February 23, 2026

AI and insurance are transforming credit risk management. Here's how:

This combination is reshaping finance, making credit risk management faster, safer, and more efficient. Early adopters are already seeing significant savings and increased shareholder returns.

AI has transformed how lenders assess risk by analyzing a wide array of data, from traditional metrics like payment histories and debt levels to real-time account activity and even qualitative insights from loan officers. This approach helps identify borrowers who may be at risk of defaulting before issues arise.

Modern AI models combine structured data, such as credit scores, payment histories, income stability, and debt-to-income ratios, with unstructured sources like text-based loan officer evaluations, account activity trends, and broader market signals. This mix of data helps create more accurate risk predictions [6][7].

For borrowers with limited or no credit history - commonly called "thin-file" borrowers - AI turns to alternative data sources to provide a more inclusive picture of creditworthiness [6]. Dr. Carlijn Van Nieuwenhuizen from Delft University of Technology highlights the importance of this approach:

"The addition of borrower account activity to improve the discriminatory ability of blended credit score logistic models would be invaluable."

By using these diverse inputs, AI systems can build sophisticated models that go beyond traditional credit scoring methods.

AI employs advanced modeling techniques like ensemble methods (e.g., random forests, gradient boosting) and deep learning architectures (e.g., CNNs, RNNs). These tools can identify complex, non-linear patterns and process alternative data, making them particularly useful for borrowers without conventional credit histories [6].

Hybrid models are also gaining traction. For example, combining logistic regression with LSTM (a type of recurrent neural network) has been shown to deliver high predictive accuracy while maintaining the level of interpretability required by regulators [6][9].

Another exciting development is the use of Large Language Models (LLMs), such as ChatGPT. These models refine qualitative data from loan officer assessments, uncovering delinquency factors that might otherwise be missed. A study published in the European Journal of Operational Research found that incorporating ChatGPT-refined assessments into lending models can improve profitability compared to relying on human-written evaluations alone [7][10].

AI-based credit scoring has proven to be highly effective. A review of 70 studies found that ensemble models consistently outperform traditional methods in assessing risk across different demographic groups [6]. However, challenges like model drift - where performance declines over time - must be addressed [2].

MD Hasanujamman Bari from Lamar University shares a hopeful perspective:

"AI has the potential to create a more inclusive and resilient credit scoring landscape, accommodating the needs of an increasingly diverse global population."

To maintain accuracy, lenders need to regularly monitor and update their AI models. Human oversight is also essential, with human-in-the-loop systems helping to verify AI insights and counteract potential biases. This ensures that AI remains a tool requiring continuous improvement rather than a static solution [2]. By blending predictive analytics with ongoing refinements, lenders can enhance both risk assessment and borrower inclusivity.

AI identifies default risks; embedded insurance steps in to cover the financial gaps. While predictive analytics offers precision in identifying potential losses, insurance provides the safety net. Together, this combination equips lenders to handle risks with greater ease.

Embedded insurance is integrated directly into the lending process, eliminating the need for borrowers to complete separate applications. Unlike traditional credit insurance, which requires additional steps, embedded insurance is seamlessly included at the loan checkout stage.

For example, in July 2022, Root Insurance teamed up with Carvana to embed auto insurance into the car-buying experience. With just three clicks, buyers could receive a quote and adjust their coverage preferences [15].

This approach simplifies the process, offering borrowers peace of mind without adding extra hurdles.

While AI forecasts potential defaults, tailored insurance products now work hand-in-hand with these predictions to protect lenders from losses. For instance:

AI-powered models are particularly effective in underwriting specific loan types, such as auto loans, credit cards, home equity lines of credit (HELOC), personal loans, and small-to-medium business (SMB) loans [12][14]. In B2B lending, trade credit insurance leverages AI to analyze both structured and unstructured data - like news reports and financial statements - to predict defaults and shield lenders from non-payment [3].

Loan Type

AI Application

Key Benefit

Automated risk ranking

Over 20% reduction in risk

Financial statement analysis and default prediction

Faster decisions for competitive markets

Interpretable logic for regulatory compliance

Transparent credit line decisions

Unstructured data analysis for B2B defaults

Improved underwriting accuracy

A standout example is TruStage Payment Guard, which integrates payment protection into digital lending platforms. This innovation earned the 2024 Celent Model Insurer Award for Innovation Execution [11].

Embedded insurance offers more than just financial protection - it builds trust. Borrowers are more likely to take on loans when they know safeguards are in place. For lenders, it reduces net losses by shifting risk to insurance providers.

