December 31, 2025

Auto insurance isn’t dead, but it’s changing fast. EV subscription services now bundle insurance, maintenance, and roadside assistance into a single monthly fee, eliminating the need for separate policies. This all-in-one model, called Vehicle-as-a-Service (VaaS), simplifies costs and offers flexibility, with month-to-month terms and no long-term commitments. By 2030, embedded insurance could shift $50 billion in premiums from traditional insurers to these models.

Key points:

Both models will coexist, catering to different needs. EV subscriptions prioritize convenience, while traditional insurance offers more control and repair choices.

Traditional auto insurance relies on static demographic data - like age, gender, marital status, and driving history - when determining premiums, without factoring in real-time driving behaviors [6].

This model comes with hefty overhead costs. In 2020, the top three U.S. property and casualty insurers spent over $5 billion on advertising alone [6]. These expenses inevitably trickle down to consumers, contributing to higher premiums. Additionally, modern vehicles bring higher repair costs. For instance, replacing a windshield can now cost over $1,000 due to the need for sensor recalibration [3]. Between 2023 and 2024, full-coverage auto insurance premiums surged by 26% [10], partly because tech-heavy vehicles demand 25% to 35% longer repair times [3].

Traditional policies are designed with driver liability in mind, primarily for vehicles where humans maintain control (automation Levels 0–2) [6]. These policies typically bundle liability, collision, and comprehensive coverage into a single household plan. However, this framework struggles to keep up with the shift toward autonomous features and software-driven vehicles.

As advanced driver-assistance systems (ADAS) become more common, the boundary between driver responsibility and manufacturer liability grows increasingly unclear - a challenge that traditional policies aren't equipped to handle. Additionally, repair practices are causing friction. Manufacturers often require OEM-certified mechanics to preserve warranties, while insurers tend to favor cheaper aftermarket parts [6][3].

The traditional insurance process is often clunky and time-intensive. Buying coverage at a dealership, for example, can take hours [10]. Claims processing is another pain point, as it usually involves multiple parties - customers, insurers, repair shops, and rental providers - working with incomplete accident data [6].

