially, from $2.2 billion in 2019 to a projected $70 billion by 2025. While they offer convenience with interest-free installments, they’ve created a hidden financial risk. Here's what you need to know:

In response, solutions like embedded insurance are emerging. New tools, such as SymendPrevent, now integrate payment protection directly into BNPL systems, covering bills during financial disruptions like job loss or illness. These changes aim to address rising default rates and build consumer trust. However, without stronger federal oversight, the risks for users remain high.

One of the biggest risks with Buy Now, Pay Later (BNPL) services is how quickly small debts can pile up. For instance, borrowers often take out multiple $131 loans through BNPL platforms [1]. In fact, 63% of users took on several simultaneous loans in a single year, and 33% borrowed from more than one BNPL provider [6]. What starts as manageable payments can spiral into what experts call "debt creep", where borrowers struggle to keep up with mounting due dates.

Nigel Morris, Co-founder of Capital One, summed up the problem:

In a world where, if I'm a buy-now-pay-later provider, and I'm not checking bureau data, I'm not feeding bureau data, I'm oblivious to a consumer taking out 10 such loans in a week.

The absence of reporting by BNPL platforms means lenders often fail to see the full picture of a consumer's debt. This blind spot can lead borrowers to prioritize paying off small BNPL obligations over larger, more important bills like credit cards or car loans [6].

The issue becomes even more pressing when you consider how people are using BNPL. About 25% of users rely on BNPL to finance groceries [6]. What used to be a tool for discretionary spending is now being used for essentials. If someone’s income drops or stops, they’re left with no safety net. These overlapping debts not only stretch personal budgets thin but also make it harder to accurately track and report overall financial obligations.

The risks tied to BNPL aren't just personal - they’re systemic. Regulatory gaps in both Canada and the U.S. leave consumers vulnerable. Many BNPL products in the U.S. fall outside the scope of the Truth in Lending Act (TILA) because they don’t charge interest or fees. This lack of oversight worsened in May 2025 when the Consumer Financial Protection Bureau (CFPB) reversed an earlier rule that would have treated BNPL like credit cards. Without that rule, BNPL providers are not required to offer dispute resolutions or billing statements [4].

Connecticut Attorney General William Tong highlighted the problem:

As Trump rescinds critical protections for buy-now-pay-later consumers, it's up to states now to ensure shoppers know what they are getting into, and to ensure these companies are held accountable.

The absence of federal protections has created a patchwork of state regulations. Some states, like New York, have tightened oversight, while others, like Nevada, have relaxed their requirements [3]. But as Adam Rust, Director of Financial Services at the Consumer Federation of America, pointed out:

A state-by-state patchwork will never work as well as robust federal regulations. Is there a state that can match the CFPB? I am not sure that there is.

In Canada, the situation is similar. The Financial Consumer Agency of Canada (FCAC) hasn’t established specific rules for BNPL, choosing instead to monitor the situation and coordinate with provincial authorities [5]. This lack of regulation means Canadian BNPL providers don’t face the same disclosure and dispute-resolution standards as traditional credit products. The result? 15% of users report making tough financial choices, such as delaying other bill payments, just to meet their BNPL commitments [5]. Without clear, standardized protections, consumers in both countries are left exposed to financial strain when their income is disrupted.

Between 2024 and 2025, the regulatory environment for Buy Now, Pay Later (BNPL) services underwent dramatic changes. In May 2024, the Consumer Financial Protection Bureau (CFPB) introduced an interpretive rule that categorized BNPL services as credit cards under the Truth in Lending Act. However, this rule was rescinded just a year later, leaving a regulatory gap [4][6][7][8].

This federal rollback prompted states to step in. For instance, New York introduced licensing requirements for BNPL providers in May 2025. Additionally, seven state attorneys general sent inquiries to major BNPL companies, demanding increased transparency [2][6]. As Connecticut Attorney General William Tong emphasized, the responsibility for consumer protections and platform accountability now largely rests with state governments.

These varied state-level regulations are pushing BNPL platforms to reevaluate their strategies. The numbers paint a clear picture: 42% of BNPL users missed at least one payment in 2025, compared to 34% in 2023, and 85% of Canadians reported living paycheck to paycheck [6][9]. With both regulatory and market pressures mounting, BNPL providers are actively seeking ways to address consumer vulnerabilities while maintaining compliance.

To bridge this gap, embedded insurance solutions are emerging as a practical answer. These solutions aim to address weaknesses in traditional credit safeguards by offering direct protection against fragmented BNPL debt.

Embedded insurance works by integrating bill protection into BNPL payment systems through API connections. A notable example is the launch of SymendPrevent in April 2026, a collaboration between Symend and Walnut Insurance. This platform uses behavioral science to offer bill payment protection at critical moments. Walnut’s API-driven infrastructure allows BNPL platforms and essential service providers to add this protection seamlessly, without overhauling their existing technology [9].