Ron Shevlin, Chief Research Officer at Cornerstone Advisors, highlights the financial upside:

"Many lenders can achieve a 20% reduction in charge-off costs with loan payment protection. A growth-focused lender can save $42 in charge-off costs for every $1 in insurance premiums."

This model also enables lenders to extend credit to underserved borrowers. By leveraging insurance to offset higher-risk profiles identified by AI, lenders can approve loans they might otherwise reject, without increasing overall exposure. Projections indicate that embedded sales of property and casualty insurance in the U.S. could surpass $70 billion by 2030 [15].

Operationally, embedded insurance offers efficiency. API integration at the point of sale reduces loan abandonment rates and eases collection efforts. Danielle Sesko, Director of Product Management at TruStage, explains:

"We see embedded payment insurance as a key component of digital lending... for lenders, it provides an effective way to manage risk while expanding access to credit to more U.S. consumers."

These examples highlight how AI predictions and insurance work hand-in-hand to manage credit risk in both consumer and commercial lending.

Credit unions are increasingly turning to AI-powered tools combined with insurance to enhance their lending processes. For instance, MKIII's Loan Decision Model (LDM) evaluates borrower risk, while Munich Re's aiSure provides coverage for losses stemming from prediction errors or data drift [17].

Similarly, Instnt's AI platform focuses on fraud prevention by blocking suspicious transactions. To back this up, Munich Re offers reinsurance protection, shielding businesses from financial losses caused by fraudulent activities [17].

AI-insurance strategies are also making a mark in commercial lending, offering scalable solutions for credit risk management.

Trade credit insurers utilize AI to process unstructured data through methods like Optical Character Recognition (OCR) and sentiment analysis. These tools can identify warning signs of defaults or credit events as early as six to eight months in advance [3][18].

Barker, a lender specializing in luxury asset-backed loans, provides another example. They use AI technology to appraise luxury assets offered as collateral. Munich Re supports this model by offering a performance warranty, which compensates for discrepancies if the AI-generated valuation turns out to be inaccurate [17].

Several factors underpin the success of AI-insurance initiatives:

These examples demonstrate how AI-driven insights, when paired with embedded insurance, create a robust framework for managing credit risk effectively. Together, they provide lenders with the tools to make informed decisions while minimizing financial exposure.