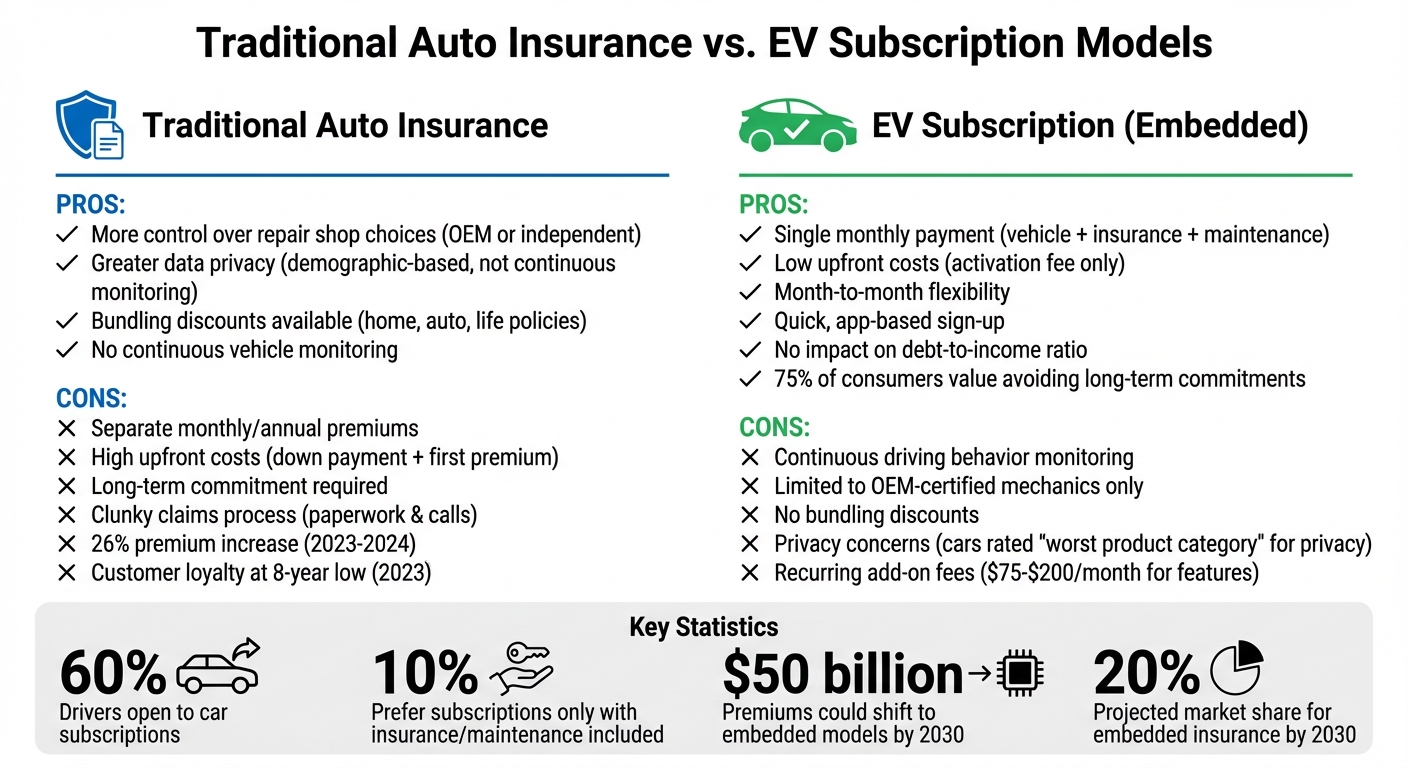

Customer loyalty in the auto insurance sector hit an eight-year low in 2023 [10]. Around one-third of U.S. consumers showed interest in embedded insurance directly from manufacturers, seeking to avoid the hassle of shopping through third-party providers. Traditional policies also lack adaptability, leaving many drivers stuck paying for coverage that doesn’t align with their actual driving habits or needs. These shortcomings highlight why more flexible and integrated insurance models are gaining traction, especially with the rise of EV subscriptions.

EV subscriptions are reshaping vehicle ownership by bundling multiple expenses into one straightforward monthly payment. This single fee typically covers vehicle access, insurance, registration, and routine maintenance, making costs more predictable for subscribers [11][4].

The financial breakdown is worth noting. For example, insuring a gas-powered Honda CR-V costs about $1,540 annually, while a Tesla Model Y averages $2,100 - roughly a 36% increase [7]. EV subscription plans absorb these higher insurance costs into a flat monthly rate. Take Autonomy’s Tesla Model 3 subscription as an example: in late 2022, it was priced at $490 per month with a $5,900 start fee. This worked out to $1.80 per mile of electric range, which was less than the $1.98 per mile cost of financing a Hyundai Kona Electric [11].

Another advantage? Subscription payments don’t count as debt, meaning they won’t impact your debt-to-income ratio - a key consideration for anyone applying for major loans. Additionally, embedded insurance removes the hassle of lengthy applications and waiting for quotes based on personal demographics [6]. Beyond simplifying costs, these plans also offer an expanded range of benefits that redefine how vehicle protection works.

EV subscription packages do more than simplify pricing - they also offer a host of benefits under one roof. Comprehensive coverage, 24/7 roadside assistance, tire replacement for wear and tear, and specialized EV maintenance are typically included, all managed by a single provider [13][4]. This streamlined approach tackles a big issue: traditional EV insurance costs, which average around $4,058 annually - approximately 49% higher than insurance for gas-powered vehicles. Much of this cost is due to insurers struggling with claims involving battery damage [12][15].

Battery packs are a significant factor, often accounting for up to 50% of an EV’s initial cost. For instance, replacing a Tesla battery can cost anywhere from $5,999 to $15,500 [14][15]. Insurers frequently total EVs after minor accidents because verifying battery safety is expensive, even though nearly 95% of salvaged batteries remain undamaged. Subscription services take on this risk directly, eliminating situations where minor damage results in a total loss.

In February 2025, Origin Energy introduced the "Origin 360 EV" in Australia, a subscription plan that bundled insurance, registration, maintenance, roadside assistance, and tire replacement. Subscribers could switch or return vehicles with just 30 days’ notice. Through salary packaging, a BYD Seal was available for $217 per week - a fraction of its $49,888 sticker price [13]. This flexible, try-before-you-buy model allows hesitant consumers to experience EV technology without committing to a long-term loan on a depreciating asset.

Beyond cost savings and comprehensive coverage, EV subscription models are elevating the customer experience. Everything is managed through an app, allowing users to select vehicles, make payments, and schedule services - all without visiting a dealership or contacting an insurance agent [4][8].

Flexibility is a key draw. Unlike traditional leases, which often require a 36-month commitment, subscriptions like Autonomy offer more freedom. For example, Autonomy requires only a three-month initial term, followed by a 28-day cancellation notice [11]. This appeals to modern consumers, with over 50% of U.S. drivers under 55 preferring a single monthly payment that covers all vehicle-related expenses [4]. Some services even incorporate telematics to offer "pay-how-you-drive" pricing based on real-time driving behavior [6]. If just 20% of the U.S. personal auto market adopts embedded models by 2030, traditional insurers could see at least $50 billion in premiums shift to these subscription-based alternatives [2].

Traditional Auto Insurance vs EV Subscription Models Comparison

As car ownership evolves, traditional and embedded insurance models each come with their own set of advantages and challenges. Traditional auto insurance gives you more control over your choices. For instance, it allows you to pick your repair shop and keeps your personal data more private. Unlike embedded insurance, which often relies on telematics to track driving behavior, traditional insurers base their rates on broader demographic data. This means less continuous monitoring of your driving habits.

On the other hand, EV subscriptions simplify things by bundling everything - your car, insurance, maintenance, and roadside assistance - into a single monthly payment. This setup eliminates surprise costs, like an unexpected tire replacement or battery diagnostics, making budgeting easier[4]. Plus, the sign-up process is quick and hassle-free, often requiring just a few clicks instead of the lengthy comparisons typical with traditional insurance[2]. Another big draw? About 75% of consumers appreciate the flexibility of avoiding long-term financial commitments[1].