The results from early implementations are promising: over 50% of users opened notifications, and churn rates dropped by 60%, as the system automatically covered bills during key life events [9]. Adrien Niblock, Co-Founder of Walnut Insurance, highlighted the achievement:

Embedded insurance has been promised for years. SymendPrevent is what it looks like when it actually works at scale.

These solutions address specific disruptions such as job loss, critical illness, hospitalization, or even death. When such events occur, the embedded insurance covers the BNPL installment or utility bill directly [9]. By integrating with major payment processors, the process becomes as smooth as a standard checkout experience [6]. For BNPL providers grappling with inconsistent federal oversight and rising default rates, embedded insurance offers a way to safeguard both consumers and their financial stability.

As regulatory changes and tech advancements reshape the financial landscape, embedded bill protection is becoming a game-changer for consumer trust. For Buy Now, Pay Later (BNPL) platforms, this feature is transforming how consumers handle financial risks.

Take the April 2026 launch of SymendPrevent as an example. This platform stepped in to assist customers during financial hardships, achieving over 50% adoption and slashing churn rates by more than 60% in a short time frame [9][10]. It specifically addresses the challenges of fragmented micro-debt across multiple platforms, offering relief when consumers face financial strain.

Here’s how it works: if a covered event like job loss, hospitalization, or a severe illness occurs, the system directly pays the BNPL provider’s bill. This ensures uninterrupted services for the consumer while safeguarding the provider’s revenue stream. Hanif Joshaghani, CEO of Symend, put it plainly:

SymendPrevent is the fix - the first solution that simultaneously protects existing revenue and generates new revenue from the same customer moment. In this economic climate, bill payment protection shouldn't be a competitive differentiator - it should be the standard.

The growing success of consumer protection tools like this is also opening doors for new revenue streams in the BNPL space.

BNPL platforms are no longer just payment processors - they’re evolving into businesses with dual revenue streams, combining transaction fees with insurance premiums. This shift is particularly timely, as credit card charge-off rates hit their highest levels in over a decade [9]. Embedded protection offers a way to turn potential losses into opportunities for customer retention.

Here’s the reality: only 18% of Americans currently have income protection, even though nearly half (46%) feel they need it [9]. With their strong customer relationships, advanced behavioral data, and established payment systems, BNPL providers are well-positioned to integrate insurance solutions. By leveraging APIs - such as those offered by Walnut - they can seamlessly add these features without major tech overhauls.

The benefits go beyond just reducing defaults. Embedded protection increases customer lifetime value and aligns with emerging regulatory requirements, as states push for safeguards similar to those mandated for credit cards. With 85% of Canadians living paycheck to paycheck and nearly 80% of UK workers worried about job security, offering a financial safety net is quickly becoming a must-have [9][10].

Buy Now, Pay Later (BNPL) services are at a critical juncture. With transaction volumes soaring and nearly half of users missing payments, the financial risks are becoming harder to ignore. What's more concerning is the shift in how BNPL is being used - spending on essentials like groceries has almost doubled[2]. This trend leaves consumers especially vulnerable, as disruptions to income can quickly spiral into financial strain, and traditional credit protections don’t cover these transactions.

Recent regulatory rollbacks have only widened this gap. The inconsistent patchwork of state-level oversight has left millions of Americans without adequate protection. This fragmented approach highlights the need for a more unified and effective solution to safeguard BNPL users.

The answer lies not just in meeting regulatory requirements but in integrating consumer protections directly into BNPL systems. For example, platforms using embedded bill protection tools, like Walnut's API solutions, can address both compliance and consumer needs. The push to report BNPL data to credit bureaus by 2025 is a step in the right direction, fostering transparency and helping responsible users build their credit history[1]. By embedding solutions like these, BNPL providers can bridge the protection gap while earning consumer trust.

BNPL purchases don't come with the same protections as credit cards because they fall outside the usual credit systems. While regulators are starting to adjust rules to offer safeguards like dispute resolution and refunds, these protections aren't fully in place yet. This leaves BNPL users without the safety measures credit card holders have relied on for years.

Keeping tabs on your total debt and the number of active Buy Now, Pay Later (BNPL) loans is a good way to determine if you're overextending yourself. If you're juggling several loans at the same time, it might be a red flag. Studies show that many BNPL users handle multiple loans at once, with the average borrower taking on nearly 10 loans in a single year. It's also important to avoid letting debts accumulate without a solid plan for repayment.

Embedded bill protection steps in to cover your bills if you lose income due to circumstances like job loss, hospitalization, serious illness, or even death. This service ensures that your bills are paid directly, helping you stay on top of your payments and avoid falling behind.