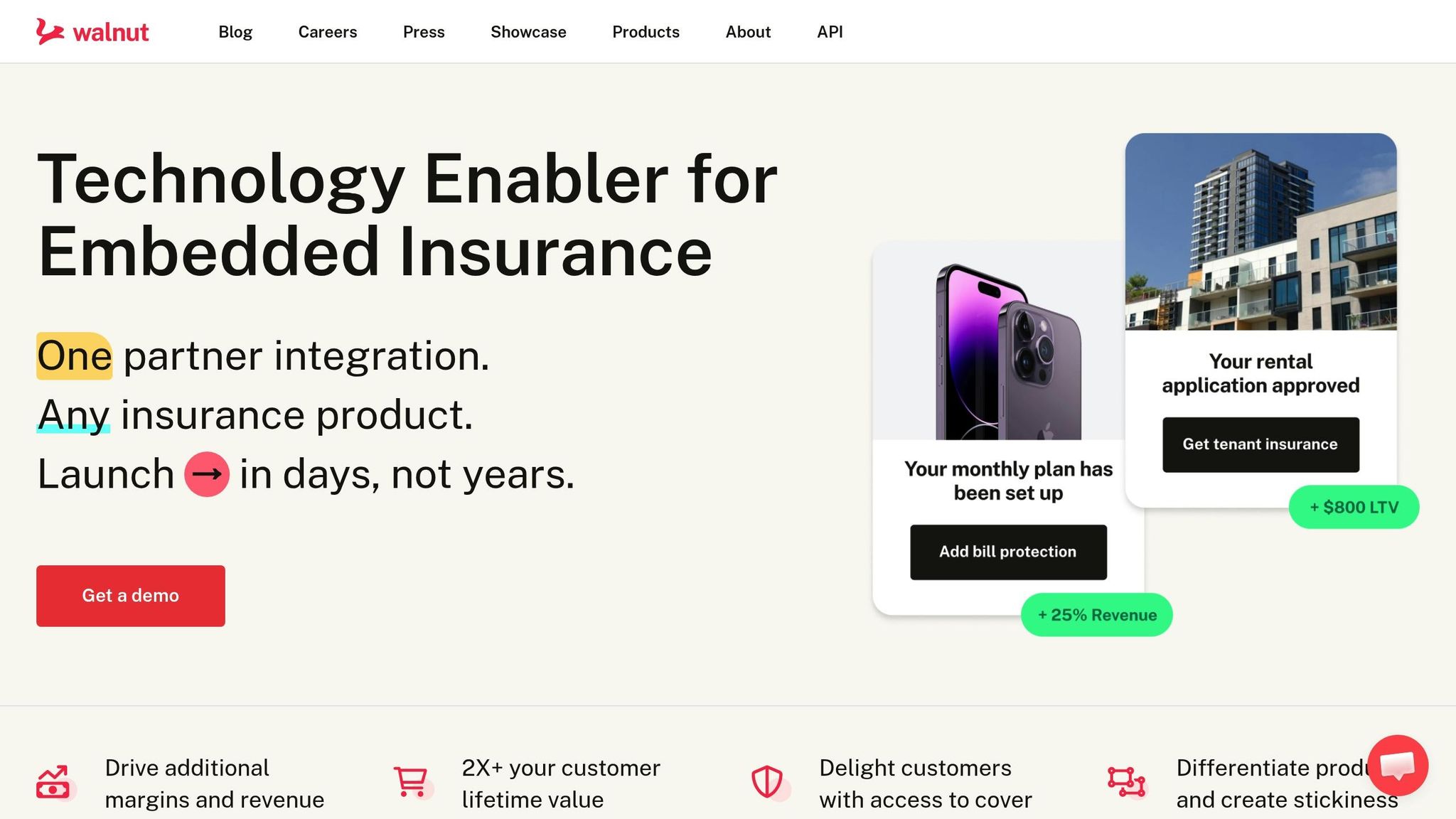

Walnut Insurance demonstrates how an API-driven approach can simplify and improve the process of embedding insurance into financial products. With a single API integration, Walnut connects lenders to 14 insurance carriers, removing the hassle of managing individual relationships with each provider. The platform takes care of the entire insurance lifecycle - from generating real-time quotes and binding policies to automating servicing workflows - while also ensuring compliance with licensing and broker-of-record requirements [20][21].

For lenders, Walnut offers Creditor Insurance APIs that integrate balance and mortgage protection directly into loan applications. This allows borrowers to enroll in coverage that safeguards their loan balance in cases of job loss or illness, which helps lenders minimize charge-offs and collection efforts [19][20]. The platform supports both API-first and no-code deployment, enabling integration in less than a day [20][21]. This ease of use has already led to tangible success stories.

Neo Financial, a Canadian neo-bank with over 1 million customers, adopted Walnut's platform in 2024–2025 to embed insurance into their credit card and mortgage offerings. They introduced coverages like extended warranty and purchase protection for credit cards, as well as premium plans offering mobile phone protection and life insurance - all seamlessly integrated into their digital ecosystem. Andrew Chau, Co-founder & CEO of Neo Financial, shared:

"We're excited to partner with Walnut, bringing insurance into the digital age and creating greater access to protection for all Canadians. We've been impressed with how their infrastructure has been able to support us in growing our product offering."

The results speak for themselves. Lenders using Walnut can double (2X+) their customer lifetime value by incorporating embedded insurance into their services [20]. A centralized dashboard further enhances usability by allowing businesses to track performance, conversion rates, and enrollment metrics across regions and products in real time [21]. Walnut’s platform is available on AWS Marketplace for $10,000 per month, with pricing based on API usage and the number of enrolled users [21].

From a technical perspective, Walnut’s API employs x-api-key authentication and includes specific endpoints tailored for loan creditor insurance [19]. The platform also features a fully managed brokerage layer that handles support and claims, easing the operational load for fintech partners [21]. By combining predictive analytics with efficient loss mitigation tools, Walnut enables lenders to launch insurance programs in a matter of days or weeks - no prior insurance expertise required [20][21].

Start by assessing whether AI credit scoring paired with embedded insurance could enhance your operations. Look at key metrics like charge-off rates, acquisition costs, and lifetime value. If high default rates or retention issues are a concern, this strategy might offer solutions. Additionally, consider if your customers would benefit from loan protection products.

You'll need to choose between two approaches for implementation. The Greenfield approach involves creating new capabilities in a separate environment, perfect for digital-first ventures that prioritize speed and adaptability. Meanwhile, the Brownfield approach builds on your existing infrastructure by adding new API and data management layers, leveraging your current licenses and compliance frameworks. For example, a European insurer used the Greenfield strategy to integrate travel and gadget insurance into fintech and mobility platforms by partnering with a software provider to build a tailored stack [22].

