April 13, 2026

Bill protection and debt relief are not the same. While debt relief reduces or eliminates what you owe, bill protection provides temporary help to cover essential bills - like rent, utilities, or mortgage payments - when your income is disrupted due to events like job loss or illness. It’s not about erasing debts but ensuring financial stability during short-term setbacks.

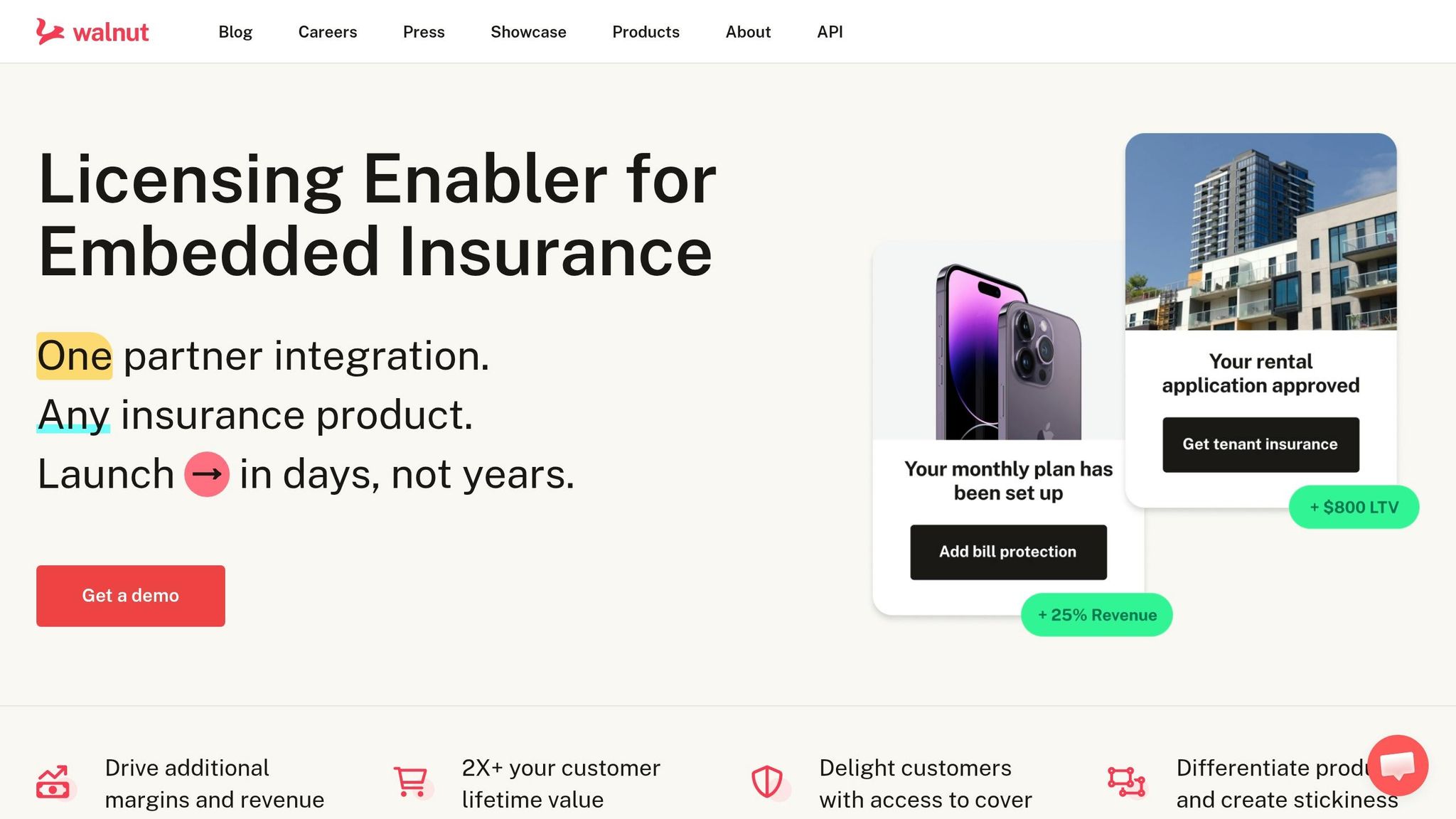

Walnut simplifies access to bill protection through easy digital integration, offering clear terms and affordable options. This transparency helps users feel secure while navigating unexpected challenges.

Bill protection serves as a short-term safety net, helping cover essential monthly expenses when your income is unexpectedly interrupted. It’s not a tool for eliminating debt but a way to manage critical bills during events like job loss or medical emergencies until your income is restored.

This coverage kicks in when specific events disrupt your income. The most common trigger is involuntary unemployment, such as layoffs, downsizing, restructuring, or business closures. However, if you lose your job due to performance issues or misconduct, you won’t qualify.

Health issues are another trigger. Coverage applies to situations where you can’t work due to chronic illness or injury. For example, disability benefits may cover conditions like cancer, post-surgical recovery, or severe mental health challenges such as depression or anxiety. Critical illness coverage is more specific, addressing diagnoses like heart attacks, strokes, organ failure, or permanent paralysis.

To activate your plan, you’ll need proof. For job loss, this means showing that your termination was unrelated to performance or behavior. For health-related claims, a formal diagnosis or documentation from a healthcare provider is required.

Most plans cover expenses for 3 to 6 months and charge monthly premiums ranging from $3 to $10 [3]. These plans are designed to focus on essential, fixed costs, ensuring you can maintain stability during a temporary setback.