But subscription models aren’t without their downsides. For one, you might miss out on bundling discounts that traditional insurance offers, such as combining auto, home, or life policies. Repairs under subscription plans are often limited to OEM-certified mechanics, which can reduce your options and lead to longer wait times for fixes[2][3]. Privacy is another concern - these models involve continuous vehicle monitoring, and a Mozilla Foundation report even called cars the "worst product category" for privacy issues[9]. Finally, recurring add-on fees, like $75 per month for Ford BlueCruise or $200 per month for Tesla Full Self-Driving, can add up over time and eat into the overall value[9].

| Feature | Traditional Auto Insurance | EV Subscription (Embedded) |

|---|---|---|

| Payment Structure | Separate monthly/annual premium | Combined in one monthly vehicle fee |

| Upfront Cost | High (down payment + first premium) | Low (activation fee or first month) |

| Repair Choice | Consumer-selected shops | Limited to OEM-certified mechanics |

| Bundling Discounts | Available (home, auto, life)[2] | Typically unavailable[2] |

| Data Privacy | Limited to claims history | Continuous driving behavior monitoring[9] |

| Flexibility | Long-term commitment | Month-to-month or short-term options |

If you own your car outright, value having choices for repairs, and enjoy multi-policy discounts, traditional insurance is likely the better fit. But if you’re drawn to convenience, lower upfront costs, and an all-in-one approach, EV subscription services might make more sense - though you’ll need to weigh the trade-offs in privacy and long-term expenses.

The discussion above highlights the contrasting advantages of traditional and embedded insurance models, showing that auto insurance isn’t vanishing - it’s transforming. By 2030, embedded insurance is expected to snag about 20% of the U.S. personal auto market, redirecting over $50 billion in premiums away from traditional providers [2]. Even so, conventional policies will still dominate, covering the majority of drivers.

Traditional insurance remains a strong option for those who value bundling discounts and the freedom to choose repair shops. On the other hand, subscription-based models appeal to budget-conscious individuals or cautious adopters of electric vehicles (EVs). Interestingly, nearly half of Americans are open to car subscription services instead of purchasing or leasing, with 10% showing interest only if insurance and maintenance are included [1].

Automakers are clearly banking on this shift. By 2030, subscription services - including bundled insurance and software features - are projected to generate $20 billion to $25 billion annually [5]. This ties back to earlier discussions about cost and coverage, where bundled services proved to simplify pricing while offering broad protection. Automakers are increasingly treating vehicles like platforms - similar to how smartphones charge monthly for apps and services. Whether consumers embrace this "Vehicle-as-a-Service" concept or push back against subscription fatigue will play a key role in shaping the pace of this transformation.

While embedded insurance models are reshaping car ownership, traditional insurance continues to serve a critical role. Both models are likely to coexist, catering to different consumer preferences and driving the evolution of the market.

EV subscription insurance rolls everything into one neat monthly payment. This package typically includes insurance coverage, maintenance, repairs, and roadside assistance - a stark contrast to traditional auto insurance, which you have to purchase separately.

One major difference lies in the cost. On average, insurance premiums for electric vehicles (EVs) are about 49% higher than those for gas-powered cars. Why? EVs tend to have a higher market value, and their repairs often require specialized expertise. With subscription models, though, these higher insurance costs are bundled into a single fee, making car ownership more straightforward and convenient.

EV subscription services depend heavily on constant connectivity to deliver bundled perks like insurance, maintenance, and roadside assistance. This connectivity allows vehicles to gather and share a significant amount of data, including location information, driving habits, and even in-car video footage. All this data is stored in the cloud, making it accessible not only to the subscription provider but sometimes to third parties, such as law enforcement. If subpoenaed, this data could disclose sensitive details about your whereabouts and behavior.

Another pressing issue is cybersecurity risks. The sheer volume of data collected by modern vehicles makes them attractive targets for hackers. A breach could expose personal details like travel history or video recordings, potentially leading to serious consequences such as identity theft or profiling. Alarmingly, many drivers remain unaware of the extent of this data collection or how to manage it.

Before signing up for an EV subscription, it’s crucial to know exactly what data is being collected, how it will be used, and how long it will be stored. Providers need to be transparent so consumers can weigh their options and make choices that prioritize their privacy and security.

Some drivers might lean toward traditional auto insurance instead of opting for an EV subscription with bundled coverage, and there are a few reasons why. One major factor is customization and flexibility. Traditional insurance lets drivers shop around, compare rates, and even bundle their auto policy with home or renters insurance to snag discounts. This approach can make it easier to manage and predict costs.

Another reason is the growing sense of subscription fatigue. With so many monthly fees piling up - from streaming services to meal deliveries - adding an EV subscription that combines insurance with other costs might feel like just one more burden on the budget.

Lastly, traditional insurers come with well-established claims processes and customer service teams that many drivers already know and trust. On the other hand, subscription-based insurance models are still finding their footing, which may leave some consumers hesitant to make the switch.