This initial evaluation is crucial in identifying the right technology partners for your needs.

When choosing technology partners, focus on platforms that offer plug-and-play solutions with standardized APIs and ready-to-use SDKs. Platforms with no-code or low-code capabilities are particularly useful, as they allow business teams to adjust policy terms, benefits, and pricing without needing developers [22]. This flexibility is becoming increasingly important, with embedded insurance expected to grow from $13 billion in gross written premiums in 2025 to over $70 billion by 2030 [22].

Ensure your chosen platform is cloud-native and capable of handling high transaction volumes while maintaining strict data privacy and consent standards [22]. According to BCG:

"Embedded insurance is no longer just an add-on; it is becoming a native function of next-generation insurance technology platforms"

.

To stay competitive, aim to retain 70–80% of your digital talent in-house [2]. Balance your investments between AI development and user adoption initiatives, as effective change management is key to achieving meaningful impact, both financially and operationally [2].

Once your technology partners are onboard, shift your focus to performance tracking. Monitor critical metrics like sales conversion (aim for a 10–20% improvement), onboarding costs (target a 20–40% reduction), and claims accuracy (strive for a 3–5% boost) [2]. Create a central AI control unit to oversee these efforts and ensure systematic tracking.

Regular updates to your AI models are essential to address model drift. In 2024, Aviva demonstrated this by deploying over 80 AI models in its claims process. These models reduced liability assessment time for complex cases by 23 days, improved claim routing accuracy by 30%, and cut customer complaints by 65%, saving the company more than £60 million ($82 million) that year [2].

Additionally, review your Probability of Default (PD) models regularly to reflect changes in economic conditions and borrower behavior. As Bill Quadrini from S&P Global Market Intelligence notes:

"PD models are designed to adapt to changing market conditions, providing lenders with a real-time assessment of credit risk"

.

Focusing on domain-wide KPIs rather than isolated metrics can lead to transformational improvements, potentially driving double-digit gains to your bottom line [2].

Credit risk management has entered a new era, combining advanced technologies for a stronger, more adaptable approach. AI-powered Probability of Default models anticipate potential defaults, while embedded insurance cushions the financial blow when defaults occur. Together, these two layers form a robust system that’s far more effective than relying on a single method [4].

The numbers speak for themselves. Early adopters of AI and insurance integration are reaping substantial rewards. For instance, AI leaders in insurance have achieved 6.1 times the Total Shareholder Return compared to laggards over a five-year span [2]. Meanwhile, embedded insurance sales in the U.S. are projected to reach $70 billion by 2030 [23]. Financial institutions that embrace these technologies now are positioning themselves to capitalize on a market expected to contribute over $12.5 trillion to global GDP by 2032 [5].

This shift also enables lenders to move beyond rigid, one-size-fits-all policies. With real-time risk profiling, they can make smarter, data-driven decisions. Credit limits can be customized to match individual risk levels, and early identification of default risks allows for proactive measures like rate adjustments or financial counseling [1]. These strategies help minimize losses and improve customer outcomes.

Embedded insurance adds another layer of value. By offering insurance at the point of sale, lenders maintain direct relationships with their customers, avoiding disintermediation by manufacturers or third-party platforms [23]. As Alex Timm, CEO of Root Insurance, puts it:

"Talking to consumers at the time when they really need insurance - like when they're purchasing a vehicle - is a lot better customer experience than being bombarded with advertisements"

.

Institutions that delay adopting this integrated model risk losing ground to competitors who are already leveraging these tools. The opportunity to secure partnerships and establish a strong market presence is narrowing as distribution channels evolve. The future belongs to those who seamlessly combine AI-driven risk prediction with embedded insurance solutions.

Lenders can use AI responsibly for predicting defaults by implementing frameworks that prioritize fairness. This involves pre-processing audits to detect and address biases in data, in-processing techniques like fairness-constrained optimization during model training, and post-processing adjustments to refine outcomes. Adding explainability to AI systems and maintaining human oversight ensures decisions are transparent and fair, minimizing the chances of unintended discrimination.

Embedded loan insurance provides a safety net for borrowers by covering loan repayments if unexpected events occur, such as losing a job, becoming disabled, or passing away. This type of coverage not only helps maintain the borrower’s credit score but also protects the lender from potential financial losses.

Lenders keep a close eye on ROI by looking at how much they can reduce defaults and charge-offs. Embedded insurance plays a big role here - it has the potential to lower charge-offs by as much as 20%, which translates into substantial savings for every loan. This not only strengthens portfolio performance but also boosts overall profitability.