Once you qualify, the plan zeroes in on non-discretionary expenses - those bills you can’t afford to skip without serious consequences. The goal is to keep your household running smoothly by covering critical costs like:

However, coverage doesn’t extend to things like credit card debt, personal loans, or optional spending. The purpose is to protect your essential services and housing during a short-term income disruption, safeguarding your financial stability and credit health.

Walnut takes the concept of bill protection - offering a safety net during income disruptions - and makes it more accessible by embedding coverage options directly into digital platforms. This approach eliminates unnecessary hurdles and ensures users remain engaged throughout the process. Here's a closer look at how Walnut's dual integration options make this possible.

Walnut offers two paths for integration, catering to both tech-savvy teams and those with limited coding resources:

Walnut’s AI-powered underwriting engine simplifies the process of offering tailored coverage. By analyzing essential user data - such as an annual income of $50,000+ and monthly expenses up to $1,000 - it delivers instant quotes. Users can then bind their coverage using compliant e-signatures, without the need for manual review. A real-world example? A US-based lending platform processed 10,000 binds per month, with 25% of users opting for $500/month utility coverage [4][6][8][9].

Compliance and clarity are at the core of Walnut’s approach. It adheres to NAIC models, state-specific regulations, and SOC 2 Type II standards. Policies are written in plain language, avoiding confusing jargon. For example, a policy might clearly state: “Covers $300 electric bills for 90 days post-job loss, not past debt.” This transparency has reduced disputes by 60%, boosted trust scores to 92%, and improved retention by 35%. Notably, 88% of US users appreciate having clear terms [4][5][6][7][8][9].

There’s often confusion about what bill protection truly offers. Many people assume it’s a debt relief program that wipes out existing balances or takes care of every financial burden. In reality, bill protection is designed as a temporary safety net, covering specific fixed expenses during short-term income disruptions. Its purpose is to help maintain financial stability while navigating unexpected challenges.

For example, bill protection might step in to cover your rent for a limited time after an involuntary layoff. However, it won’t pay off your credit card debt or settle outstanding medical bills. Understanding this distinction upfront helps set realistic expectations and highlights how transparency in design builds trust.

Covers all debts and financial losses

Covers only specific fixed expenses like rent, utilities, or mortgage payments

Functions as debt forgiveness or relief

Provides temporary payment assistance with no debt erasure

Anyone experiencing financial hardship qualifies

Requires specific triggers such as involuntary job loss, disability, or critical illness

Is a loan that must be repaid

Is an insurance benefit with no repayment requirement

Using clear, straightforward terms is far more effective than relying on flashy marketing phrases like "complete protection" or "total coverage." While those phrases might sound comforting, they can lead to disappointment when the actual terms fall short of those promises. Instead, transparency ensures that consumers know exactly what to expect. For instance, a policy might clearly outline that it covers essential bills but doesn’t eliminate prior debts.

The idea of a "bridge" offers a helpful analogy. As Eric Beining, Director at EisnerAmper, explains:

"The term 'bridge' refers to the program's purpose: to bridge the gap between current economic challenges and the implementation of permanent farm bill improvements... It is a temporary benefit, not a loan, even though the term 'bridge' might sound similar to 'bridge loan.'"

Transparent policies go a step further by clearly listing qualifying events - like layoffs, downsizing, or company restructuring - while also specifying exclusions, such as terminations due to performance issues [3]. By outlining these details, bill protection programs can foster trust when people need it most.

Bill protection helps cover essential expenses during short-term disruptions caused by events like layoffs, disabilities, or serious illnesses. Rather than erasing debts, it acts as a temporary income safety net, helping individuals maintain financial stability while they recover.

By clearly defining what expenses are covered, the events that trigger benefits, and the duration of assistance, bill protection fosters trust. Consumers can feel confident knowing it provides support for fixed costs like rent, utilities, or mortgage payments during income loss. This clarity reflects Walnut's dedication to offering straightforward, consumer-focused solutions.

Walnut simplifies the delivery of bill protection through flexible integration options, including no-code and co-branded flows for quick implementation. With opt-in premiums ranging from $3 to $10 per month, these protections are designed to be affordable without adding a heavy financial burden [3].

Data reveals that over 50% of consumers are interested in protection products [3]. By embedding bill protection into existing service plans, businesses can stand out, enhance customer loyalty, and deliver real financial security during uncertain times.

When consumers have a clear understanding of what bill protection offers - and its limitations - they can make confident, informed choices that align with their needs. Transparent design is key to building lasting trust.

Bill protection acts as a short-term safety net, helping you manage essential payments - like utility bills or rent - during a temporary financial setback. It’s designed to ensure you can keep up with fixed expenses while you work on getting back on your feet.

Debt relief, however, takes a different approach. It aims to address the root of financial struggles by reducing, restructuring, or even eliminating debt through methods like settlement agreements or bankruptcy. Unlike debt relief, bill protection doesn’t reduce or erase the debt you owe; it simply helps you stay afloat during a challenging period.

To qualify for assistance after a job loss or illness, you’ll usually need to submit documentation like proof of income, employment status, or medical records. The exact requirements can differ based on the benefit program you’re applying for. Ensure your paperwork clearly shows why you meet the program’s eligibility criteria.

The amount of coverage you need hinges on your financial situation and the fixed expenses you’re responsible for. Bill protection acts as a temporary safety net, helping you manage essential costs like rent, utilities, or loan payments during unexpected income disruptions. However, it’s not designed for paying off debt or offering long-term financial assistance.

To figure out the right coverage amount, start by calculating your fixed monthly expenses. For example, if your monthly costs total $2,000, aim for a plan that meets or slightly exceeds this amount. Make sure to carefully review the plan’s benefit triggers, coverage duration, and qualifying events to ensure it aligns with your specific needs.